Unsettled payments are one of the most persistent operational headaches in debt recovery. You may receive an ACH payment authorization, post it in your system, and still wait days for funds to settle. Those timing gaps complicate forecasting, delay reconciliations, and distort performance reporting across teams.

The ACH Network remains the backbone of electronic payments. It processed 35.2 billion transactions worth $93 trillion in 2025. Yet not all of those transfers settle at the same pace. For collection agencies, understanding how long an ACH transfer takes is critical to cash flow reliability, operational efficiency, and consumer communication.

In this blog, we clarify standard ACH timing, identify the key factors that impact settlement speed, and explain how this knowledge can strengthen your collections outcomes.

Quick look:

In debt collections, an ACH transfer is a consumer-authorized bank-to-bank debit that moves funds without card networks or paper instruments. It follows structured clearing rules set by Nacha, which affect timing, settlement, and cost in ways that differ from other payment methods.

Benefits of ACH transfers:

These advantages explain why ACH remains central to collections workflows. In the next section, we walk through the standard ACH processing timeline, so you can see where delays occur and how they impact your operations.

Suggested Read: How to Use ACH Agreements for Faster Debt Recovery

ACH moves in bank-controlled batches and follows operating rules set by Nacha. This means timing depends on when files enter the network and how banks process them.

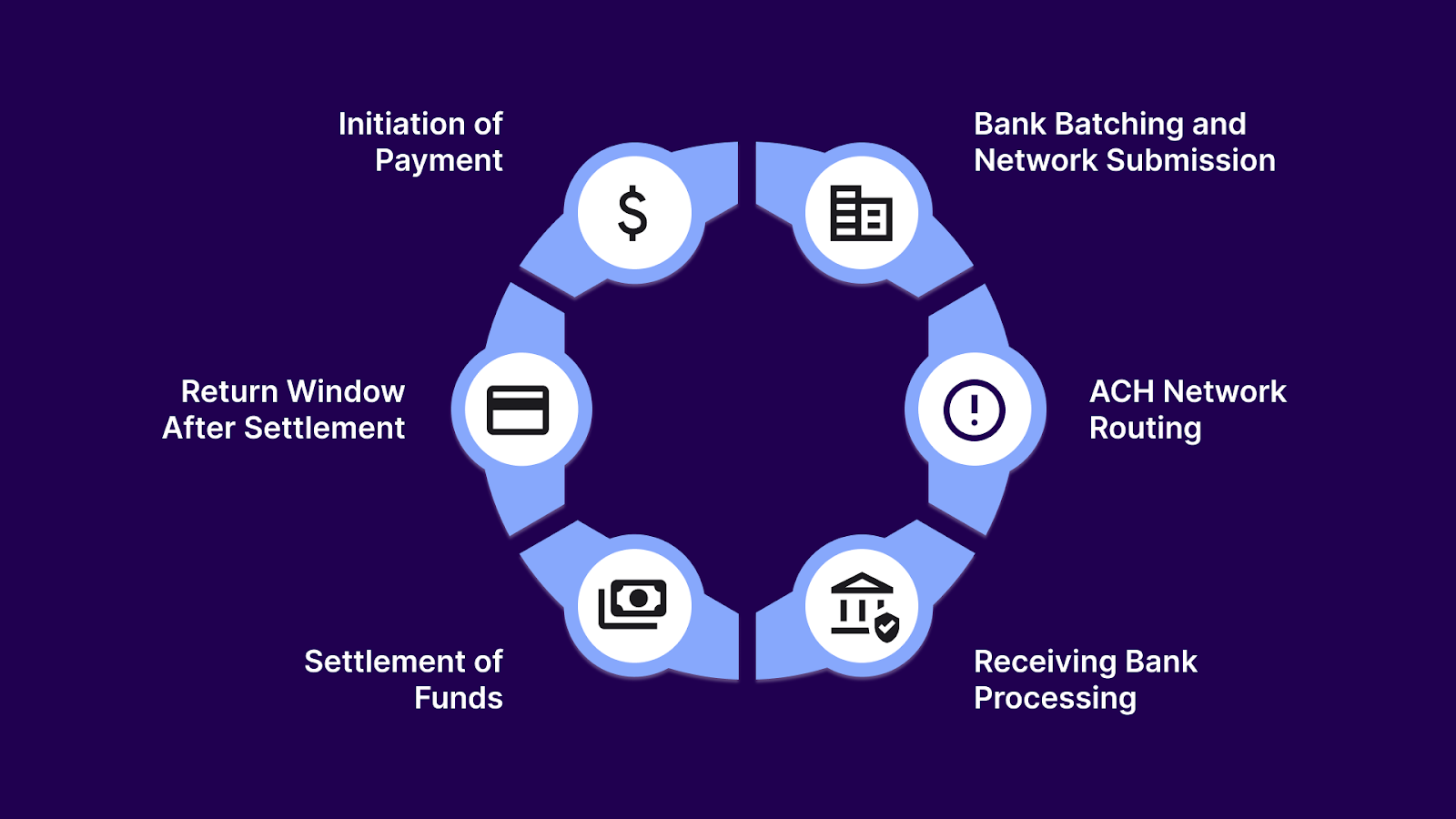

This is how ACH payments work:

This stage begins when the consumer authorizes the debit, and the agency submits the entry through its processor to the Originating Depository Financial Institution (ODFI). The timestamp of this submission determines whether the payment starts moving the same day or the next business day.

The key variables at this stage are:

The ODFI groups multiple ACH entries into batches and sends them to the ACH Operator at scheduled intervals during the business day. If the batch misses a window, it waits for the next cycle.

The key variables at this stage are:

The ACH Operator sorts entries and routes them to the Receiving Depository Financial Institution (RDFI). This routing only occurs on banking days and pauses on weekends and federal holidays.

The key variables at this stage are:

The RDFI receives the debit request and validates the account for accuracy, authorization, and available funds. At this point, the agency system may show a pending or successful status even though settlement has not occurred.

The key variables at this stage are:

Funds are officially moved between banks at settlement, when the payment is truly complete from a cash flow perspective. While standard ACH timelines are 1–3 business days, Nacha reports that about 80% of ACH payments settle within one banking day when submitted within processing windows.

The key variables at this stage are:

Even after settlement, ACH rules allow the RDFI to return the transaction if issues are discovered. These returns often occur within two business days, sometimes later, depending on the return reason.

The key variables at this stage are:

Tratta gives your team real visibility into where every ACH payment stands from authorization to settlement. You can reduce reconciliation guesswork, prevent premature posting, and respond faster to returns. Schedule a demo.

ACH delays are rarely random. They are usually tied to banking schedules, submission timing, data accuracy, and Nacha-governed return rules.

Common factors that introduce ACH delays in collections:

These variables explain why ACH timing often feels unpredictable inside collections workflows. In the next section, we examine why ACH transfers can feel slow operationally, even when they are moving exactly as designed through the banking system.

ACH often gets blamed for delays that are actually caused by how collections teams track and interpret payment status. The banking system may be moving the payment exactly as designed, but internal workflows, posting practices, and reporting views create the perception that nothing is happening.

These are a few reasons why ACH transfers may seem slow:

In the next section, we compare Same-Day ACH and standard ACH, and when each makes sense in collections operations.

Suggested Read: Reduce Fraud Risk in Collections Through ACH Check Verification

When agencies evaluate ACH speed, the real decision is not whether ACH is fast or slow. It is whether Same-Day ACH or standard ACH fits the payment scenario.

Table showing differences that affect timelines:

Tratta gives agencies clear visibility into every stage of the ACH lifecycle, replacing vague statuses with actionable detail. Built-in validation reduces errors before submission, and detailed tracking across cutoffs, batching, and settlement helps teams choose the right rail and reconcile funds confidently. Learn more.

Cards, wires, checks, and newer real-time rails all appear in day-to-day recovery workflows. Each method differs in settlement speed, cost, and risk, which directly affects how quickly agencies can convert promises into usable funds.

Table showing how different payment methods help in debt collections:

The right method depends on the payment context, the balance size, and the speed at which funds must settle for operational or reporting purposes. In the next section, we share practical tips for agencies to ensure payments settle quickly and predictably.

Suggested Read: ACH Reversal in Debt Recovery: Everything Agencies Need to Know

Payment speed is not controlled solely by the banking system. Many delays begin inside agency workflows before the file ever reaches a bank.

Steps agencies can take to improve payment settlement timelines:

When systems provide clear visibility into payment stages, validation at entry, and tracking across banking steps, these practices become easier to execute consistently across teams.

Suggested Read: 5 Best ACH Alternatives for Debt Collection Agencies in 2026

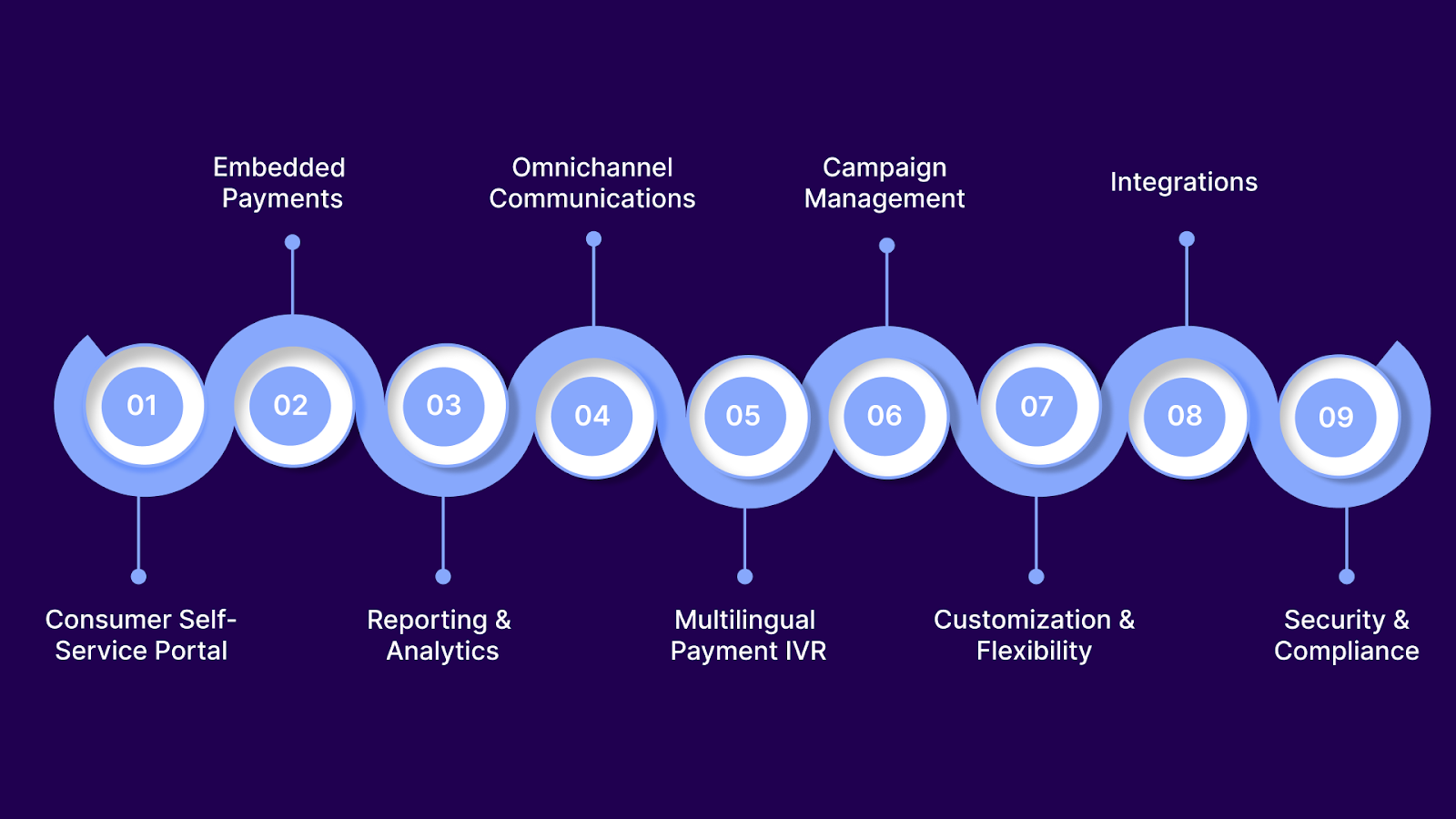

Tratta is a collections payment and engagement platform designed for agencies that rely on timely settlement and clear payment visibility. We bring payment capture, processing, communication, and reporting into one system so you can see where delays start and prevent them before they affect cash flow.

Core features include:

Consumers enter their own bank details and authorize payments directly. This reduces keying errors that often cause ACH rejects and returns.

ACH processing happens inside the platform without handoffs to external tools. This shortens the time between authorization and bank submission.

You can see whether a payment is authorized, submitted, in processing, settled, or returned. This removes guesswork from reconciliation and performance reporting.

SMS, email, and other channels deliver payment links instantly. Faster consumer action helps agencies meet cutoff windows more consistently.

Consumers can make payments through IVR in English and Spanish. This reduces the friction that delays authorizations.

Automated reminders and workflows are triggered based on payment status. This reduces lag between failed attempts and recovery action.

Workflows, payment options, and timing rules can be configured to match your agency’s operating model. This ensures ACH handling aligns with how your team works.

Payment data flows directly into your existing systems. This prevents delays caused by manual exports, imports, or status mismatches.

Banking data is handled securely in accordance with ACH operating rules and regulatory requirements. This protects both the agency and the consumer while payments move through the network.

Tratta does not just help you process payments. We help you understand them, track them, and recover faster with clarity your team can rely on every day.

When an ACH payment is delayed, the impact goes beyond timing. Reconciliations fall behind, cash flow forecasts become unreliable, and teams spend time investigating payments that appear complete but are still moving through banking stages.

Tratta removes that uncertainty by combining a consumer self-service portal, embedded payments, and real-time reporting into a single connected system. Your team can see exactly where each payment stands and act early to prevent delays from affecting recovery.

Book a demo to understand how your agency can track, reconcile, and recover payments with confidence.

Most ACH transfers settle within one to three business days. Many are completed within one banking day when submitted before the cutoff windows, but weekends, holidays, and batching schedules can extend timelines.

The five-day rule refers to the window banks may use to return certain ACH debits, especially unauthorized claims. Funds may appear settled earlier but remain exposed to potential returns during this period.

No. ACH authorization happens instantly, but fund movement occurs later through bank batches. Agencies may see payment confirmation before the receiving bank completes settlement and posts funds.

ACH is batch processed rather than real-time. Files move through scheduled bank windows, skip non-banking days, and pass validation checks before settlement between financial institutions.

Many delays are avoidable with accurate data entry, timely file submission before cutoffs, and clear visibility into payment stages. Proper tracking reduces reconciliation issues and recovery slowdowns.