Reaching consumers through traditional collection methods is becoming increasingly difficult. Many third-party agencies face declining engagement rates, rising operational costs, and changing communication preferences. Research from McKinsey found that consumers contacted through digital channels made 12% more payments than those contacted through traditional channels.

That shift reflects a broader change in how consumers prefer to communicate and resolve accounts. If your agency is looking to improve recoveries while meeting modern expectations, a digital-first collection strategy may be the answer.

In this article, we explore its benefits, core components, implementation best practices, and the technologies that support successful execution.

Quick look:

A digital-first collection strategy places digital channels at the center of consumer engagement and recovery efforts. Instead of relying primarily on phone calls and letters, agencies use channels such as SMS, email, self-service portals, and digital payment tools to connect with consumers.

65% of U.S. citizens prefer to make online payments for regular monthly bills, according to a recent YouGov survey of 2,000 U.S. citizens.

For third-party debt collectors, a digital-first strategy can deliver several advantages:

A digital-first strategy is ultimately shaped by the people it is designed to reach. Consumer communication habits, payment preferences, and service expectations continue to evolve. In the next section, we will examine why consumer preferences are driving digital collections and what that means for third-party agencies.

Suggested Read: Collections Strategy in 2026: What Actually Works (Based on Real Agency Data)

Consumer expectations have changed significantly over the past decade. Many people now prefer to communicate, make purchases, and manage financial obligations through digital channels. This shift is influencing how third-party collection agencies engage consumers.

According to industry research, 73% of late-stage delinquent consumers made a payment after being contacted through digital channels, highlighting the effectiveness of digital engagement.

Several factors are accelerating this trend:

Meeting these expectations requires more than simply adding digital channels. Agencies need a platform that supports consistent communication, convenient payment experiences, and operational visibility. In the next section, we look at the core features of a successful strategy.

Suggested Read: Proven Debt Collection Techniques for Higher Recovery Rates

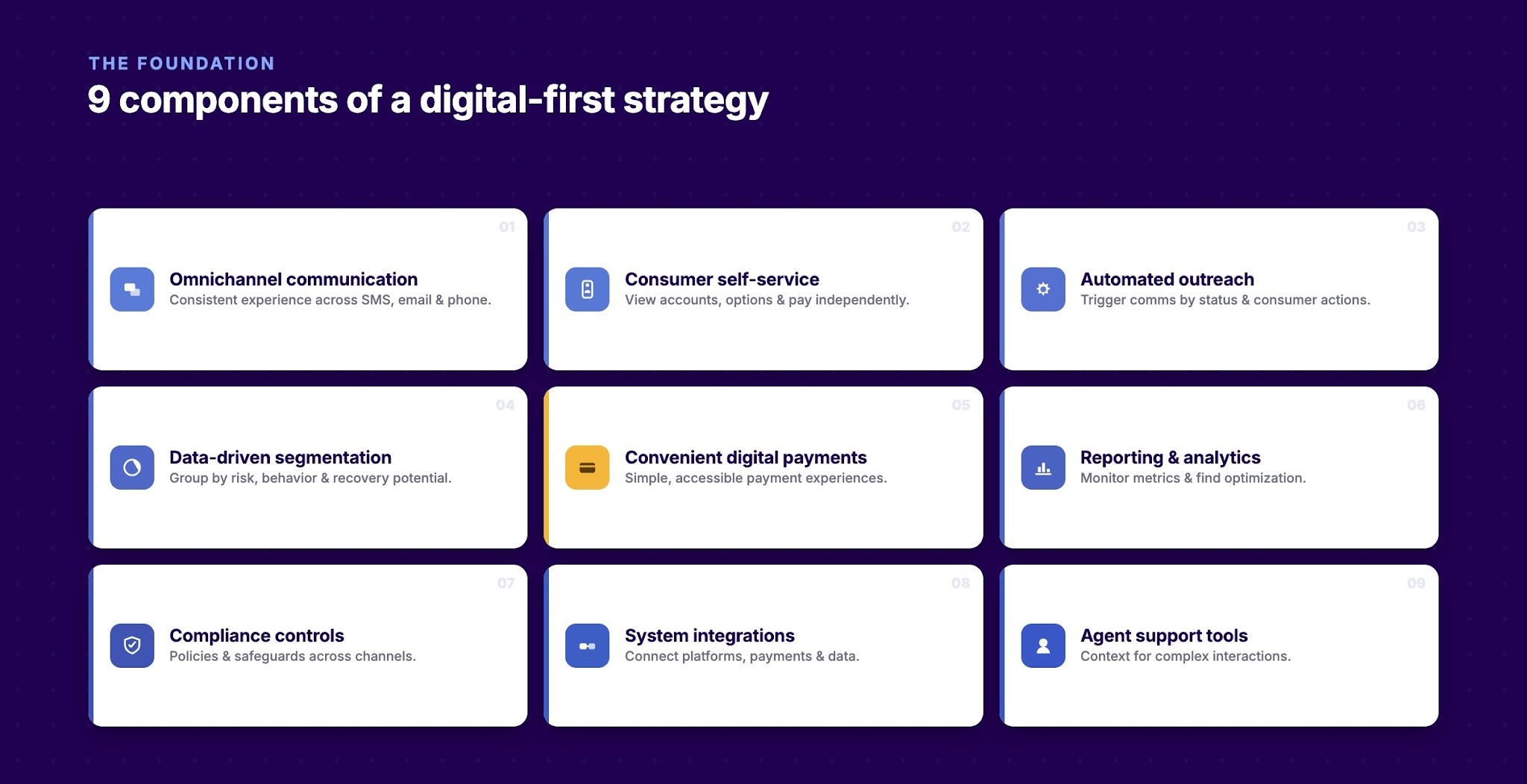

A digital-first strategy requires more than digital communication channels. Agencies must create a connected experience that supports engagement, payments, compliance, and performance management.

The following components form the foundation of an effective digital collection program.

Building these components is an important first step. However, agencies also need a practical plan for implementation and ongoing optimization.

Tratta helps support these goals through omnichannel communications, self-service payment options, automated campaigns, and integrated reporting. These capabilities help agencies align collection strategies with modern consumer preferences while maintaining operational control. Schedule a free demo.

A digital-first strategy requires careful planning and execution. Agencies must align technology, processes, and consumer engagement practices to achieve meaningful results.

The following steps can help guide implementation.

A successful strategy begins with understanding how consumers prefer to communicate and make payments. Different consumer segments may respond better to different channels and experiences.

Focus on the following areas:

Consumers often interact across multiple channels during the collection process. Agencies should create a coordinated experience that maintains consistency regardless of channel.

Key planning considerations include:

Many consumers prefer resolving accounts without speaking to an agent. Self-service tools can improve convenience while reducing operational demands.

Consider offering:

Automation helps agencies scale operations and improve consistency. It can also reduce manual workloads and support timely consumer engagement.

Common automation opportunities include:

Digital engagement increases the need for consistent compliance oversight. Policies should be applied across all communication channels and workflows.

Important controls include:

A digital-first strategy should evolve based on performance data. Continuous improvement helps agencies maximize recovery outcomes and consumer engagement.

Track metrics such as:

Implementing these steps can help agencies create a strong foundation for digital collections. The benefits become even clearer when viewed through practical applications. In the next section, we will explore real-world use cases of adopting a digital-first collection strategy.

Suggested Read: Digital Transformation and Its Impact on the Collection Industry

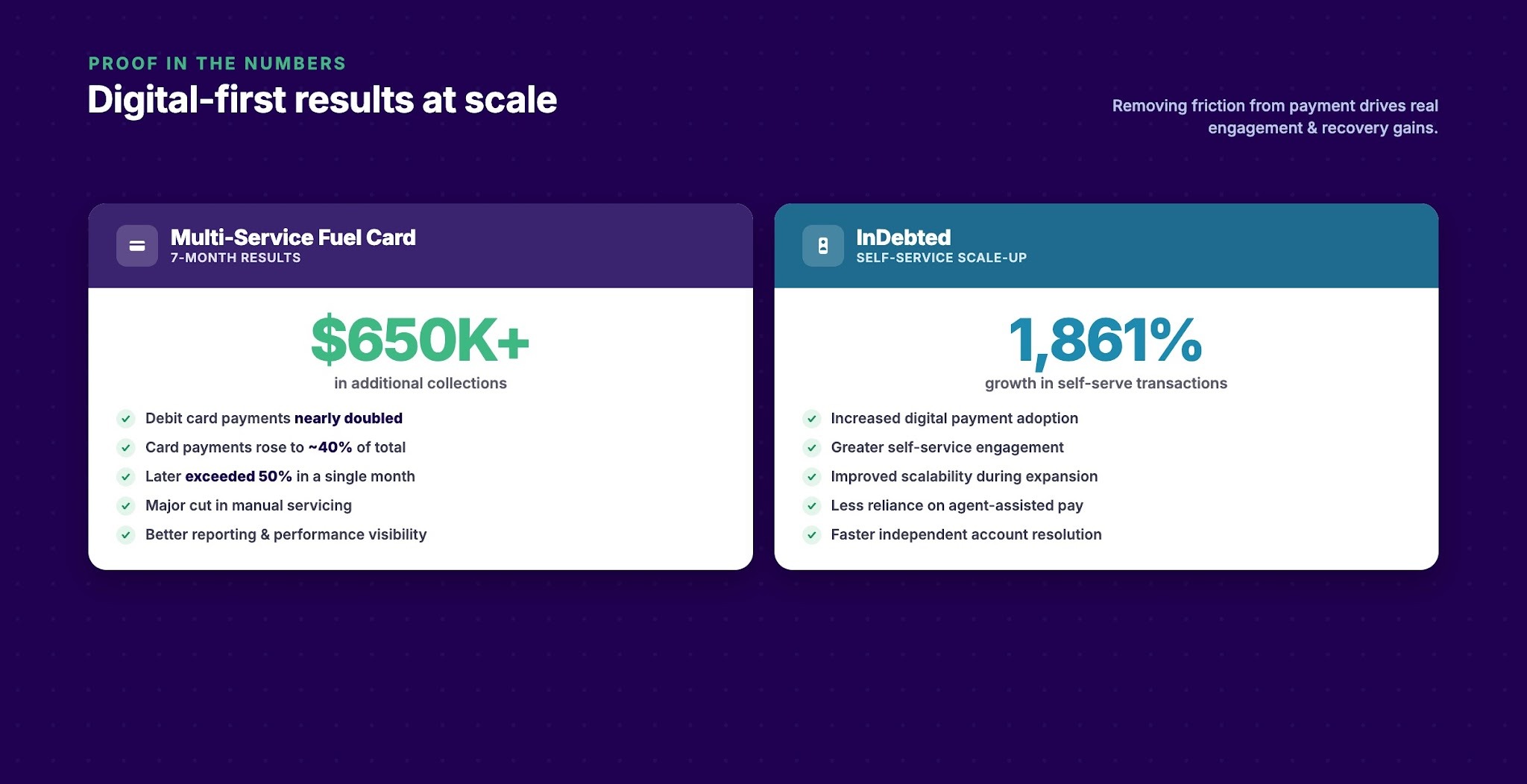

The benefits of digital-first collections are best demonstrated through real-world results. Organizations that remove friction from the payment process often see significant gains in both engagement and recoveries.

These case studies show how digital tools can improve collection performance at scale.

Multi-Service Fuel Card wanted to simplify account resolution and reduce the operational burden on its team. By implementing Tratta's digital payment and self-service capabilities, the company created a more convenient experience for customers while improving visibility into collection performance.

Tratta helped the company through:

The results included:

InDebted's digital-first strategy focused on helping consumers resolve accounts independently through digital channels. Its partnership with Tratta supported the company's expansion while increasing self-service adoption across its collection operations.

Tratta supported this initiative through:

The outcomes included:

The greatest results occur when agencies combine digital engagement, self-service experiences, and payment convenience into a unified strategy.

In the next section, we will examine the most common challenges agencies face when adopting a digital-first collection strategy and how to overcome them.

Suggested Read: 10 Practical Tips to Simplify Collections Management

While the benefits of digital-first collections are compelling, implementation can be challenging. Many agencies struggle to balance consumer expectations, operational requirements, and compliance obligations. Identifying common obstacles can help agencies build a more effective adoption plan.

Table showing common challenges:

Addressing these challenges requires a structured approach. Agencies that succeed typically focus on a few key operational practices:

The right technology plays a critical role in supporting these efforts. Agencies need platforms that connect communications, payments, reporting, compliance, and consumer engagement within a single workflow. When the technology is aligned with the collection strategy, digital-first initiatives become easier to manage, scale, and optimize.

A digital-first strategy can improve engagement and recovery performance. However, poor execution can create new challenges. Disconnected channels, limited self-service options, inconsistent consumer experiences, and weak compliance controls can reduce results and increase operational complexity.

Tratta helps third-party collection agencies execute digital-first strategies with confidence. The platform combines omnichannel communications, automated campaigns, self-service payment options, reporting and analytics, payment processing, and compliance-focused workflows in one solution. This enables agencies to create more convenient consumer experiences while improving operational efficiency and recovery outcomes.

See how Tratta can help your agency build and scale a successful digital-first collection strategy. Request a demo today to explore the platform in action.

Success is commonly measured using metrics such as payment rates, resolution rates, self-service adoption, consumer engagement, collection costs, and recovery performance. Agencies should track these metrics consistently to identify improvement opportunities.

There is no single best channel for every consumer. Effective agencies use a mix of SMS, email, phone, and self-service options, then adjust outreach based on consumer behavior and preferences.

Implementation timelines vary based on technology, integrations, and operational complexity. Some agencies can launch core digital capabilities within weeks, while larger transformations may take several months.

Yes. Digital engagement can support consumers throughout the collection lifecycle. Agencies often use different communication strategies and payment options depending on account status and recovery goals.

Digital tools can automate routine interactions and payment processes. This allows agents to spend more time handling complex accounts, negotiations, and consumer conversations that require personal attention.