Debt settlement often fails because settlement opportunities do not scale. Thousands of eligible accounts never see an offer, agreements stall after acceptance, and first payments are missed because execution depends on manual follow-up.

This pressure to handle settlements at volume is reshaping the industry. The global debt collection software market is projected to reach USD 6.56 billion in 2026, growing at a 9.72 percent CAGR. This signals a clear shift toward automation built for throughput, consistency, and execution at scale.

In this guide, we examine how debt settlement agreement automation tools support high-volume settlement workflows in 2026, what capabilities actually matter, and how automation turns intent into completed recoveries.

Quick look:

Debt settlement agreement automation tools are systems designed to present, manage, and execute settlement options at scale, without relying on one-to-one agent negotiation. Instead of treating settlements as standalone legal documents, they focus on automating the process of moving settlement opportunities from offer to payment.

In practice, these tools are needed because they:

As portfolios grow and manual workflows break under volume, these capabilities shift settlement from a bottleneck into a scalable recovery channel.

Suggested Read: Automated Debt Settlement: What It Is And How It Works

Manual debt settlement processes are breaking down under rising delinquency volumes. According to the Federal Reserve Bank of New York, overall delinquency rates remained elevated in recent reports, with aggregate serious delinquency (90+ days past due) rising across multiple debt types.

As more accounts enter delinquency, agent-led settlement workflows struggle to keep up, exposing structural weaknesses that were manageable at a lower scale but are costly now.

They typically break down because:

These limitations are why settlement agreement automation tools prioritize certain core features. The following section explains these in detail.

Suggested Read: Understanding Debt Settlement Law and Procedures

The right capabilities reduce agent dependency, improve conversion after agreement, and lower operational risk across large portfolios.

These are the core features you should look for:

Automated settlement offer logic uses predefined rules to determine eligibility and settlement terms across large account volumes. This removes agent-by-agent decision-making and ensures settlement offers are applied consistently across portfolios. As volume increases, rules-based logic prevents bottlenecks caused by manual review and approval.

This helps collection agencies by:

Digital settlement presentations deliver offers through self-service portals or automated channels rather than relying solely on phone calls or emails. This ensures settlement options are visible even when agents are unavailable or consumers do not answer calls. Digital access allows consumers to review terms on their own timeline, increasing engagement.

This feature helps collection agencies by:

Self-service acceptance allows consumers to confirm settlement terms without agent intervention. This removes delays between intent and commitment, which is where many settlements fail. Faster acceptance also reduces the need for repeated follow-ups.

This capability helps collection agencies by:

Payment execution automation connects settlement acceptance directly to payment setup. Whether lump sum or payment plan, the system initiates payments immediately after agreement. This minimizes the risk of drop-off between acceptance and the first payment.

This helps collection agencies by:

Compliance controls ensure the system enforces settlement disclosures, timing, and documentation. Every action related to a settlement is recorded automatically. This creates a defensible record without relying on manual notes or spreadsheets.

This feature helps collection agencies by:

Tratta supports settlement agreement automation by focusing on high-volume execution. It enables automated settlement offer presentation through self-service channels, allows consumers to accept terms digitally, and connects those agreements directly to payment workflows.

McKinsey research shows that organizations shifting to digital-first collections can reduce collections operating costs by at least 15%, largely by moving activity away from labor-intensive processes and into automated, self-service execution.

Settlement automation is less about fixing what is broken and more about unlocking operational leverage. Investing in automation delivers benefits that manual processes cannot provide at scale:

These benefits shift the conversation from efficiency to capacity. The next section explains the signs that it may be time to move away from manual settlement workflows.

Suggested Read: How Settlement Accounts Appear in Collections: What Agencies Need to Know

Manual settlement processes usually fail quietly. Instead of a single breaking point, agencies experience gradual operational strain that becomes visible across volume, outcomes, and internal effort.

The table below highlights common warning signs and what they indicate at an operational level.

Tratta helps address these warning signs by removing settlement execution from agent-dependent workflows. It standardizes how settlement offers are presented, accepted, and converted into payments. Agencies can absorb higher settlement volumes without increasing administrative load or losing visibility into outcomes. Schedule a free demo.

Many platforms automate isolated steps while leaving execution gaps that agencies still have to manage manually. Asking the right questions helps separate tools built for scale from those built for limited use cases.

Key questions to ask include:

It is important to understand the practical limits of settlement agreement automation before setting expectations or committing to a tool. These limitations are explained in the next section.

Suggested Read: How to Write a Letter for Settlement of Disputed Debt

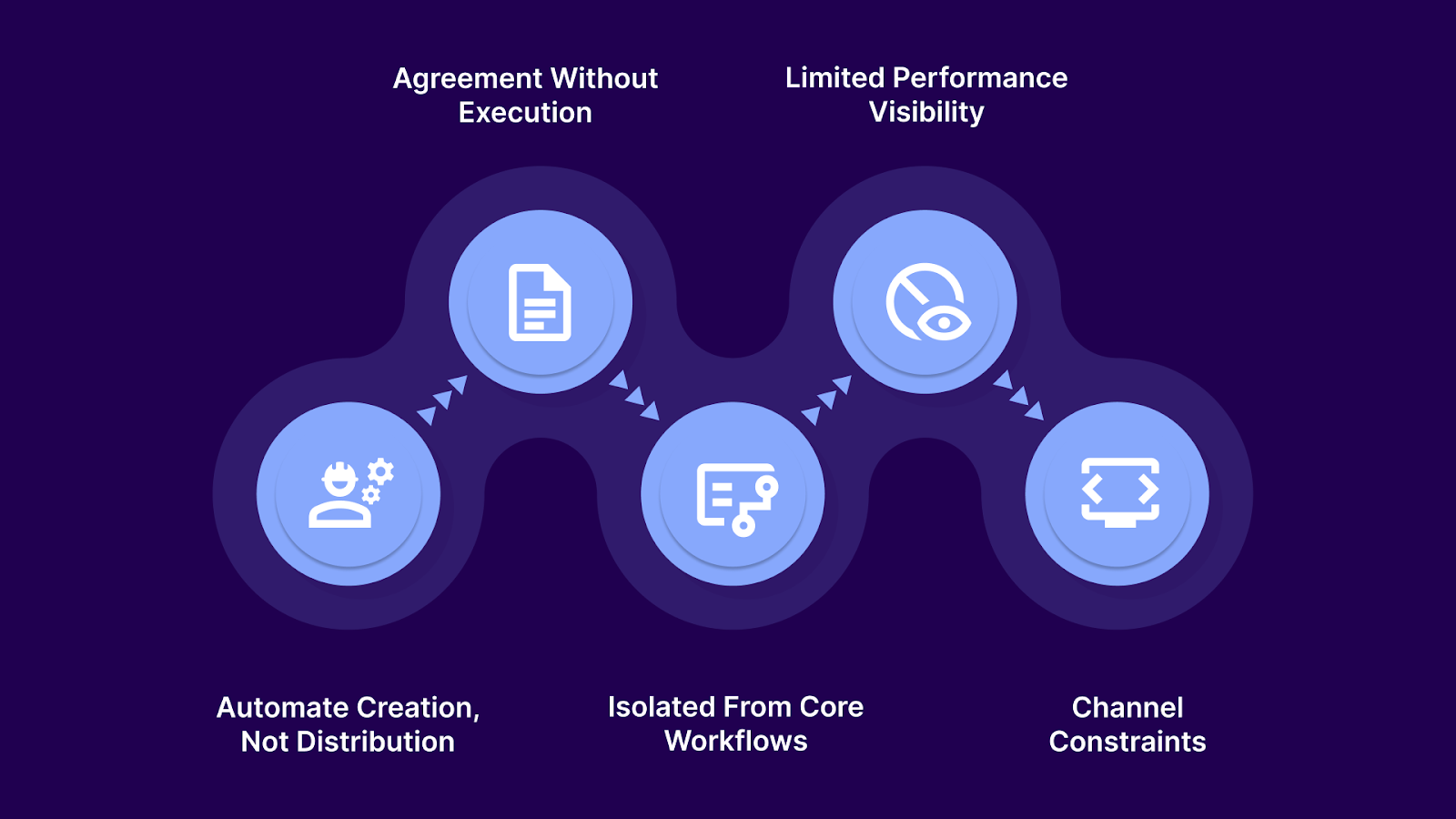

Settlement agreement automation tools often solve a narrow part of the workflow. While they can standardize how agreements are created or stored, many stop short of supporting what actually drives recovery at scale: delivery, follow-through, and execution across channels.

Common limitations include:

These gaps explain why agencies increasingly look beyond point solutions. To manage settlement volume effectively, they need platforms that connect settlement logic to delivery, payment execution, and reporting within a broader collections workflow.

Suggested Read: How Collection Agencies Evaluate and Accept Settlement Offers

Tratta is a modern, all-in-one debt collection platform that helps agencies automate and scale cash recovery across large portfolios. It replaces siloed tools and manual handoffs with a unified system that connects consumer engagement, communication, payments, analytics, and compliance. By bringing these capabilities together, agencies can boost recoveries, reduce operational friction, and increase consistency across workflows.

Tratta’s portal gives consumers a secure, branded space to view balances, settle debts, and choose payment options directly. It supports flexible payment and settlement choices so consumers can resolve their accounts without agent dependency. This increases consumer engagement and reduces inbound workload for agencies.

Real-time dashboards and reports allow agencies to track recovery performance, segment results, and make data-driven decisions. These analytics surface trends in consumer behavior and payment outcomes to help refine strategies. By eliminating manual reporting, teams spend less time gathering data and more time acting on insights.

Tratta’s inbound IVR supports payments in multiple languages, widening access for diverse consumer populations. Consumers can verify accounts and make payments over the phone, with activity reflected instantly in reporting. This broadens channel coverage without adding agent burden.

The platform enables automated outreach via email, SMS, and other digital channels to deliver settlement and payment messages. Reaching consumers where they prefer increases the likelihood of engagement and action. Agencies benefit from a consistent communication strategy that does not depend on manual sending.

Agencies can run intelligent campaigns with custom segments, smart scheduling, and automated triggers. These campaigns help drive specific behaviors, such as settling accounts or setting up payment plans. This automation increases throughput while reducing manual campaign management.

Embedded payment processing allows consumers to pay directly within the portal or via other digital channels. This seamless integration accelerates payment collection and reduces reconciliation effort. Agencies see improved cash flow and fewer errors from disconnected systems.

Tratta’s admin console lets agencies tailor messaging, branding, payment options, and workflows to fit their business rules. This flexibility ensures that the platform adapts to operational preferences rather than forcing agencies to conform. Customized workflows increase adoption and effectiveness.

Robust REST APIs and system integrations allow Tratta to connect with existing collections, CRM, or financial systems. This seamless connectivity keeps data synchronized across tools and removes manual data entry. Agencies avoid fragmentation and preserve end-to-end workflow coherence.

Tratta’s platform is built with strong security protocols and compliance-by-design features to protect data and enforce regulatory requirements. Dynamic notices and disclosures can be applied based on consumer profile, location, and transaction type. This reduces compliance risk while simplifying audits and regulatory reporting.

Tratta changes how agencies think about settlement altogether. Instead of treating settlements as exceptions that require extra effort, it makes them a repeatable, system-driven outcome across portfolios.

Choosing the wrong settlement agreement automation tool creates quiet but compounding problems. Point solutions that stop at agreement creation leave agencies managing delivery gaps, payment delays, disconnected reporting, and rising administrative overhead as volumes grow.

Tratta moves settlement automation beyond isolated steps and into end-to-end execution. By connecting settlement presentation, execution, analytics, and compliance within a single platform, agencies can process higher delinquency volumes with control and consistency.

If settlement volume is increasing, your tools must scale with it. Speak to us to learn how you can turn settlement intent into completed recoveries at scale.

No. While volume makes the impact more visible, automation benefits any agency that wants consistent execution, fewer manual handoffs, and better conversion from agreement to payment.

No. These tools reduce administrative and follow-up work, allowing collectors to focus on exceptions, disputes, and higher-risk accounts rather than routine settlement execution.

They reduce drop-off by connecting settlement acceptance directly to payment execution, minimizing delays, missed follow-ups, and manual errors after agreement.

Yes, when built correctly. System-enforced disclosures, logged consumer actions, and audit-ready records reduce reliance on manual documentation and lower compliance risk.

Tratta connects settlement logic, delivery, payment execution, reporting, and compliance within a broader collections platform, rather than automating only one isolated step.