The CFPB received approximately 207,800 debt collection complaints in 2024, nearly double the volume from the year before. A significant share of those complaints came down to how calls were conducted: wrong disclosures, aggressive language, or no clear process.

If you run a collection agency, manage receivables for a credit issuer, or oversee outreach operations at a debt buyer, the scripts your agents use are not just a means of communication. They are a compliance document, a recovery driver, and the first real touchpoint with a consumer who may be anxious, defensive, or genuinely unable to pay.

This guide provides practical, FDCPA-compliant debt-collection call scripts for the scenarios your team faces every day, including initial contact, payment-plan negotiations, hardship situations, disputes, and follow-ups. You will also find guidance on what makes scripts fail and how to structure your overall call process to support both recovery and compliance.

A debt collection call script is a pre-written framework that guides agents through conversations with consumers about outstanding balances. It is not a rigid word-for-word read but a structured outline that ensures every call covers required disclosures, stays compliant, and moves toward a resolution.

Scripts are used across collection agencies, law firms handling debt-related matters, AR teams at credit issuers, and debt buyers managing purchased portfolios. The use case is the same across contexts: provide agents with a consistent, legally sound starting point they can adapt to as the consumer responds.

What separates a good script from a bad one is not length. It is structured. A well-built script ensures agents never skip the mini-Miranda, always verify identity before disclosing account details, offer realistic payment options, and document the outcome of every call.

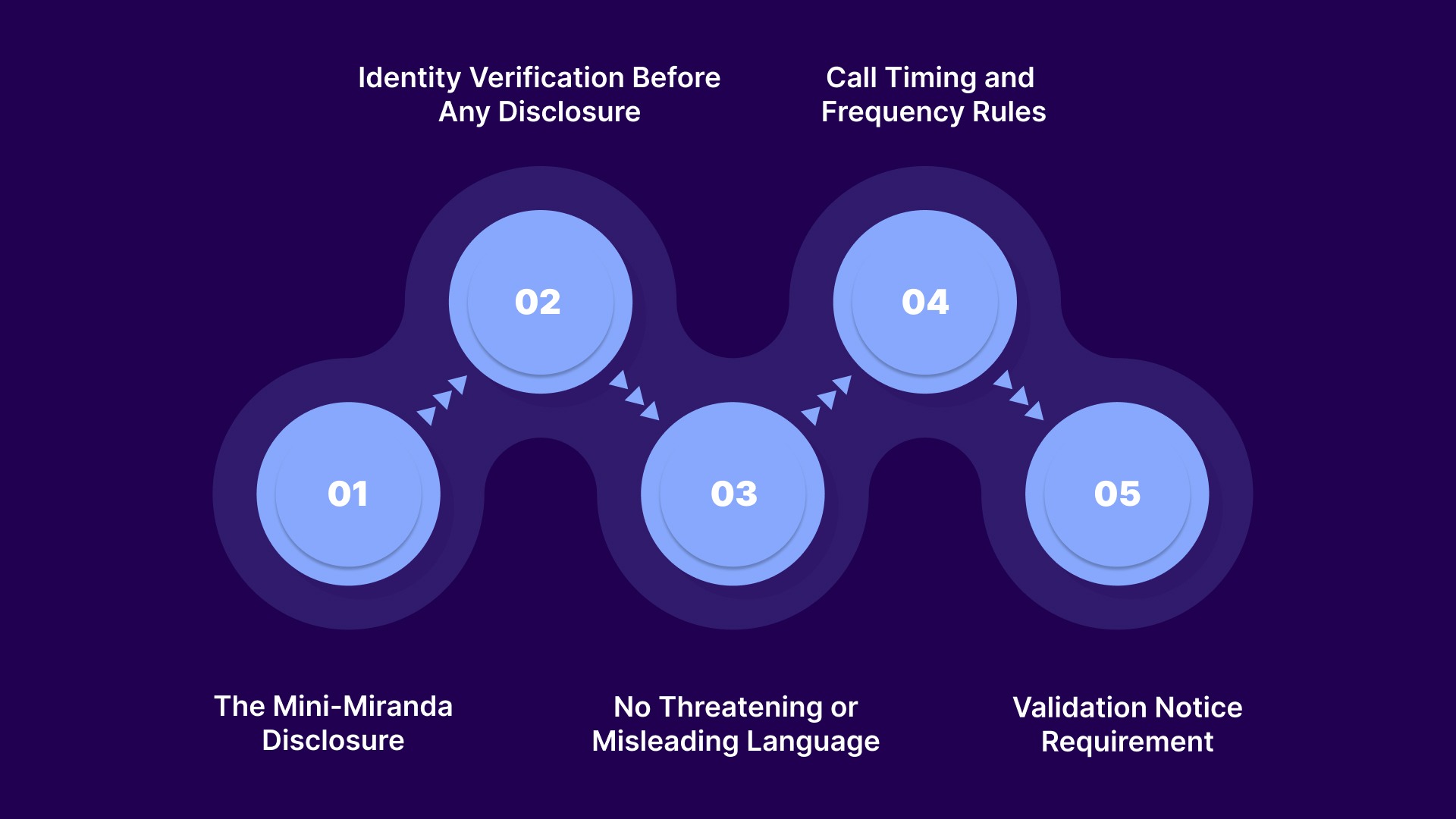

Before you build or use any collection call script, you need to understand the legal floor. The Fair Debt Collection Practices Act (FDCPA) sets specific requirements for every consumer contact, and scripts must be built around them.

On the initial contact with a consumer, every collector must state that the communication is an attempt to collect a debt and that any information obtained will be used for that purpose. This is required whether the contact is by phone, voicemail, text, or email. In subsequent calls, collectors must still identify themselves as a debt collector, even if the full mini-Miranda is not repeated.

Standard Mini-Miranda Language: "This is an attempt to collect a debt, and any information obtained will be used for that purpose."

You must confirm you are speaking with the right person before disclosing any account information. Never state the balance, creditor name, or any account details until you have verified identity. This is not just good practice - it is an FDCPA requirement to prevent third-party disclosure.

Scripts must not imply that legal action will be taken if it is not actually planned or permitted. Threatening to sue, arrest, or garnish wages when those actions are not authorized is an FDCPA violation. Language that misrepresents the legal status of a debt, including time-barred accounts, is also prohibited.

Under Regulation F, collectors are limited to seven call attempts per week per debt. Calls are not permitted before 8 AM or after 9 PM in the consumer's local time zone. Scripts should reflect this by confirming with agents that timing has been checked before dialing.

Within five business days of initial contact, you must send a written validation notice that includes the debt amount, creditor name, and information about the consumer's right to dispute the debt. Your call scripts should prompt agents to confirm that this notice will follow the call.

Suggested Read: Essential Debt Collection Software Features Your System Needs

Every scenario calls for a slightly different script, but the building blocks stay the same. Here is what every effective collection call script needs to include:

Strong scripts balance structure with adaptability to guide conversations toward resolution. Each component ensures clarity, compliance, and a higher chance of successful recovery.

Suggested Read: How to Stay Compliant With the Fair Debt Collection Practices Act

The scripts below are structured around FDCPA requirements. Your agents should treat these as frameworks to adapt - not word-for-word reads. The goal is consistency in compliance and flexibility in tone.

Use this for outbound debt collection calls when your team is contacting the consumer for the first time.

Sample First-Contact Collection Call Script

Script 2: Consumer Requests a Payment Plan

This script is for consumers who acknowledge the debt but say they cannot pay in full. Use it to negotiate manageable installments and document commitments.

Sample Payment Plan Negotiation Script

Script 3: Consumer Claims Financial Hardship

When a consumer indicates they are facing serious financial difficulty, job loss, medical emergency, or other hardship, your script must shift to active listening and empathy without abandoning the goal of finding a resolution.

Sample Hardship Collection Call Script

If a consumer says they do not recognize the debt, believe it is incorrect, or request validation, you must stop collection activity immediately and honor the dispute process.

Sample Dispute Handling Script

Script 5: Follow-Up After a Missed Payment Commitment

When a consumer promised to pay on a specific date, and the payment did not come through, your follow-up script should be firm but not aggressive.

Sample Follow-Up Collection Call Script

Script 6: Leaving a Voicemail (Compliant)

Voicemails count as initial communications under the FDCPA and must include compliant language. At the same time, they must not disclose the existence of the debt to an unknown third party. This creates a narrow window for what you can say.

Sample FDCPA-Compliant Voicemail Script

Script 7: Payment Reminder Call (Warm Outreach)

This applies to AR teams at credit issuers or original creditors reaching consumers who are mildly overdue but have a positive payment history. The tone here should be conversational and low-pressure.

Sample Payment Reminder Call Script

These debt collection call-script examples are structured to align with FDCPA‑driven compliance expectations when the caller is a third‑party debt collector. Your agents should treat them as flexible frameworks to adapt, not word‑for‑word reads.

The goal is to maintain consistency in compliance while allowing flexibility in tone. When using these scripts for original‑creditor or in‑house collections, verify your specific disclosure and calling‑rule obligations with your legal team, because FDCPA‑style requirements apply differently in those contexts.

Managing payment commitments, follow-ups, and compliance across hundreds of accounts manually is a heavy lift.

Tratta's consumer self-service platform gives your team a structured way to track payment arrangements and consumer interactions in one place. See how it works at tratta.io

Suggested Read: SMS Compliance Laws and Regulations

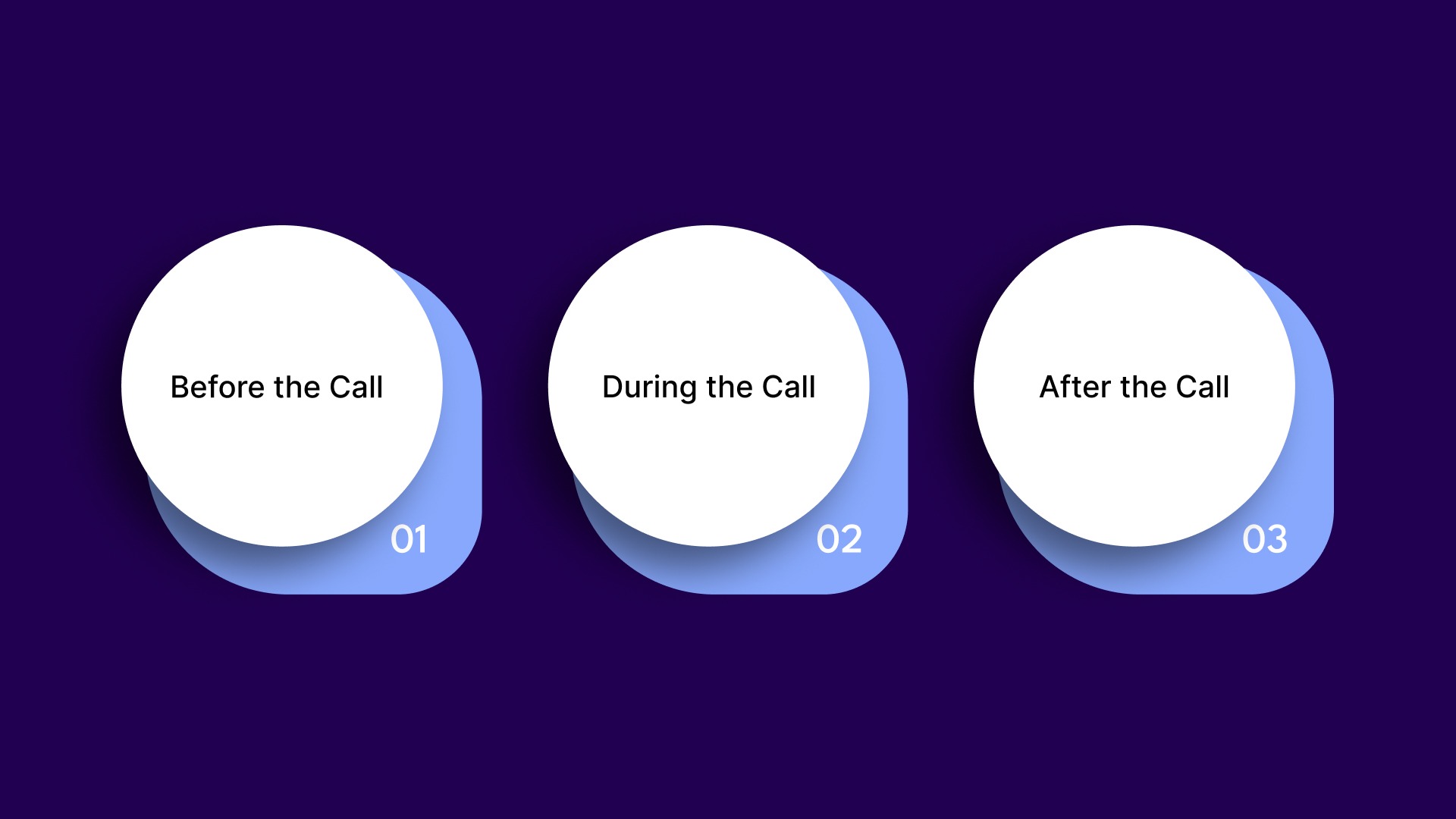

Scripts work best when they are embedded within a consistent call process. Without that structure, even good scripts get skipped, shortened, or delivered inconsistently. Here is what an effective outbound collection call process looks like from start to finish.

Process alignment ensures agents act with context, turning isolated calls into part of a coordinated recovery workflow across the entire account lifecycle.

Suggested Read: CFPB Credit Card Late Fee Lawsuits and Legal Developments 2026

The right script tone and language shifts depending on who is calling and who they represent. Here is how the approach differs across common collection contexts.

Accounts receivable call scripts break down most often when agents hit objections they were not prepared for. Here are the most common ones and how to respond effectively.

Do not argue. Ask the consumer for the date and method of payment, log it, and tell them you will verify with your records and follow up. If the payment is confirmed, update the account immediately. If it is not confirmed, walk through the validation process.

Acknowledge the situation without offering anything you are not authorized to. Ask what their timeline looks like. Offer to note the hardship on the account and schedule a follow-up. Even a small commitment - a callback date, a partial payment - is better than ending the call with nothing documented.

Do not pressure the consumer to pay on a disputed account. Log the dispute, explain their right to request validation in writing, and pause outreach activity until the debt is validated. This is a legal requirement, not an option.

If a consumer requests in writing that you cease contact, you must stop. If the request is verbal, document it and check your legal obligations in the relevant state. Some state laws treat verbal cease-and-desist requests as binding. When in doubt, flag the account for your compliance team.

Escalation requests should be handled without hesitation. Document the request, transfer, or schedule the callback, and note the reason for escalation. Refusing or delaying supervisor escalation can be characterized as a harassment tactic under the FDCPA.

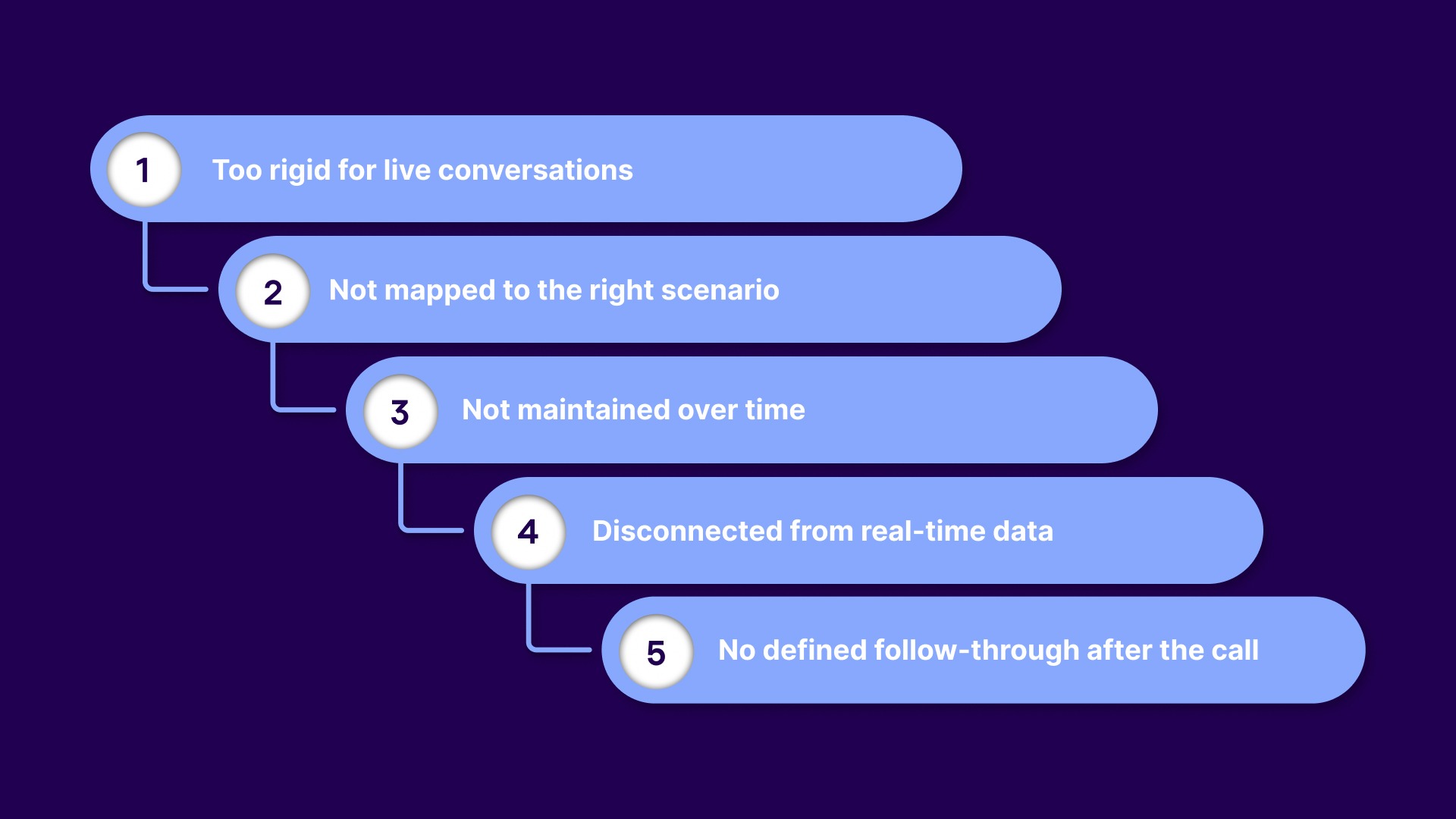

Most collection call scripts are built correctly. The breakdown occurs during execution, when scripts are used without alignment with real workflows, account context, and system support.

Here is where they fail:

Strong scripts support the conversation. Consistent outcomes depend on how well they are integrated into the surrounding system.

Federal FDCPA requirements set the baseline, but several states have stricter rules that affect how you script and conduct collection calls. If you are operating in high-volume states, these are worth knowing.

Important: This table is informational. Confirm your obligations with qualified legal counsel before building scripts for specific state markets.

Suggested Read: Debt Collection Compliance: Essential Regulations and Guidelines to Know

A well-written debt collection call script solves the conversation problem. But it does not solve what happens around it: tracking call attempts against Regulation F limits, logging outcomes, sending validation notices on time, managing payment arrangements, and keeping compliance-sensitive account activity documented.

For most collection agencies, debt buyers, and law firms, those operational gaps exist not because teams do not know better, but because they are working across disconnected tools. Call notes in one place, payment data in another, follow-ups managed manually. When volume increases, those gaps become a risk.

Tratta is debt collection software that brings payments, digital communications, reporting, and workflow management into one platform. Your agents can focus on the call while the system handles what comes before and after it.

Here is where Tratta supports the work your scripts set in motion:

Instead of managing compliance, tracking, and payments across disconnected tools, with Tratta, your team operates with full visibility and control from a single platform.

Effective collection call scripts are not defined by what is written, but by how consistently they are executed across every interaction. The difference shows up in outcomes, not intent.

Teams that treat scripts as part of a larger operational system can maintain control, improve consistency, and scale performance without adding friction.

Tratta supports this by bringing communication, payments, and workflows into one place, keeping execution consistent as operations grow.

To improve collection outcomes with better control and consistency, book a demo and see how Tratta works in practice.

A debt settlement script guides agents in negotiating reduced payoff amounts by confirming balances, assessing affordability, and proposing terms while maintaining compliance and a structured conversation flow.

A collection message script is used for SMS or email reminders, including account reference, payment link, and opt-out instructions, while avoiding sensitive disclosures to maintain compliance requirements.

A collection's phone call script helps agents structure conversations, verify identity, explain balances, and guide consumers toward payment or resolution while maintaining compliance and consistency across calls.

Outbound debt collection call script samples provide structured conversation flows for first contact, follow-ups, and negotiations, helping agents stay compliant and focused on achieving payment outcomes.

A collection call script sample is used in agent training to demonstrate compliant language, objection handling, and call flow, helping new collectors conduct effective, consistent conversations.