Your collection agency has adopted accounts receivable automation to recover debts faster. But when your team discovers that $50,000 in payments hasn’t been posted to the correct accounts and creditors are calling about missing transactions, you realize something is wrong.

According to PYMNTS Intelligence research, automating manual AR processes can reduce collection times by 67%. But speed alone doesn’t guarantee results. When payment posting, balance updates, and reconciliation aren’t accurate, automation amplifies errors instead of eliminating them. Even small gaps in AR automation accuracy can lead to misapplied payments, consumer confusion, and compliance risk.

This blog explains where AR automation commonly breaks down in the collections stage, why those failures hurt recovery, and the steps collection agencies can take to improve accuracy.

Accounts receivable automation for collection agencies refers to the use of software to automate payment processing, balance updates, reconciliation, and compliance workflows for delinquent accounts.

For collection agencies, AR automation typically includes:

For collection agencies, effective AR automation supports compliance. Structured workflows help ensure that payment activity and communications are documented consistently, reducing the likelihood of missing or conflicting records during audits or reviews.

At its core, accounts receivable automation helps collection agencies shift from reactive error correction to proactive accuracy. By reducing manual touchpoints and centralizing data, agencies gain cleaner records, more dependable reporting, and greater confidence in the information used to guide collection efforts.

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

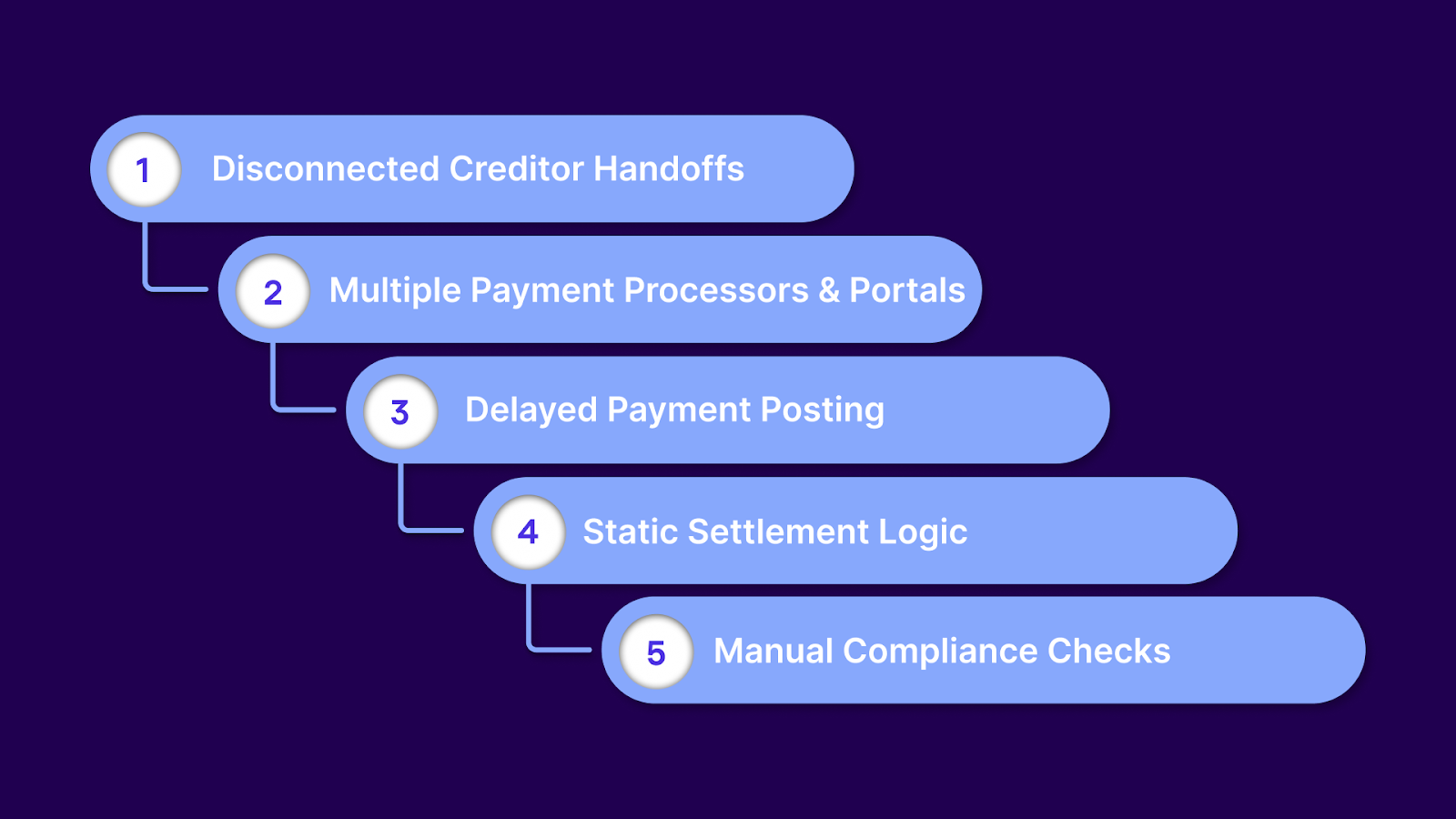

AR automation breaks down at specific points in the collection workflow. These breakdowns create errors that spread across your entire portfolio.

When creditors transfer accounts to your agency, the data rarely arrives in a clean, standardized format. You receive spreadsheets with different column headers, PDFs with incomplete payment histories, and manual updates sent through email.

Your automation system tries to import this data, but field mapping errors create immediate problems:

Your system might automate the wrong balance from day one, and every subsequent action compounds that initial error.

Most agencies accept payments through several channels: a proprietary payment portal, creditor portals, direct bank transfers, and third-party processors. Each system operates independently, with its own settlement schedule and reporting format.

The result is inconsistent visibility:

Automation cannot reconcile transactions it cannot see in real time. This creates a window in which balances appear incorrect, agents contact customers about obligations that have already been satisfied, and compliance violations occur because system activity does not reflect the actual payment status.

Even when payments reach your system, posting delays create accuracy problems. A customer pays on Monday, but your batch processing runs overnight, so the payment doesn't reflect until Tuesday.

During that gap:

Manual reconciliation catches some of these issues, but it defeats the purpose of automation. Your team spends hours comparing processor reports against internal records, hunting for missing transactions, and correcting posting errors that shouldn't exist in an automated system.

Your automation might calculate settlement offers based on the original balance without accounting for partial payments, disputed amounts, or applied credits.

Here's what happens:

Either way, the error damages recovery and creates additional work to resolve.

The Fair Debt Collection Practices Act and Regulation F require specific disclosures, timing restrictions, and documentation standards. Your automation handles outreach, but compliance verification often remains manual.

Agents review communications before sending, check account status before calling, and verify dispute flags before proceeding. This manual layer exists because your automated system lacks real-time AR automation accuracy.

You can't trust it to know whether:

These manual checks slow operations and introduce human error. The result of these accuracy breakdowns goes beyond operational inefficiency. They create real financial and legal consequences.

Tratta is designed to address these points of failure directly. By centralizing payment processing, balance updates, settlement logic, and compliance controls in a single platform, Tratta helps collection agencies maintain accuracy.

With a unified system of record, agencies gain clearer visibility into account activity, more reliable creditor reporting, and greater confidence that automation is operating on accurate data. Schedule a free demo to see how Tratta supports accurate AR automation throughout the collections lifecycle.

Suggested Read: How To Calculate Average Net Accounts Receivable: Definition, Formula & Examples

The next section outlines specific actions your agency can take to improve AR automation accuracy, regardless of your current platform.

Improving AR automation accuracy does not require a full platform replacement. The most effective gains come from correcting specific failure points where data becomes delayed, fragmented, or unreliable.

The following actions prioritize operational precision over system speed.

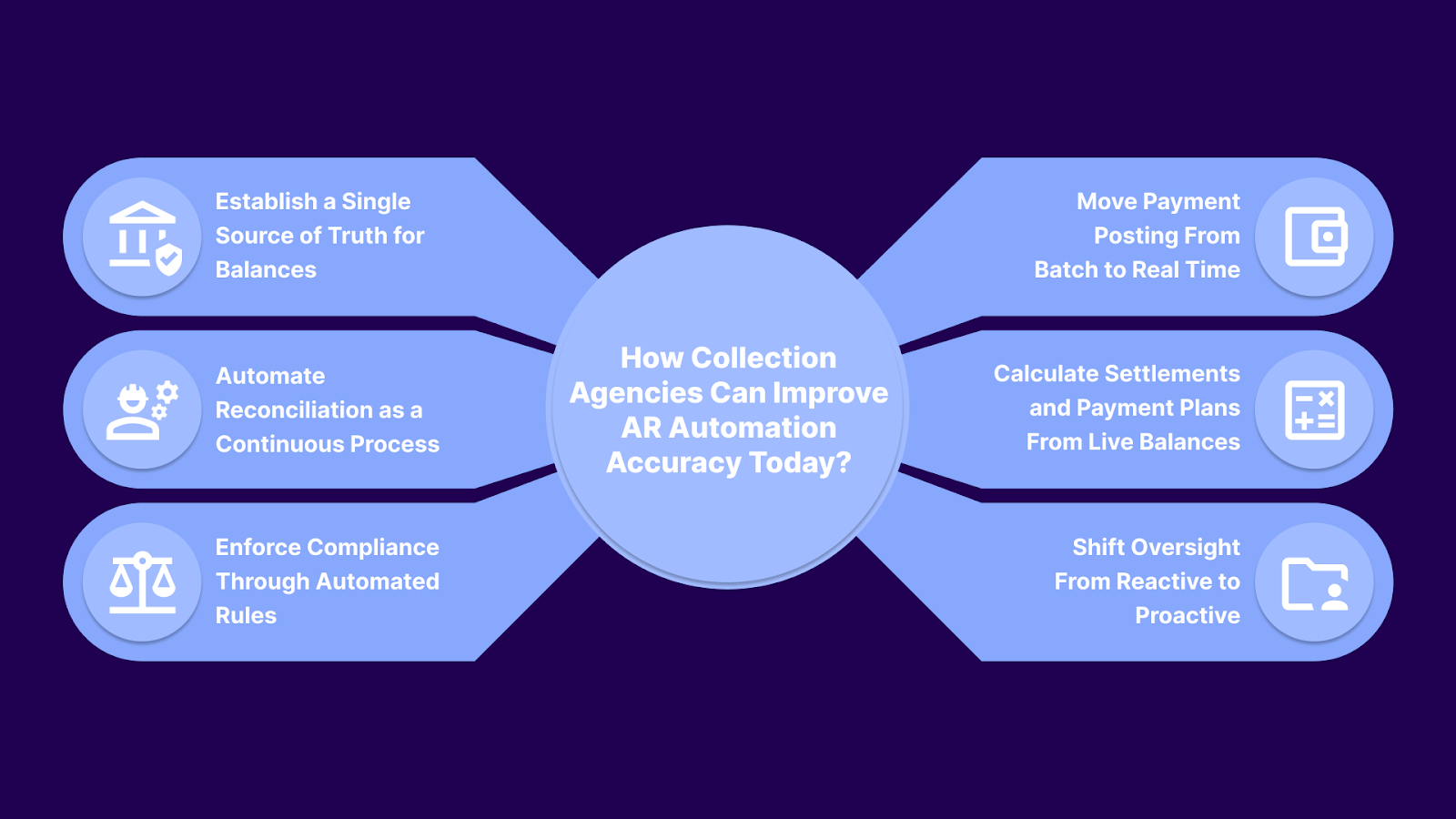

Accuracy breaks down when payment and balance data live in multiple systems. Collection agencies need one authoritative ledger per account, updated in real time, regardless of the payment channel.

Execution priorities:

Centralized, real-time data eliminates the timing gaps that create downstream errors in reporting, outreach, and compliance workflows.

Delayed posting introduces balance inaccuracies during the most sensitive moments in the collection lifecycle. Payments should update account balances immediately after authorization.

Operational requirements:

Immediate posting reduces duplicate outreach, improves agent effectiveness, and removes reconciliation work created solely to correct timing delays.

Reconciliation should occur automatically as transactions are received, not as a manual cleanup activity at the end of the day or week.

Automated reconciliation should handle:

Human intervention should be limited to valid exceptions. If staff regularly compare processor reports to internal ledgers, the automation is compensating for system gaps rather than enforcing accuracy.

To resolve this, Tratta streamlines reconciliation and collections by automating repetitive workflows, reducing manual errors, and freeing your team to focus on valid exceptions. Book a demo to see how it works for you.

Settlement offers must reflect the current account state at the moment they are generated. Static tables or pre-calculated amounts create avoidable disputes and revenue leakage.

Implementation standards:

Dynamic settlement logic prevents mismatches between consumer expectations and system calculations.

Compliance should be enforced by system logic, not manual review. Automation must prevent non-compliant actions by default.

Minimum compliance automation requirements:

Automated compliance controls reduce risk by eliminating reliance on human intervention at critical decision points.

Document existing compliance and accuracy checkpoints. Identify where manual reviews exist solely to compensate for unreliable system data. Replace those checkpoints with automated rules and exception-based monitoring.

The goal is not to remove oversight, but to ensure it operates upstream, before errors reach consumers, creditors, or regulators.

Targeted improvements reduce errors, accelerate recovery, and lower compliance exposure without disrupting existing operations.

Suggested Read: Understanding IVR Payment Systems: Enhancing Customer Experience & Streamlining Payments

Tratta is a debt collection and recovery platform built to help debt collection agencies improve AR automation accuracy by centralizing payments, account updates, communications, and reporting. By consolidating all activity into a single platform, agencies can reduce misposted payments, streamline reconciliation, and keep account status aligned with actual consumer activity.

Key features include:

With Tratta, you gain clarity, control, and confidence in your AR operations.

AR automation can transform collections, but only if accuracy is built in. When systems post payments instantly, reconcile data continuously, and enforce compliance automatically, agencies can operate with confidence, resolve accounts faster, and maintain strong creditor relationships.

Ultimately, automation is a tool, not a guarantee. Agencies that prioritize real-time data integrity and streamlined workflows will see measurable improvements in recovery, efficiency, and compliance resilience.

Tratta helps collection agencies turn automation into a dependable advantage. By centralizing account activity and eliminating manual gaps, your team can focus on what matters most: recovering debt efficiently, reducing errors, and maintaining trust with both consumers and creditors. Schedule a demo to see AR automation done right.

Staff should learn exception handling, verification processes, and reporting interpretation. Continuous training ensures employees correctly manage anomalies without undermining AR automation accuracy.

Consider real-time reconciliation capabilities, API integrations, compliance support, scalability, and audit trails. Vendor reliability, customer support, and US regulatory experience are key decision factors.

Yes, by standardizing data formats, integrating APIs, automating reconciliation, and applying exception-based monitoring. Incremental upgrades can enhance accuracy without full platform replacement.

Mobile wallets, real-time ACH, and tokenized card payments require integration and monitoring. Accurate recording and reconciliation depend on systems adapting to new transaction formats.

Rising misapplied payments, higher dispute rates, repeated balance corrections, delayed reconciliation, and inconsistent creditor reporting signal automation gaps that need immediate attention.