A poorly structured collection workflow can turn attorney letters into operational and compliance risks instead of effective recovery tools. For collection law firms, even minor issues such as inconsistent disclosures, weak documentation, or disconnected communication tracking can increase disputes and slow recoveries.

The pressure is growing as well. The CFPB received approximately 207,800 debt collection complaints last year, many tied to written notifications, disputed debts, and collection communications. Collection firms already manage high account volumes, regulatory scrutiny, and rising consumer expectations.

In this article, we will explain what a collection letter from an attorney includes, what practices are off limits, common compliance risks, and how firms can manage attorney letter workflows more efficiently.

A debt collection letter from an attorney is a formal written communication sent by a collection law firm or attorney to recover unpaid debt on behalf of a creditor, debt buyer, or collection agency. These letters are commonly used in third-party debt recovery when accounts move beyond early-stage collection efforts or require additional escalation.

These collection letters are typically used by law firms to support:

In the next section, we will look at when law firms typically send collection demand letters to consumers and what drives the timing behind those decisions.

Suggested Read: Final Notice Letter Examples and Templates

Collection demand letters are formal recovery communications, but they are not automatically lawsuits or legal notices that litigation has already been filed. In many third-party debt collection workflows, these letters are used as part of structured communication sequences before accounts move toward potential legal escalation.

Collection demand letters are commonly sent during the following situations:

Tratta helps collection law firms automate attorney letter workflows through configurable sequencing, centralized communication management, and integrated account tracking. The platform also supports standardized outreach strategies and consumer self-service experiences across third-party debt recovery operations. Schedule a free demo today.

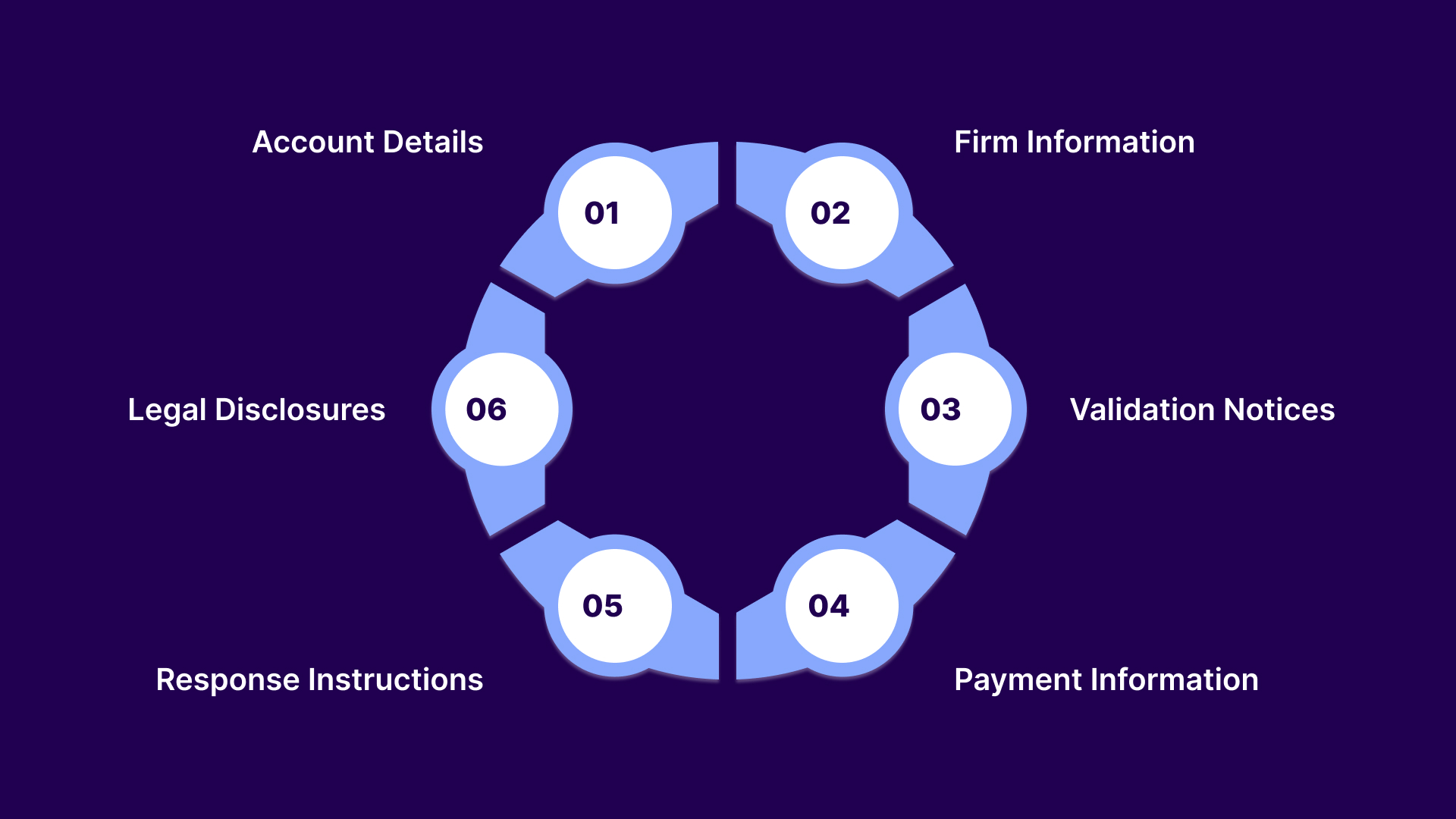

In third-party debt recovery, incomplete or inconsistent letters can create disputes, operational delays, and compliance exposure. These letters commonly include the following components:

Consumers should be able to clearly identify the debt referenced in the communication. Accurate account information also helps reduce disputes and supports more efficient account resolution workflows.

Common account details include:

Attorney collection letters should clearly identify the law firm or attorney responsible for the communication. Some jurisdictions also require licensing, registration, or disclosure information tied to debt collection activity.

Collection law firms commonly include:

Many attorney collection letters must include debt validation disclosures required under the FDCPA, including validation notice requirements under 15 U.S.C. § 1692g and Regulation F. These notices help consumers understand their rights to dispute or request verification of the debt.

Validation sections often contain:

Attorney collection letters often include repayment or settlement options designed to encourage consumer action. Clear payment instructions can reduce operational friction and improve recovery workflows.

These sections may include:

Consumers should understand how to respond after receiving the letter. Clear response guidance can help reduce communication gaps and support more consistent recovery operations.

Response sections may include:

Collection law firms frequently include disclosures tied to attorney involvement, communication requirements, and federal or state debt collection laws. Under the FDCPA, debt collectors must also provide Mini-Miranda disclosures identifying the communication as an attempt to collect a debt.

Legal disclosure sections may contain:

The structure, tone, and regulatory requirements of attorney collection letters can differ significantly from standard collection notices. In the next section, we will compare attorney collection letters vs standard collection notices and explain how their operational roles differ.

Suggested Read: Understanding Debt Settlement Letters in New Jersey

Standard notices are typically used earlier in the collection lifecycle, while attorney collection letters are often integrated into more formal recovery stages involving legal oversight or escalation review. The structure, tone, compliance considerations, and consumer perception of these communications can vary significantly.

Table showing operational differences:

Some additional operational differences include:

Because attorney collection letters involve more structured legal and operational considerations, drafting them requires greater consistency and workflow control. In the next section, we will break down the steps to draft a collection letter for third-party debt and explain how firms can standardize the process more effectively.

Suggested Read: How to Write Effective Debt Collection Letters with Samples

Collection law firms must structure these communications carefully to support recovery objectives while maintaining accurate disclosures, standardized workflows, and compliant communication practices.

When drafting attorney collection letters, focus on the following steps:

Law firms should confirm account balances, creditor details, delinquency records, and consumer information before generating the letter. Incorrect account data can create disputes, compliance exposure, and operational delays during the recovery process. Many firms use centralized account management systems to reduce data inconsistencies across portfolios.

The communication should clearly identify the law firm, attorney involvement, and the party attempting to collect the debt. This helps establish transparency while supporting disclosure requirements tied to third-party debt collection operations. Some jurisdictions may also require licensing or registration information within the communication.

Attorney collection letters often include validation disclosures required under 15 U.S.C. § 1692g and Regulation F. These notices explain consumer rights related to disputes, verification requests, and debt validation timelines. Standardized disclosure templates can help firms maintain consistency across communication workflows.

Collection letters should provide clear repayment instructions and available resolution pathways. Consumers are more likely to engage when payment methods, settlement opportunities, and response channels are easy to understand. Many firms also include self-service payment access within attorney communication workflows.

The tone of the communication should remain professional, factual, and compliant with federal and state debt collection laws. Attorney collection letters should avoid misleading language, unsupported legal threats, or aggressive communication tactics. Standardized review processes can help reduce wording inconsistencies across recovery operations.

Collection law firms operating across multiple jurisdictions often need to include state-specific notices or disclosure language. Requirements may vary depending on licensing laws, consumer protections, and communication regulations. Workflow automation can help firms apply the correct disclosures based on account location and portfolio rules.

Firms should maintain documentation of attorney letters, delivery activity, consumer responses, and workflow actions. Communication tracking supports audit readiness, dispute management, and operational visibility across third-party debt recovery operations. Integrated reporting systems can also help standardize communication records at scale.

Below is a simplified example showing how collection law firms may structure attorney collection letters in third-party debt recovery workflows. Actual communications should be reviewed for FDCPA, Regulation F, client-specific, and state-law requirements before use.

Example:

[Law Firm Name]

[Law Firm Address]

[Phone Number]

[Date]

Re: Account Reference Number: XXXXXXX

Dear [Consumer Name],

Our office is attempting to collect a debt on behalf of [Current Creditor Name] related to the above-referenced account. According to the information currently available, the account balance is $[Amount Due].

Please review this notice carefully. If you dispute the validity of this debt or any portion of it, you may notify our office in writing within the timeframe required by applicable law. Upon receiving a valid dispute request, additional verification information may be provided as required under federal law.

For questions regarding this account or available resolution options, you may contact our office using the information listed above. Payment options, if applicable, may also be available through approved communication channels or payment portals.

This communication is from a debt collector. This is an attempt to collect a debt, and any information obtained will be used for that purpose.

Sincerely,

[Law Firm Name]

Authorized Representative

Because attorney collection letters operate within heavily regulated recovery environments, drafting them correctly is only one part of the process. In the next section, we will examine federal rules and operational risks that collection law firms must account for.

Suggested Read: Best Letter Collection Templates for Faster Debt Recovery

The smallest wording inconsistencies, disclosure failures, or documentation gaps can create litigation exposure, consumer disputes, and regulatory scrutiny.

Some of the most important legal and compliance considerations include:

Attorney collection letters must avoid false, deceptive, misleading, unfair, or abusive communication practices under 15 U.S.C. §§ 1692d, 1692e, and 1692f. The statute also regulates validation notices, consumer disputes, communication practices, and disclosure requirements.

Under 15 U.S.C. § 1692g, debt collectors must provide validation information within the required timelines after the initial consumer communication. Regulation F, codified under 12 C.F.R. Part 1006, further standardizes validation notice requirements and model disclosure formats.

The FDCPA requires debt collectors to disclose that the communication is from a debt collector attempting to collect a debt. These disclosures are commonly referred to as Mini-Miranda warnings and are tied to 15 U.S.C. § 1692e(11). Failure to include proper disclosure language may create compliance exposure.

Attorney collection letters must accurately reflect attorney participation in the communication process. Courts have repeatedly scrutinized letters implying attorney review when no meaningful involvement actually occurred. Collection law firms must maintain documented review workflows and operational controls surrounding attorney communications.

Regulation F establishes additional rules covering electronic communications, consumer preferences, limited-content messages, and communication frequency standards. Collection law firms using digital outreach alongside attorney letters must align workflows with these CFPB requirements.

Collection workflows must properly track disputes, verification requests, cease communication requests, and representation notices. Failure to pause or adjust communication activity after qualifying disputes can create regulatory and litigation risks under federal and state laws.

Maintaining communication records, delivery history, consumer responses, and disclosure versions is critical for audit readiness and dispute defense. Strong documentation practices also help collection law firms demonstrate operational consistency across attorney communication workflows.

Tratta helps legal recovery teams monitor communication activity through centralized reporting, campaign oversight, and audit-focused workflow tracking. The platform also supports more consistent management of disclosures, outreach records, and operational performance across third-party debt collection workflows. Contact us to learn more.

Attorney collection letters must follow strict federal and state debt collection laws governing consumer communications. Violations tied to attorney collection letters can create regulatory scrutiny, litigation exposure, consumer complaints, and operational risk across recovery workflows.

The following practices are generally considered prohibited or high-risk in debt collection letter operations:

Many prohibited collection letter practices are tied to inconsistent workflows, manual processes, and weak communication oversight rather than intentional misconduct.

Poorly managed attorney collection letter workflows can slow recoveries, increase disputes, and create operational inefficiencies across third-party debt collection portfolios. Automation can help collection law firms standardize templates, apply jurisdiction-specific disclosures, maintain audit records, and track communication activity across portfolios more consistently.

Tratta helps collection law firms improve operations through centralized workflow management, configurable campaign controls, communication tracking, reporting visibility, and integrated recovery infrastructure. Its data-driven platform supports audit-ready operations, consumer self-service experiences, and scalable third-party debt recovery processes.

Looking to improve how your firm manages attorney collection letter workflows? Request a free demo today.

Yes, attorney collection communications may be delivered electronically if the workflow complies with the FDCPA, Regulation F, consumer consent requirements, and applicable state laws. Collection law firms often use email alongside letters, SMS, and digital portals within omnichannel recovery strategies.

Retention timelines vary based on client agreements, state laws, regulatory expectations, and internal compliance policies. Many firms maintain communication histories, delivery records, dispute activity, and disclosure versions for audit and litigation defense purposes.

A lawyer collection letter is generally a recovery communication used within third-party debt collection workflows, while a litigation notice is tied more directly to formal legal proceedings or filed lawsuits. Not every attorney collection letter indicates that litigation has started or will immediately occur.

Debt collection emails should include accurate account information, required disclosures, communication preferences, and compliant wording that aligns with federal and state regulations. Law firms should also maintain documentation, consent tracking, and standardized review processes for electronic communication workflows.

Yes, many collection law firms automate portions of attorney communication workflows using standardized templates, communication sequencing, reporting systems, and account segmentation strategies. Automation can help improve consistency, audit visibility, and operational efficiency across third-party debt recovery operations.