If your operations touch Florida phone numbers, you are already working under one of the most demanding state telemarketing laws in the country. Florida's mini-TCPA, formally known as the Florida Telephone Solicitation Act (FTSA), Fla. Stat. § 501.059, imposes stricter rules on automated calls, consent, calling hours, and call frequency than the federal Telephone Consumer Protection Act (TCPA) does.

For collection agencies, law firms, credit issuers, and debt buyers managing Florida accounts, these rules are not background reading. They shape how you build outreach workflows, what your dialing systems need to enforce, and where class-action exposure is most likely to arise.

This guide covers what the FTSA actually says, how it changed in 2023, where the debt collection exemption holds and where it does not, what violations cost, and what your team needs to do differently when working Florida portfolios today in 2026.

The Florida Mini-TCPA, formally the Florida Telephone Solicitation Act (FTSA), is a state law that regulates telephonic sales calls to Florida consumers.

It applies to calls, text messages, and voicemail transmissions made to Florida residents or to phone numbers with a Florida area code, regardless of where the caller is located.

The law is triggered by what qualifies as a “telephonic sales call,” defined as any communication made to sell goods or services, extend credit, or collect information for future solicitation.

For debt collection, communications made solely to recover an existing debt are generally outside the scope of the FTSA. However, if any solicitation element is included, the communication may be treated as a telephonic sales call and become subject to the law.

The FTSA took effect in 2021 and was amended in 2023 to clarify definitions and narrow its application.

Both the federal TCPA and Florida's FTSA restrict automated consumer contact. But the FTSA is stricter in a few areas that matter directly to collection operations. Knowing where these gaps sit is where most compliance errors occur.

One practical note on time zones: Florida spans Eastern and Central time zones. If your dialing system applies a single statewide time cutoff rather than the consumer's local time zone, calls to the Florida Panhandle placed at 8:15 p.m. Eastern are likely landing in Central time and fall outside permitted hours. Your system needs to resolve this at the account level, not the state level.

Suggested Read: Statute of limitations, Florida

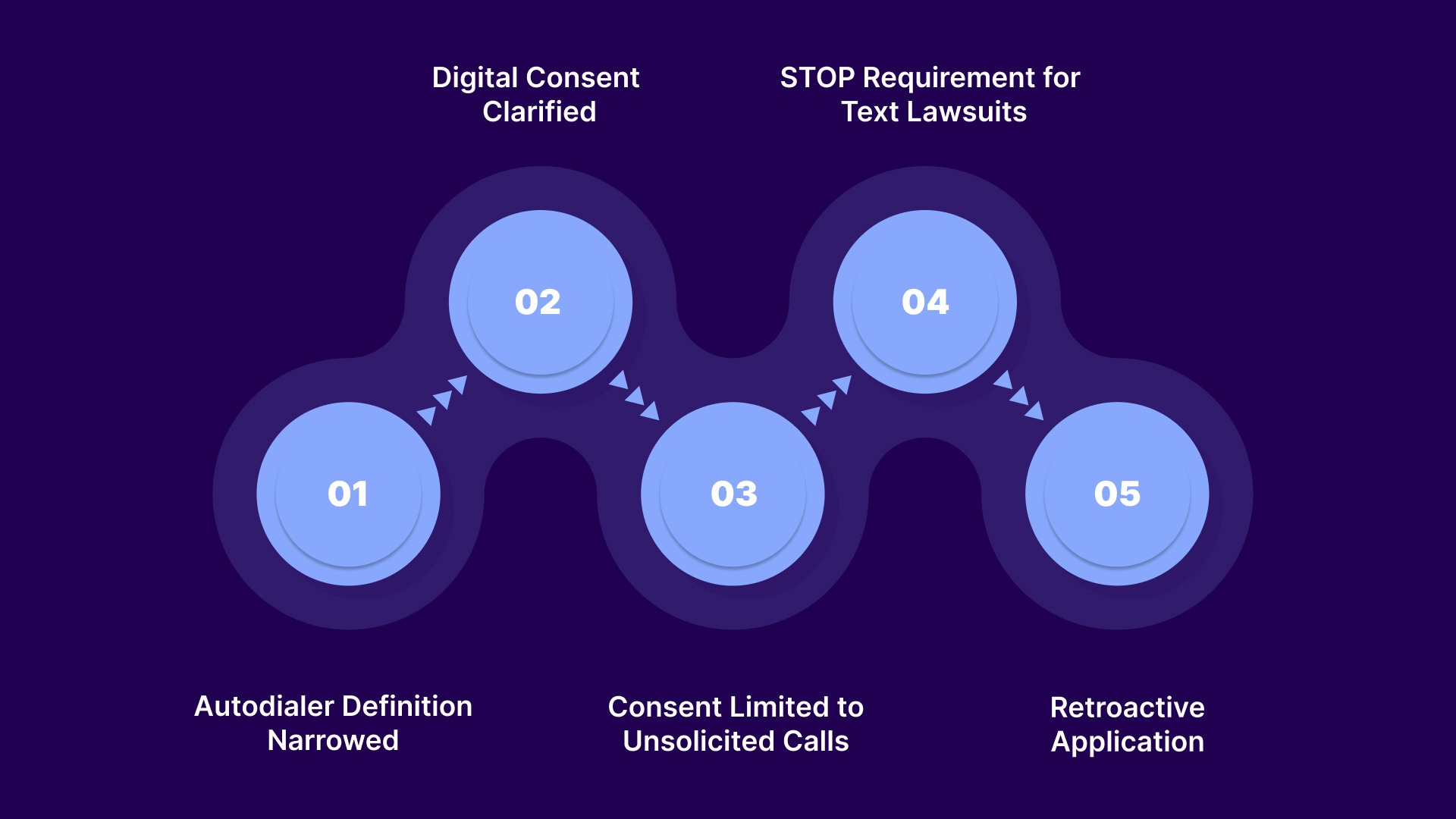

Florida amended the FTSA through HB 761 (effective May 25, 2023) to narrow the scope and reduce litigation exposure while retaining core compliance requirements.

1. Autodialer Definition Narrowed: The law now requires a system to both select and dial numbers automatically. This aligns more closely with the federal standard post-Duguid, though Florida remains broader in scope.

2. Digital Consent Clarified: Prior express written consent can be captured through digital actions such as checked boxes or affirmative text responses, resolving earlier disputes around valid consent methods.

3. Consent Limited to Unsolicited Calls: Consent is required only for unsolicited telephonic sales calls. Communications tied to an existing relationship or initiated by the consumer fall outside this requirement.

4. STOP Requirement for Text Lawsuits: Consumers must first reply STOP before filing suit over text messages. Businesses have a 15-day window to comply, significantly reducing immediate litigation risk for text campaigns.

5. Retroactive Application: The amendments apply to uncertified class actions pending at the time of enactment but do not affect previously filed individual claims.

Operationally, these changes shift focus from broad risk avoidance to precise classification of outreach and stronger consent and suppression workflows.

Managing compliant outreach across Florida accounts is a workflow challenge that requires more than policy awareness. Tratta centralizes consumer communications, consent records, and contact controls in one place, so your team does not have to manage compliance manually across multiple tools. Schedule a demo to watch how Tratta works for collection agencies and law firms.

Suggested Read: Form for Notice of Proposal for Settlement in Florida Rule 1

The FTSA exempts calls made primarily to collect an existing debt or contract that has not yet been completed, as defined under Fla. Stat. § 501.059(1)(k).

In practice, a communication focused solely on collecting an outstanding balance, with no solicitation element, is generally not treated as a telephonic sales call and is not subject to FTSA consent or frequency restrictions.

This distinction becomes critical in real-world outreach. Here is where it breaks down in practice:

If an agent offers a consumer a settlement, a hardship repayment plan, or any new financial product during a collection call, that element can be characterized as solicitation. Keep collection messaging focused on the specific account and avoid bundling promotional language in the same contact.

A collection agency or law firm placing calls on behalf of an original creditor cannot assume that the creditor's exemption status transfers to their outbound activity. The FTSA evaluates the purpose of the specific communication and who is making it. If you are a third party and your call includes any element of solicitation, you are likely within scope.

The FTSA's area code presumption applies to text messages as it does to calls. If you send a text to a Florida area code, Florida law treats that as a contact with a Florida resident unless you can demonstrate otherwise. Text campaigns to Florida consumers carrying any solicitation language require prior express written consent and a clear STOP opt-out mechanism.

The 2021 statute expressly included voicemail transmissions in the definition of telephonic sales calls. Ringless voicemail drops containing any solicitation content sent to Florida numbers are within the scope of FTSA and require the same consent and restrictions as calls and texts.

Suggested Read: Guide to Debt Settlement Agreement Automation Tools in 2026

The FTSA is not the only Florida statute affecting collection outreach. The Florida Consumer Collection Practices Act (FCCPA), codified at Fla. Stat. § 559.55 et seq., runs alongside it and applies specifically to debt collection activity. The two laws have different scopes but overlap in key areas for collection teams.

Note: A May 2025 FCCPA amendment (SB 232, effective July 1, 2025) confirmed that email communications are not subject to the FCCPA's quiet-hour restrictions. This resolved the conflict among court decisions on the issue. Phone calls and text messages to Florida consumers still fall within the 8:00 a.m. to 9:00 p.m. FCCPA window; note this is one hour later than the FTSA's 8:00 p.m. cutoff. Third-party collectors also remain subject to the federal FDCPA's quiet-hour rules, which are applied separately.

Suggested Read: How to Stay Compliant With the Fair Debt Collection Practices Act

Damages under the FTSA are per violation, not per incident. Class actions aggregate those figures across every affected consumer. Here is what that means in practice:

To put that in context: a text campaign that sends 1,000 messages to Florida consumers without prior express written consent and without a functioning STOP opt-out can expose up to $1,500,000 in potential exposure for willful violations alone, before attorney fees or any injunctive action. That number drove hundreds of class actions between 2021 and 2023, before the STOP cure provision was added.

The 2023 amendments introduced the 15-day STOP cure for text lawsuits, which reduced that specific exposure. Call-based violations carry no equivalent cure period; any call violation is immediately actionable without prior notice to the caller.

The full list of FTSA exemptions is set out in Fla. Stat. § 501.059(6) and related provisions. The main categories relevant to financial services and collection operations are:

Suggested Read: Vetting a 3rd Party Collection Agency: What Debt Collection Agency Should Know

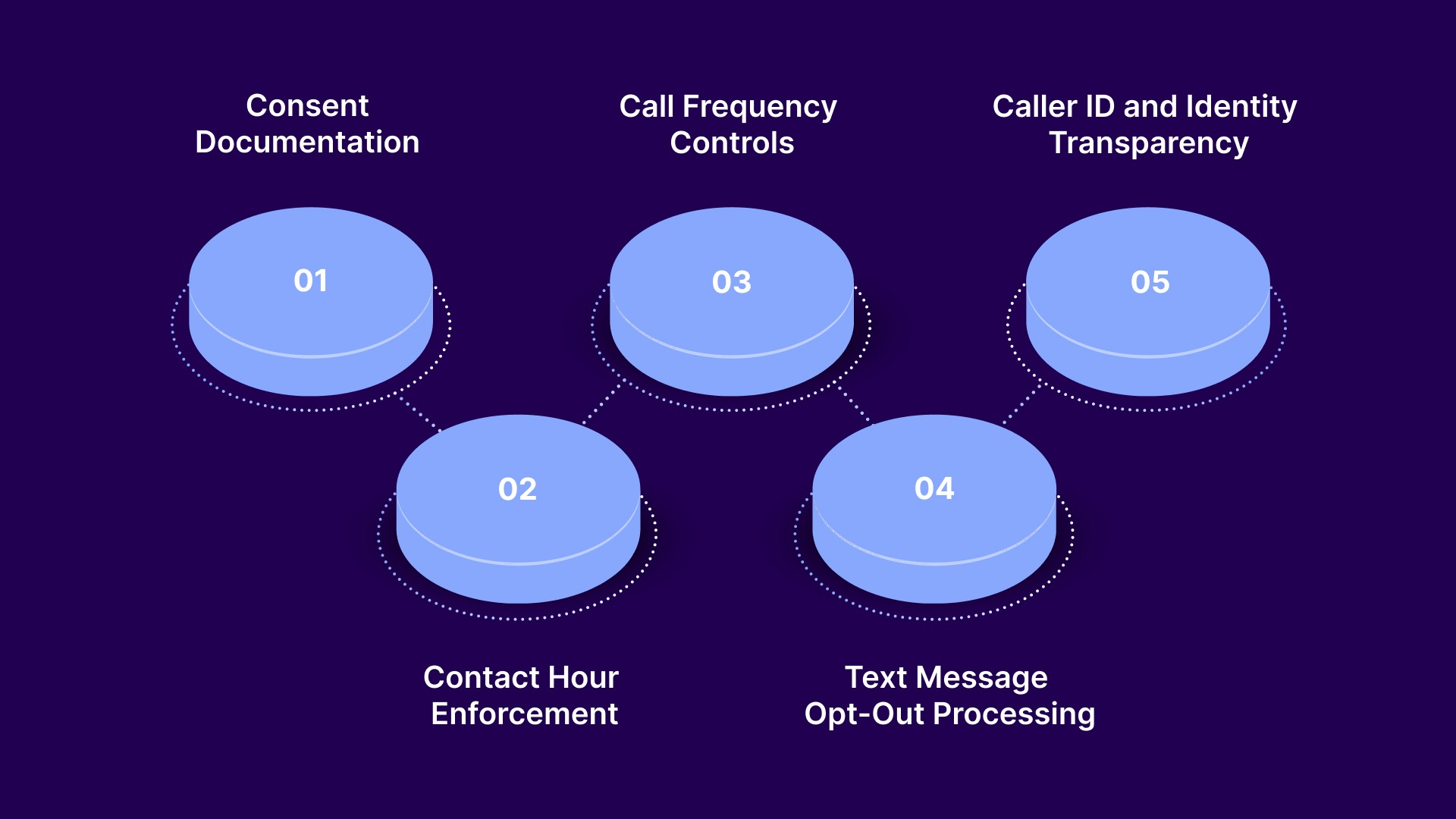

Understanding the rules is the starting point. The harder part is building outreach workflows that enforce them consistently across agents, campaigns, accounts, and vendors. Here is what collection teams managing Florida accounts need to have in place.

Tratta is built for collection agencies, law firms, and debt buyers that need to manage compliant outreach at scale. From embedded payments and omnichannel communications to real-time reporting and configurable workflow controls, Tratta centralizes the tools your Florida operations depend on. Explore the platform and schedule a demo at tratta.io.

Florida's FTSA sits inside a broader federal and state regulatory picture that is shifting. Collection teams working multi-state portfolios need to track both.

In January 2025, the U.S. Court of Appeals for the Eleventh Circuit vacated the FCC's one-to-one consent rule in Insurance Marketing Coalition v. FCC. That rule would have required consent to be tied to a single named company rather than a group of businesses. The vacatur means bundled consent arrangements survive federally. Florida's own prior express written consent requirements under the FTSA remain unchanged and still require consent to be clearly directed at the specific caller.

The FCC's cross-channel revocation rule, which would require a single opt-out request to stop all communications from a caller regardless of account or channel, was delayed to January 31, 2027. The 10-business-day opt-out processing window included in the same order has been active since April 2025. Collection teams should build revocation-tracking systems now, not wait until the 2027 enforcement date.

In response to the FCC's March 2025 'Delete, Delete, Delete' public notice on unnecessary regulatory burden, ACA International formally asked the FCC to eliminate the Revoke-All rule, restore the Established Business Relationship (EBR) exemption for debt collection calls, and resolve direct conflicts between TCPA rules and the FDCPA. As of early 2026, no final action has been taken on these requests, but federal policy is moving toward reducing the TCPA burden for collection-specific communications.

Florida SB 232, which took effect on July 1, 2025, resolved a split among Florida courts by confirming that the FCCPA's quiet-hour restrictions do not apply to email communications. Email to Florida consumers is no longer constrained by the 8:00 a.m. to 9:00 p.m. window that applies to calls and texts. Phone and text restrictions remain fully in force.

Florida continues to generate more TCPA and FTSA litigation than almost any other state. The combination of strict state law, active plaintiff counsel, a large and diverse consumer population, and courts that have been receptive to class certification creates ongoing exposure for any operation that places high volumes of outbound calls to Florida numbers.

If you are managing a Florida portfolio today, work through the tables below. Each checklist is built for a specific audience, so you can see exactly where your operations may have gaps before they become violations.

Most collection teams managing Florida accounts are running compliance across disconnected tools, separate systems for dialing, texting, payments, and consent records. That fragmentation is where gaps form. Tratta is a debt collection software that brings these workflows onto a single platform.

Here is what that looks like for each compliance requirement the FTSA creates.

Gives consumers direct access to their balances, payment options, and account details without calling an agent. Every action is logged automatically with a time stamp.

Records every consumer contact across email, SMS, IVR, and portal in a single account history.

Consumers complete payments inside the platform without being redirected to a third-party tool. Each transaction is time-stamped and instantly linked to the account.

Florida has one of the most linguistically diverse consumer populations in the country. Tratta's IVR supports transactions in multiple languages.

Outreach campaigns can be segmented and configured with rules that enforce FTSA requirements before any contact is made.

Real-time dashboards give operations leaders visibility into contact rates, payment activity, and opt-out patterns across Florida portfolios.

API connections pull account data from creditor systems, law firm platforms, and CRM tools into a single view, removing the manual transfers where errors in consent records or area codes most often occur.

Tratta does not guarantee compliance outcomes and does not replace legal counsel. What it does is give your team the operational infrastructure to consistently apply the rules you already know you need to follow, at the scale Florida portfolios require.

Florida's mini-TCPA is one of the more operationally demanding state-level compliance frameworks for anyone managing consumer contact in debt recovery. The 2023 amendments reduced class-action exposure for text-based violations, but the core requirements, consent documentation, contact-hour enforcement, call-frequency caps, and text-opt-out controls, remain in force and continue to generate litigation.

For collection agencies, law firms, credit issuers, and debt buyers, getting Florida right is an execution problem as much as a legal one. You need systems that enforce the rules your compliance team sets, consistently document consumer interactions, and give your operations leaders the visibility to catch patterns before they become violations.

Tratta centralizes payments, communications, consent tracking, and reporting so that collection teams working Florida portfolios have the operational infrastructure the rules actually require. If your current tools are forcing your team to manage FTSA compliance manually, schedule a demo today.

Yes. FTSA applies to calls or texts made to Florida area codes, regardless of the consumer’s actual location, unless you can prove the recipient is not in Florida.

Not always. Even manually dialed calls can fall under FTSA if they qualify as telephonic sales calls, meaning the purpose of the communication, not the dialing method, determines applicability.

No. Consent must be specific and clearly tied to the communication type and sender. Broad or bundled consent may not meet the FTSA standards for unsolicited telemarketing calls.

If consent cannot be produced, the burden shifts to the caller. Lack of documentation significantly increases liability risk and weakens defense in FTSA-related claims or audits.

Yes. Vendors create additional exposure if their systems fail to enforce consent, timing, or opt-out rules. You remain responsible for compliance across all outsourced outreach activities.