Your autodialer just ran a campaign across 8,000 accounts. One consent record was incomplete. Not 8,000. One. Under the TCPA, that single gap, if it affected even a fraction of those contacts, can produce statutory exposure of $500 to $1,500 per violation. The math is not hard. The outcome is.

Debt collection sits at the intersection of every condition that makes TCPA exposure multiply: high outreach volume, purchased portfolios with incomplete consent histories, automated tools that do not share compliance data, and a plaintiff's bar that has made TCPA class actions one of the most financially attractive areas of consumer litigation in the country.

A TCPA settlement occurs when those conditions go unmanaged long enough for someone to notice. This guide tells you what one is, what it costs, and where your operation is most likely to be exposed right now.

A TCPA settlement is a legal agreement in which a business accused of violating the Telephone Consumer Protection Act resolves the claim by compensating affected consumers instead of going to trial. These cases typically involve unauthorized calls or text messages made using automated systems or without proper consent.

Consumers can file individual claims or join class action lawsuits when communication practices do not comply with TCPA rules. If the parties reach an agreement outside of court, the outcome is a settlement.

In practice, a TCPA settlement reflects breakdowns in the execution of communication workflows. Missing or unclear consent records, failure to honor opt-outs, and outdated contact data are among the most common causes.

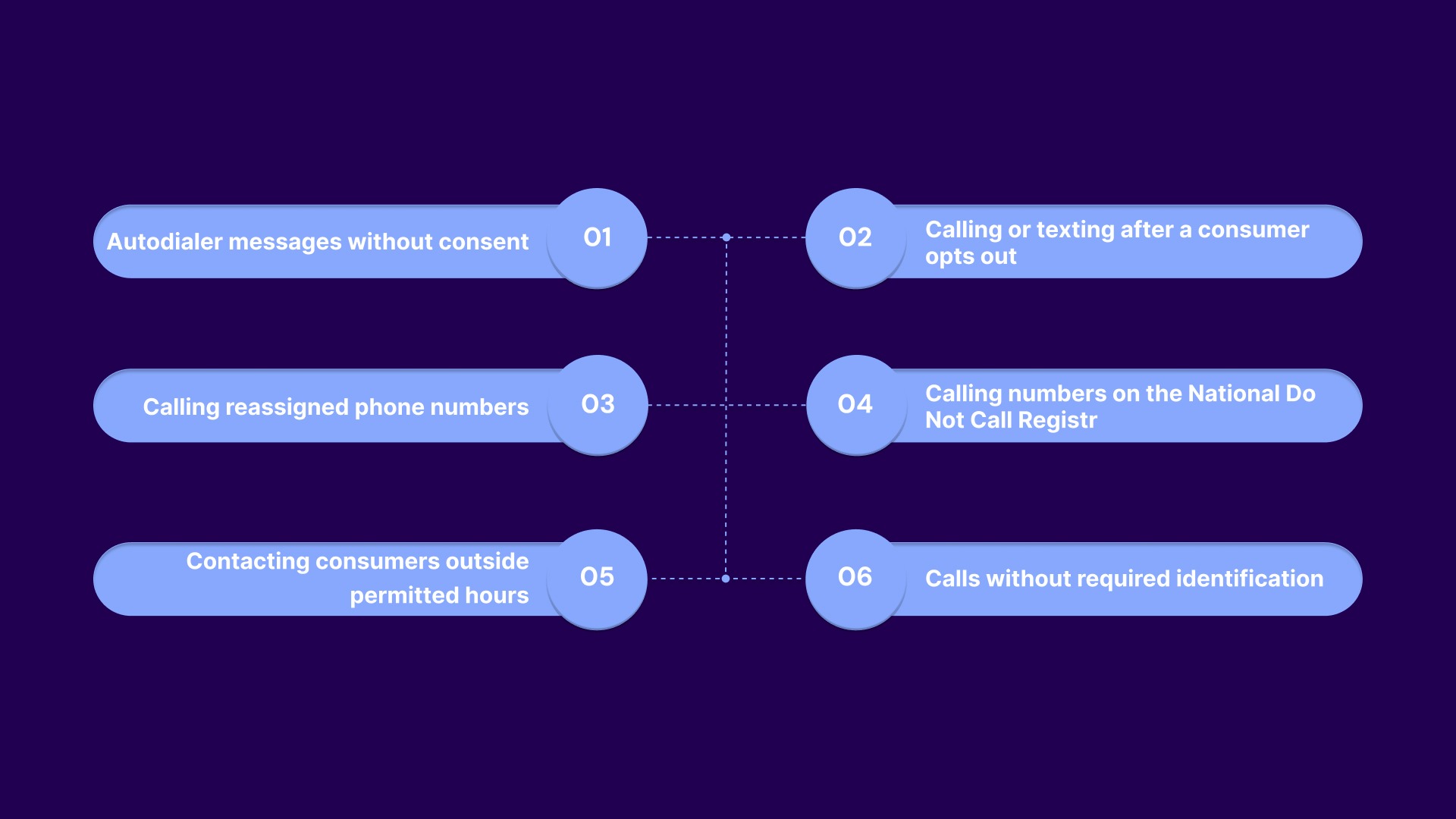

A claim does not require intent. TCPA liability is strict, meaning even an accidental violation, a wrong number, an unverified consent record, or an opt-out that did not propagate can carry the same per-violation damage as a deliberate one. These are the triggers that generate the most claims in collection operations.

Any call or text made using automated dialing technology or a prerecorded voice to a mobile phone requires prior express consent from the person being contacted. In collection workflows, this becomes a problem when contact records include a phone number but lack documentation of when, how, or whether consent was given, or when consent was given for one type of contact but not another.

Practical issue for your operation: Consent obtained at the time an account was originated may not cover SMS outreach. Prior express consent covers informational calls; prior express written consent is required for marketing messages. The distinction matters, and it is frequently missed.

When a consumer asks to stop receiving calls or texts, that request must be honored across all outreach channels within 10 business days, under FCC rules that took effect in April 2025. If your SMS platform and your dialer do not share opt-out data, the consumer may continue receiving outbound contact after a valid revocation request.

Every contact after a valid opt-out is a separate violation. In a high-volume operation, that is not one claim. It is potentially one claim per account that continued to receive outreach after the revocation.

Phone numbers are reassigned frequently. A number your system associates with an account holder from 18 months ago may now belong to someone else. Calling that number with an autodialer is a TCPA violation regardless of the consent the original account holder provided.

For debt buyers specifically, Purchased portfolios carry this risk most heavily. You are working with contact records you did not originate, and the consent history for those numbers may be incomplete or entirely undocumented.

The TCPA requires calling lists to be checked against the National DNC Registry at least every 31 days. Failure to maintain this, or failure to maintain an internal DNC list that is kept current, is one of the more operationally preventable violations and one of the more common ones cited in enforcement actions.

Automated calls and texts are prohibited before 8 AM and after 9 PM in the recipient's local time zone. Using the agency's time zone rather than the consumer's is a compliance gap that affects anyone running multi-state outreach. Every contact outside that window is a separate violation.

Prerecorded messages must identify the calling organization at the beginning. Missing this element, even in an otherwise compliant workflow, constitutes a violation.

Suggested Read: Understanding the TCPA Statute of Limitations and Changes in Regulations

The cost of a TCPA settlement depends on three things: the number of violations, whether they are classified as willful, and whether the claim is individual or a class action. Here is what those numbers look like in practice.

The danger for collection operations is not the per-violation cost. It is that automated outreach at volume means a single compliance gap replicates across every account in the campaign before it is caught.

Statutory exposure based on TCPA damage ranges. Actual settlement amounts vary by the facts of each case, class certification, willfulness determination, and negotiation. This is not legal advice.

Individual TCPA settlements average $5,000 to $12,000 per claimant, according to TCPASettlements.com 2025 data. Most defendants settle to avoid the cost of litigation, not because the claim is necessarily strong.

Class actions represent fewer than 5% of TCPA filings but account for the largest outcomes. A single defective campaign touching tens of thousands of accounts can produce a class that generates exposure far exceeding the operation's annual revenue.

Taking a TCPA case through discovery typically costs $50,000 to $150,000 in legal fees, according to Troutman Pepper's 2025 analysis. Trial preparation adds another $100,000 to $300,000. These costs are incurred before any outcome, win or lose. For most operations, they make a settlement rational at almost any dollar amount.

Collection teams running high-volume outreach manage TCPA exposure across every campaign they run. Tratta's Consumer Self-Service Platform is designed to reduce the volume of outbound contacts your team needs to initiate by giving consumers a direct path to manage balances, set up payment arrangements, and resolve accounts without contacting an agent. Fewer outbound contacts means a smaller exposure surface.

Book a demo now to explore more.

Debt collection is one of the top industries targeted by TCPA lawsuits, reflecting the scale of automated outreach in the sector. In 2025, there were 2,810 TCPA lawsuits filed in U.S. federal courts, according to WebRecon’s year‑in‑review data, with debt‑collection‑related cases making up a substantial share of the total. This is not a coincidence. It reflects the industry's operational structure.

Most industries send automated communications occasionally, in defined campaigns. Debt collection sends them continuously, at high volume, to consumers who did not initiate the relationship. That structural reality creates three compounding risk factors that other industries do not face at the same scale.

Suggested Read: TCPA Rules and Exemptions for Healthcare Providers

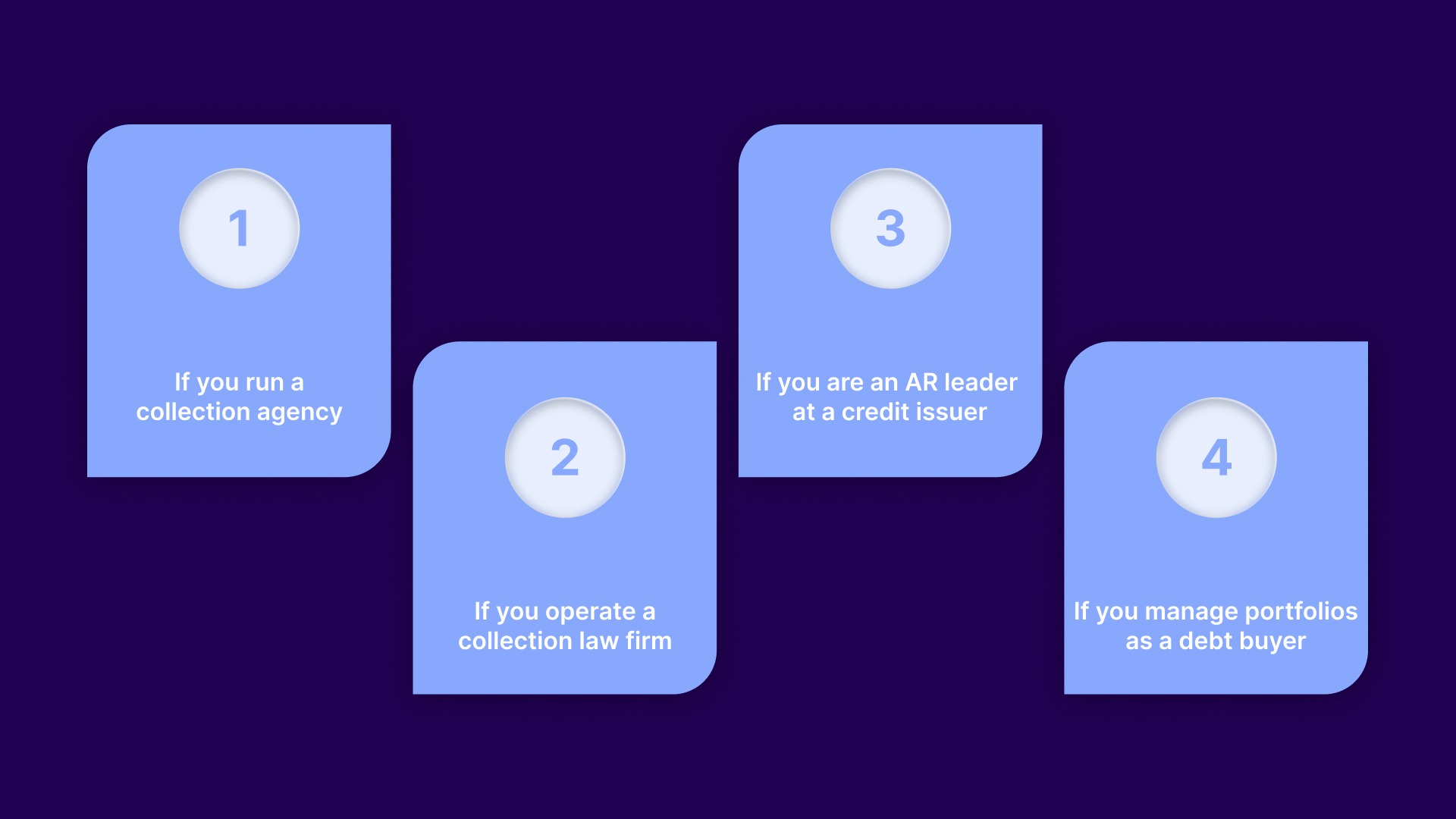

Most TCPA violations in collection operations do not happen because someone decided to ignore the rules. They happen because compliance requirements do not map cleanly onto the way collection workflows are built. Here is where the exposure appears, broken down by what your role in the process actually looks like.

The core issue: Your outreach volume is your TCPA exposure surface. Autodialers, SMS platforms, and account management systems are often separate products that do not share compliance data. Opt-out status recorded in one system is invisible to automated workflows in another. Consent records stored in a CRM do not follow the account into the dialer queue.

If a consumer opts out of SMS contact. Your messaging platform records it. Your dialer does not receive the update. Outreach continues. Each call or text after that opt-out is a separate violation. In a campaign running across 10,000 accounts, if even 2% of those accounts have unsynced opt-out data, that is 200 accounts generating ongoing violation counts until someone notices.

The reporting problem: Without real-time visibility into outreach activity, consent status, and opt-out processing, your compliance team cannot catch a gap until a complaint surfaces. By then, the violation count in that campaign may already be large enough to support class certification.

The core issue: Your exposure sits in two places. If your firm contacts consumers directly, you are subject to the same consent and technology requirements as any other collector. If you use third-party agencies or vendors to contact consumers on your behalf, their violations become your liability.

Documentation and auditability are the requirements that matter most for firm operations. When a TCPA claim is filed, the question is whether you can produce clear, timestamped records of consent for every number that was contacted, and evidence that opt-out requests were honored. If your contact records are scattered across vendor systems, or consent was assumed based on account origination rather than explicitly documented, that defense becomes difficult.

The vendor gap: Firms that place accounts with collection agencies or use third-party dialers need compliance requirements written into those contracts and verified against actual practice. A contract clause does not stop a claim. Documented oversight does.

The core issue: Early-stage recovery outreach, the outreach most likely to preserve the customer relationship, often involves automated SMS or prerecorded calls. That is exactly the outreach TCPA governs most strictly. For credit issuers, a TCPA class action is not just a legal cost. It is a brand event.

Your consumer base has a direct relationship with your brand. TCPA complaints from customers, particularly class actions that become public, affect trust in ways that debt collection agency claims typically do not. The compliance requirement here is tighter in practice because the cost of getting it wrong is higher.

The integrated reporting gap: Credit issuers running recovery through internal teams and external partners often lack a single view of outreach activity, consent status, and opt-out data across all channels. That fragmentation creates the same compliance gaps on a larger scale.

The core issue: When you purchase a portfolio, you inherit whatever consent documentation the previous owner maintained, or failed to maintain. Phone numbers in purchased portfolios may have been reassigned since the original consent was collected. Calling those numbers is a TCPA violation regardless of what the original account holder consented to.

Portfolio recovery performance depends on scalable, controlled outreach. A single TCPA class action based on a purchased portfolio can expose the purchaser to recovery amounts exceeding the portfolio's value. The Rash Curtis case, which resulted in a judgment against a debt collector, is the most direct example of what happens when automated outreach runs against unvalidated contact records at scale.

Suggested Read: National Grid TCPA Settlement over Abusive Automated Calls

Most of these companies had compliance programs in place. The liability usually did not come from a complete lack of compliance, but from operational breakdowns in consent management, number hygiene, vendor oversight, or opt-out handling that were not caught until they had already affected large volumes of calls.

The pattern across these cases is consistent: automation outpaced the compliance controls built to govern it. In each instance, the core issue was less about intent and more about systems' failure to capture consent, consent updates, reassigned numbers, or vendor behavior before calls were made at scale.

The TCPA regulatory environment shifted significantly in 2025. If your compliance approach is based on guidance from more than 18 months ago, parts of it may not reflect current requirements or current legal interpretation.

In 2025, the FCC issued a rule requiring that a consumer's revocation of consent apply to all future communications from the caller on unrelated matters. ACA International and the debt collection industry pushed back, arguing that this conflicts with the FDCPA and creates unworkable compliance burdens. As of April 2026, the rule remains in effect while the industry continues to advocate for reform through the FCC's 'Delete, Delete, Delete' deregulation initiative.

What this means for you: Until the rule is revised or revoked, a consumer opt-out in any channel may apply more broadly than your current workflow assumes. If you rely on a narrow interpretation of revocation, your opt-out processing may not be compliant with current FCC guidance.

In January 2025, the Eleventh Circuit struck down the FCC's rule requiring one-to-one consent, finding the FCC had exceeded its statutory authority. This removed a compliance requirement scheduled to take effect in January 2025, but it did not eliminate the underlying consent obligations under the TCPA.

What this means for you: Consent must still be valid under the statute's existing standards. The vacating of the FCC rule removed one specific restriction but did not loosen the fundamental requirement for prior express consent before automated contact.

A 2025 Supreme Court decision changed how TCPA cases are interpreted, giving individual courts more authority to set their own standards rather than deferring to FCC guidance. This means that compliance that passed muster under a single FCC interpretation may now be evaluated differently depending on the circuit in which a claim is filed.

What this means for you: Geographic concentration of your accounts matters more than it used to. Operations concentrated in Florida, California, and Illinois, which lead state-level TCPA litigation and have plaintiff-friendly court environments, carry more exposure than those in jurisdictions with more defense-friendly precedent.

As of April 2025, the FCC requires that opt-out requests be honored within 10 business days across all channels. This is the operational rule that most frequently creates exposure in operations where dialer and SMS platforms do not share data.

Suggested Read: TCPA Compliance Guide for SMS Text Messages

Reducing TCPA exposure does not require fewer calls or lower recovery targets. It requires building compliance into how outreach operates rather than layering it on after the fact. These are the controls that matter most for collection operations running at volume.

Consent documentation needs to be timestamped, channel-specific, and stored in a format that is searchable and producible in legal review. If consent was collected verbally or noted informally, it cannot be defended under TCPA. Every number in an automated outreach queue should have a consent record that can be retrieved and produced on demand.

For debt buyers: Make consent documentation a diligence item in every portfolio purchase. If the seller cannot provide records of how and when consent was obtained for mobile numbers in the portfolio, those numbers carry elevated risk in any automated outreach campaign.

Phone numbers change owners regularly. Before any automated campaign runs, numbers in the queue should be validated against reassigned number databases and updated contact information. Running campaigns with unvalidated data is the most preventable source of wrong-number violations and one of the most expensive.

Opt-out synchronization cannot be a manual downstream step. If your SMS platform and your dialer are separate products, an opt-out received in one must propagate to the other automatically. Under current FCC rules, this must happen within 10 business days. Real-time synchronization is the more defensible operating standard.

The TCPA requires this. It is also one of the more operationally straightforward requirements to maintain. Missing this step is documented in enforcement actions because list management, when handled manually or inconsistently, falls behind.

If a vendor contacts consumers on your behalf, their violations are your exposure. Contract language is not sufficient. You need documented verification that your vendors are running DNC scrubs, validating consent, checking reassigned numbers, and honoring opt-out requests before outreach runs on your accounts.

Every contact your team initiates is a TCPA exposure point. Every contact a consumer initiates is not. Consumer self-service platforms, digital payment portals, and inbound IVR options give consumers a path to resolve accounts without requiring your team to contact them. Lower outbound contact volume reduces TCPA exposure without reducing the opportunity for account resolution.

If your current setup has your dialer, SMS tool, and CRM operating as separate systems, opt-out synchronization is likely your highest compliance gap. Tratta centralizes communication workflows and account data on a single platform, so opt-out status, consent records, and outreach history are visible across your operation rather than siloed by tool. That is the foundation of manageable compliance at scale.

Schedule a demo to see how it can work for you.

Suggested Read: Understanding TCPA Express Consent for Debt Collection Calls

Tratta is debt-collection software designed for collection agencies, law firms, credit issuers, and debt buyers. It replaces disconnected legacy systems with one platform for consumer payments, digital communications, reporting, and compliance-aware recovery workflows.

Here is how Tratta's features connect to the operational controls that reduce TCPA settlement risk:

Consumers can resolve accounts, set up payment plans, and make payments without contacting an agent. This reduces outbound volume and limits the number of exposure points.

Communication activity is centralized across channels, with consistent enforcement of consent and opt-out rules. Updates in one channel apply across the entire operation.

Integrated payment processing reduces the need for follow-up calls and texts, lowering exposure during the payment stage.

Dashboards provide visibility into outreach activity and workflow performance, helping teams identify gaps before they escalate into compliance issues.

Inbound IVR allows consumers to complete transactions independently, reducing reliance on outbound automated contact.

Tratta connects with existing systems to maintain consistent consent, opt-out, and account data across the technology stack, reducing fragmentation and improving control.

At scale, outcomes are determined by how consistently your systems apply the rules your team already understands. The gap is rarely knowledge. It is execution across data, tools, and workflows.

Teams that build those controls into their operations can scale outreach with confidence, rather than managing risk by limiting activity.

Tratta supports this by unifying communication, payments, and compliance workflows so controls are applied consistently without adding manual overhead.

To reduce TCPA settlement risk while maintaining recovery performance, book a demo and move from policy to enforced workflows across every account.

A: Treat every number as needing documented, channel‑specific consent, validate it before each campaign, and sync opt‑outs across dialer, SMS, and CRM in real time.

A: Yes; TCPA covers non‑marketing autodialed or prerecorded calls to mobile numbers as long as prior express consent is not properly obtained and documented.

A: Reassigned‑number lists should be checked before each campaign; DNC‑list scrubbing every 31 days remains the minimum operational standard.

A: Yes; if a vendor violates TCPA while contacting consumers on your behalf, your organization is still liable, so contracts and audits are required.

A: Yes; inbound or self‑service interactions are not TCPA‑covered outreach, so shifting volume there reduces exposure without lessening recovery.