Credit portfolios are growing fast, but traditional risk models are struggling to keep up. U.S. household debt exceeded $18.8 trillion in 2025, according to the Federal Reserve Bank of New York. This increase places greater pressure on lenders, collection agencies, and credit issuers to manage credit risk more effectively.

For collections teams, the challenge is practical. Large portfolios, limited agent capacity, and changing consumer behavior make it difficult to determine which accounts to prioritize and how to engage borrowers.

Advanced analytics in credit risk management offers a clearer path forward. By analyzing repayment patterns, financial signals, and engagement data, organizations can identify risk earlier, prioritize accounts more accurately, and improve outreach strategies.

In this blog, we explore how advanced analytics helps collections teams make better decisions, improve recovery outcomes, and manage credit risk more effectively.

Advanced analytics in credit risk management uses statistical models, predictive techniques, and machine learning to evaluate borrower behavior and repayment risk. Instead of relying only on static credit scores or manual reviews, these methods analyze large volumes of financial, behavioral, and transactional data to identify patterns linked to repayment or default.

Credit risk analytics helps organizations estimate the likelihood that a borrower will repay a loan or debt, and supports more informed decision-making across the credit lifecycle.

These analytics tools help estimate key risk indicators:

For collection agencies and credit issuers, this shift provides clearer visibility into portfolio risk. Better data allows teams to prioritize accounts more accurately.

However, many collections operations still rely on traditional approaches that were designed for a very different financial environment.

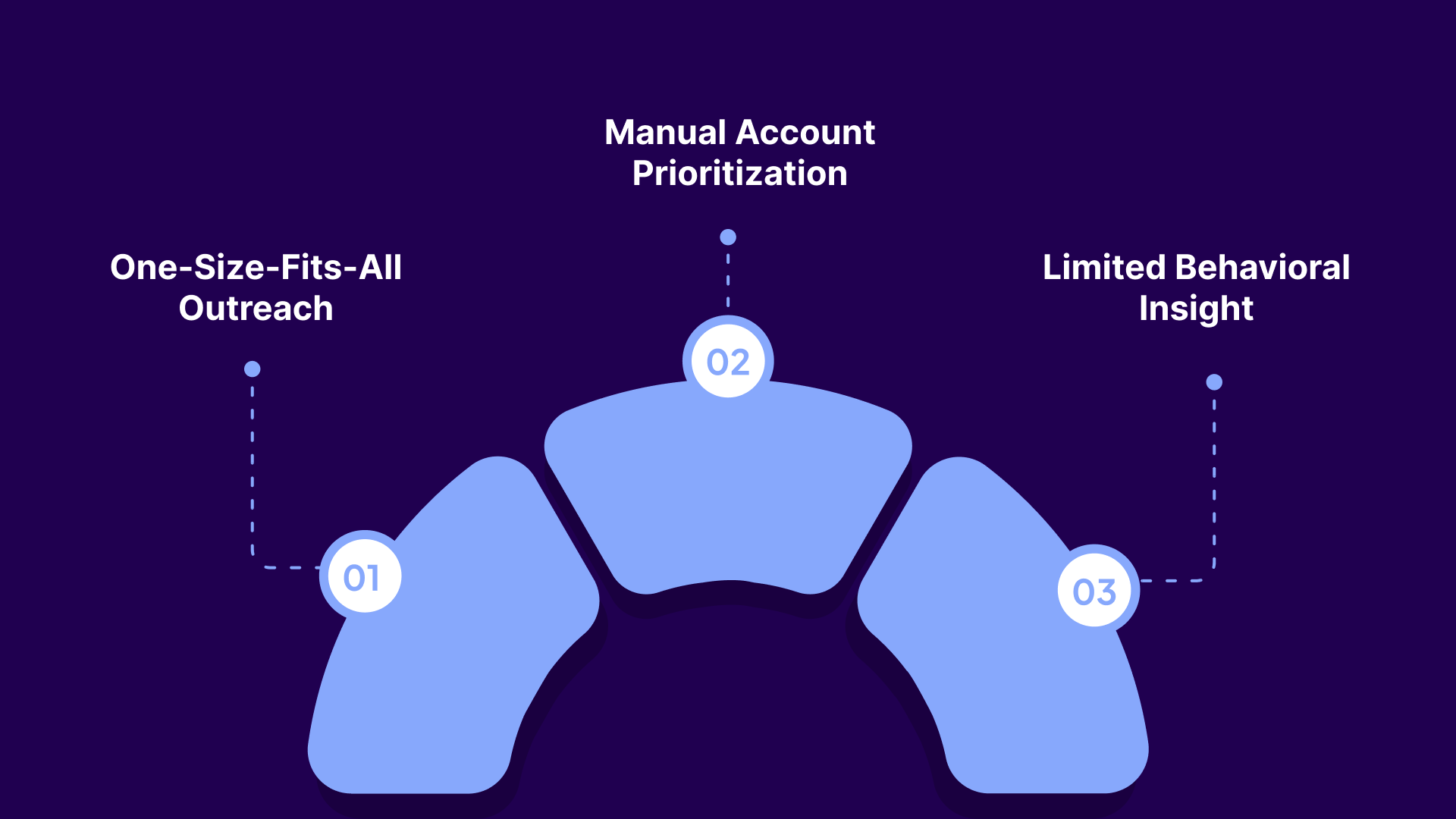

Many collections operations still rely on static workflows where accounts are prioritized by balance size or delinquency age, and outreach follows fixed schedules. While this approach worked in the past, it is less effective today, as borrower behavior and communication preferences vary widely.

1) One-Size-Fits-All Outreach: Using the same communication approach for every account often leads to low engagement. Consumers have different payment capacities and channel preferences. Some respond to digital reminders, while others prefer different forms of outreach. Uniform strategies overlook these differences.

2) Manual Account Prioritization: Collections teams often focus on accounts with the largest balances. However, higher balances do not always indicate a higher likelihood of repayment. Without data insights, teams may spend time on accounts with low recovery potential while overlooking those more likely to respond.

3) Limited Behavioral Insight: Traditional models rely mainly on historical credit data and rarely capture real-time behavioral changes. Factors such as employment shifts, spending patterns, or financial stress can influence repayment behavior.

Research published in the journal Risks shows that machine learning and advanced analytics improve credit risk predictions by identifying patterns in borrower data that traditional models may miss.

These limitations highlight why many organizations are adopting analytics-driven approaches to evaluate risk and manage delinquent accounts more effectively.

Also Read: Why Credit & Collection Policies Matter in 2026

Collection agencies and law firms often manage thousands of accounts across multiple creditor portfolios. Not every account has the same likelihood of repayment. Without reliable data insights, teams may spend time pursuing low-probability recoveries while overlooking accounts that could respond quickly.

Advanced analytics addresses this challenge by guiding recovery decisions with data rather than static rules. By analyzing repayment patterns, financial activity, and communication responses, organizations can prioritize accounts more accurately and identify risk earlier.

Predictive models analyze behavioral and financial signals to detect early signs of financial stress. These signals may include:

Identifying these patterns early allows organizations to intervene before accounts become severely delinquent.

Analytics helps rank accounts based on repayment probability and behavioral indicators. Collections teams can prioritize accounts using signals such as:

This approach helps teams focus on accounts most likely to respond.

Analytics also reveals how consumers respond to different communication channels. Data insights can help determine:

Understanding these patterns improves outreach effectiveness.

Analytics supports more targeted campaign planning by analyzing key performance indicators such as:

These insights help refine outreach strategies and improve recovery outcomes.

Analytics insights can guide the design of more accessible repayment options, including:

These tools allow consumers to review balances, set up payment plans, and resolve accounts without waiting for agent assistance.

These capabilities rely on several analytics techniques used in modern credit risk analysis.

Also Read: Reminder Email Templates and Notices

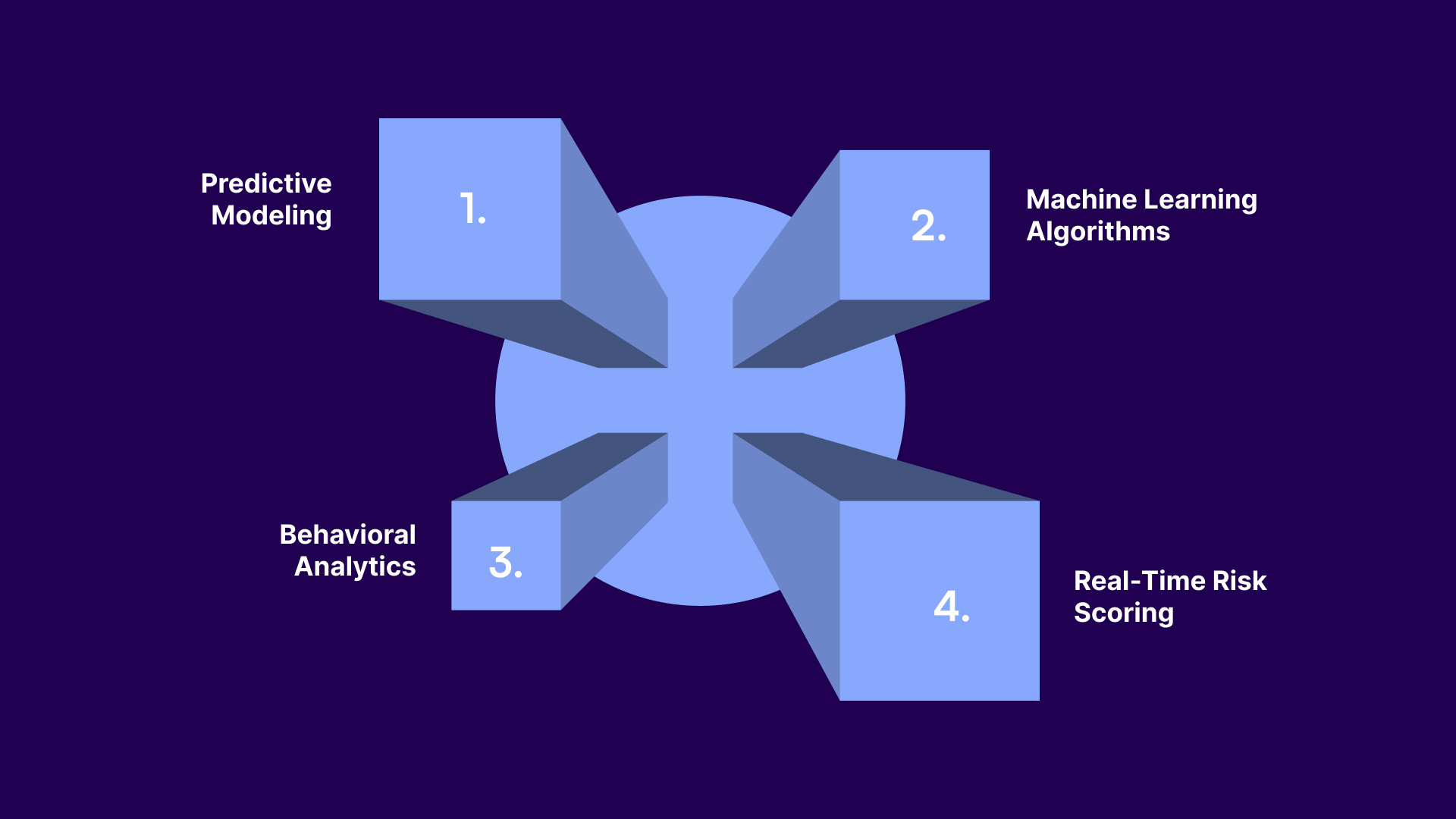

Modern credit risk management relies on several analytics techniques to evaluate borrower behavior and support better collections decisions. These methods help organizations identify risk patterns, predict repayment outcomes, and guide recovery strategies.

Predictive models analyze historical borrower data to estimate the likelihood of repayment or default. These models typically evaluate factors such as:

These insights help organizations prioritize accounts and determine appropriate recovery actions.

Machine learning models analyze large datasets to detect complex patterns that traditional statistical methods may miss. Common algorithms used in credit risk analysis include:

Behavioral analytics focuses on how consumers interact with their accounts and communication channels. Key behavioral signals may include:

These signals help organizations better understand repayment intent and adjust engagement strategies.

Traditional credit scores are updated periodically, which can delay risk detection. Advanced analytics platforms update borrower risk profiles continuously as new data becomes available. This enables collections teams to:

When applied consistently, these analytics techniques help organizations improve recovery performance and operate more efficiently.

Also Read: How Optimized Payment Portals Boost Debt Recovery Rates

When advanced analytics becomes part of credit risk management, organizations gain clearer visibility into portfolio performance and borrower behavior. These insights translate into measurable improvements across collections operations.

However, insights alone are not enough. Organizations also need technology platforms that allow teams to apply these insights directly within daily collections workflows.

Modern collections operations rely on digital platforms that connect analytics insights with daily workflows. These platforms combine data analysis, communication tools, and payment systems in a single environment, helping organizations manage recovery efforts more effectively.

A typical digital collections platform includes:

When these capabilities work together, organizations gain better visibility into portfolio performance and consumer engagement. Centralized systems also make it easier to apply analytics insights in real time and adjust outreach strategies as conditions change.

Platforms such as Tratta support this approach by integrating communication tools, secure embedded payment options, and analytics-driven workflows. Rather than acting as a collection agency, Tratta provides technology that helps agencies, law firms, and credit organizations modernize recovery operations while giving consumers convenient ways to resolve their accounts.

With this technology foundation in place, organizations can integrate analytics more effectively into their collections processes.

Adopting advanced analytics in credit risk management requires a structured approach. To generate meaningful insights, organizations must connect data sources, risk models, and operational tools used in daily collection activities.

1. Centralize Data Sources: Collections data often exists across multiple systems. Bringing together repayment history, account activity, and communication records in one environment creates a reliable foundation for analytics.

2. Implement Predictive Risk Models: Predictive models analyze historical and behavioral data to estimate repayment probability and segment accounts by risk level. These insights help guide account prioritization and outreach strategies.

3. Integrate Communication Channels: Analytics insights are most effective when connected to operational tools. Integrating communication channels such as SMS, email, and digital payment portals allows teams to act on recommendations quickly.

4. Monitor Performance Metrics: Organizations should track key indicators such as recovery rates, engagement levels, and campaign results. Monitoring these metrics helps measure the effectiveness of analytics-driven strategies.

5. Refine Strategies Over Time: Analytics models improve as more data becomes available. Regular analysis and adjustments help ensure collections strategies remain accurate and aligned with changing borrower behavior.

As organizations adopt analytics-driven collections strategies, maintaining compliance with regulatory requirements also becomes an important priority.

Also Read: 5 Ways to Use a Debt Collection Management Software for Higher Recovery

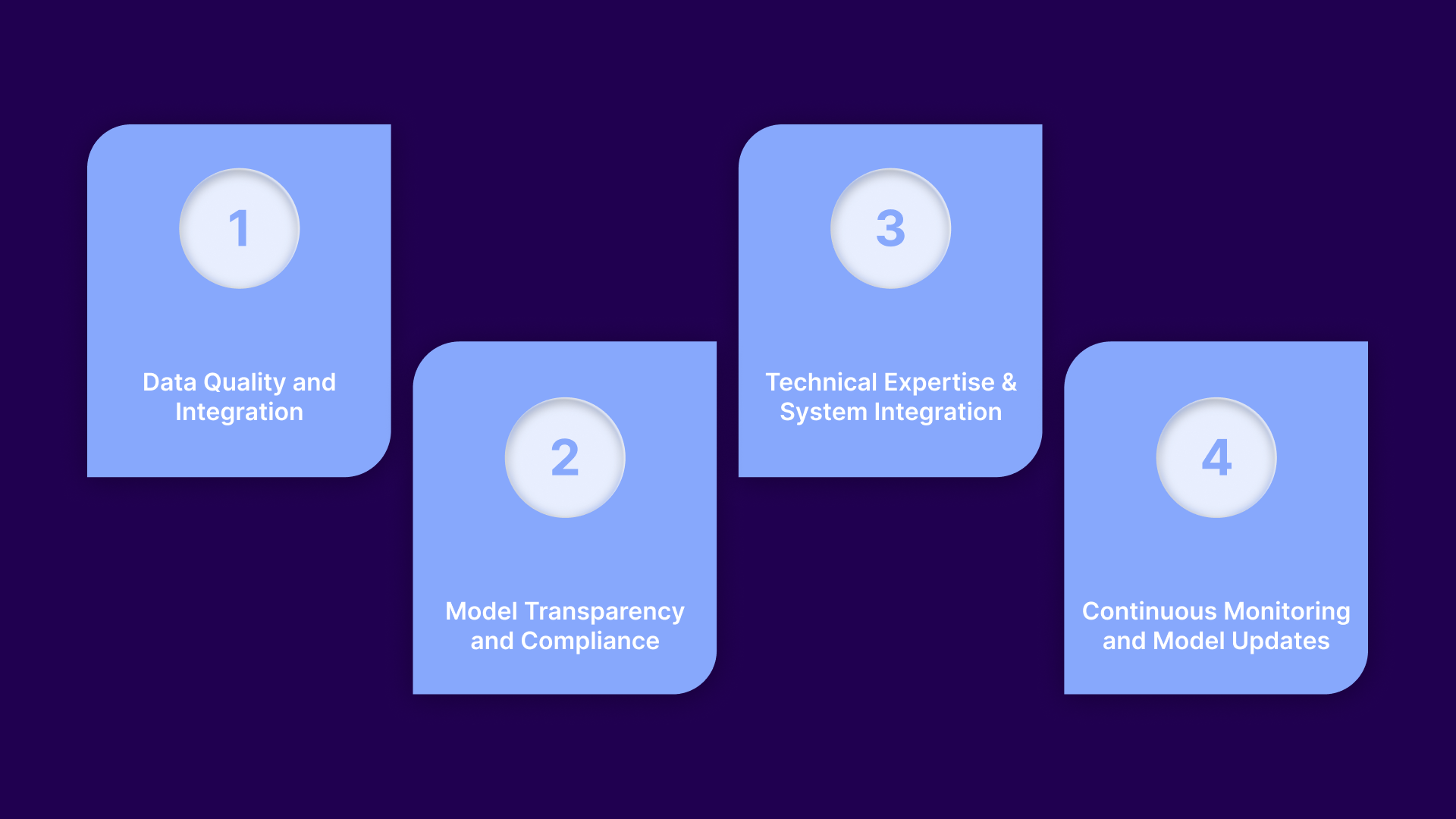

Although advanced analytics offers clear benefits, successful implementation requires careful planning and strong governance. Organizations must ensure that analytics systems are reliable, transparent, and integrated with existing collections workflows.

Analytics models rely on accurate and consistent data. However, collections data is often spread across multiple legacy systems. Consolidating and standardizing these sources is essential for building reliable models.

In regulated environments, organizations must understand how analytics models generate decisions. Explainable models help maintain transparency and support compliance with regulations enforced by agencies such as the Consumer Financial Protection Bureau.

Implementing analytics requires expertise in data science and risk modeling. Systems must also integrate with communication channels, payment platforms, and case management tools so insights can be applied in daily operations.

Predictive models must be regularly reviewed and updated as borrower behavior and economic conditions change. Ongoing monitoring helps maintain accuracy and ensure strategies remain effective.

Despite these challenges, advances in analytics technology continue to create new opportunities for improving credit risk management and collections strategies.

Credit risk analytics continues to evolve as new technologies and data sources emerge. For collection agencies, law firms, and credit issuers, these developments are changing how organizations monitor risk and design recovery strategies.

Together, these developments are driving a shift toward more data-driven and consumer-focused collections strategies.

Advanced analytics in credit risk management helps collection agencies, law firms, and credit organizations detect risk earlier, prioritize accounts more accurately, and guide more effective recovery strategies. When combined with digital communication and payment systems, these insights help organizations operate more efficiently while giving consumers flexible and convenient ways to resolve their accounts.

To see how analytics-driven collections work in practice, explore how Tratta’s digital collections platform supports data-informed outreach, secure payment experiences, and modern recovery workflows.

Learn more about Tratta's digital collections platform and schedule a free demo!

Advanced analytics uses statistical models, machine learning, and large datasets to assess borrower risk and repayment likelihood. It helps organizations analyze payment behavior and financial signals to make more informed credit and recovery decisions.

Advanced analytics helps agencies identify accounts with higher repayment potential and prioritize outreach accordingly. It also suggests optimal communication timing and channels, allowing collectors to focus efforts where they are most effective.

Credit risk analytics combines data such as credit bureau reports, repayment history, transaction records, and utility payments. It may also include behavioral signals and economic indicators to improve prediction accuracy.

Machine learning models analyze large datasets to detect patterns related to repayment behavior and financial stress. These models can update risk scores dynamically and help organizations identify potential defaults earlier.

Digital platforms connect analytics tools, communication channels, and payment systems in one environment. This integration helps organizations monitor account performance, automate risk scoring, and offer consumers secure self-service payment options.