Debt collection does not always end with full repayment. In many cases, creditors and consumers reach a negotiated resolution that closes the account while recovering a portion of the balance. When that happens, having clear documentation is critical for protecting both sides and preventing future disputes.

Settlements are becoming increasingly common as consumer debt grows. In fact, U.S. household debt reached $18.80 trillion, according to the Federal Reserve Bank of New York. This highlights the scale of accounts that may eventually require structured repayment or settlement agreements.

A well-written agreement brings clarity to the process. In this guide, we explain how settlements work in collections and provide a sample settlement agreement between two parties that agencies can use to document payment terms and close accounts efficiently.

A settlement agreement in debt collections is a written arrangement between a creditor (or collection agency) and a debtor to resolve an outstanding balance under specific terms. For collection agencies, these agreements typically follow a settlement offer letter and help clarify the final payment terms and conditions.

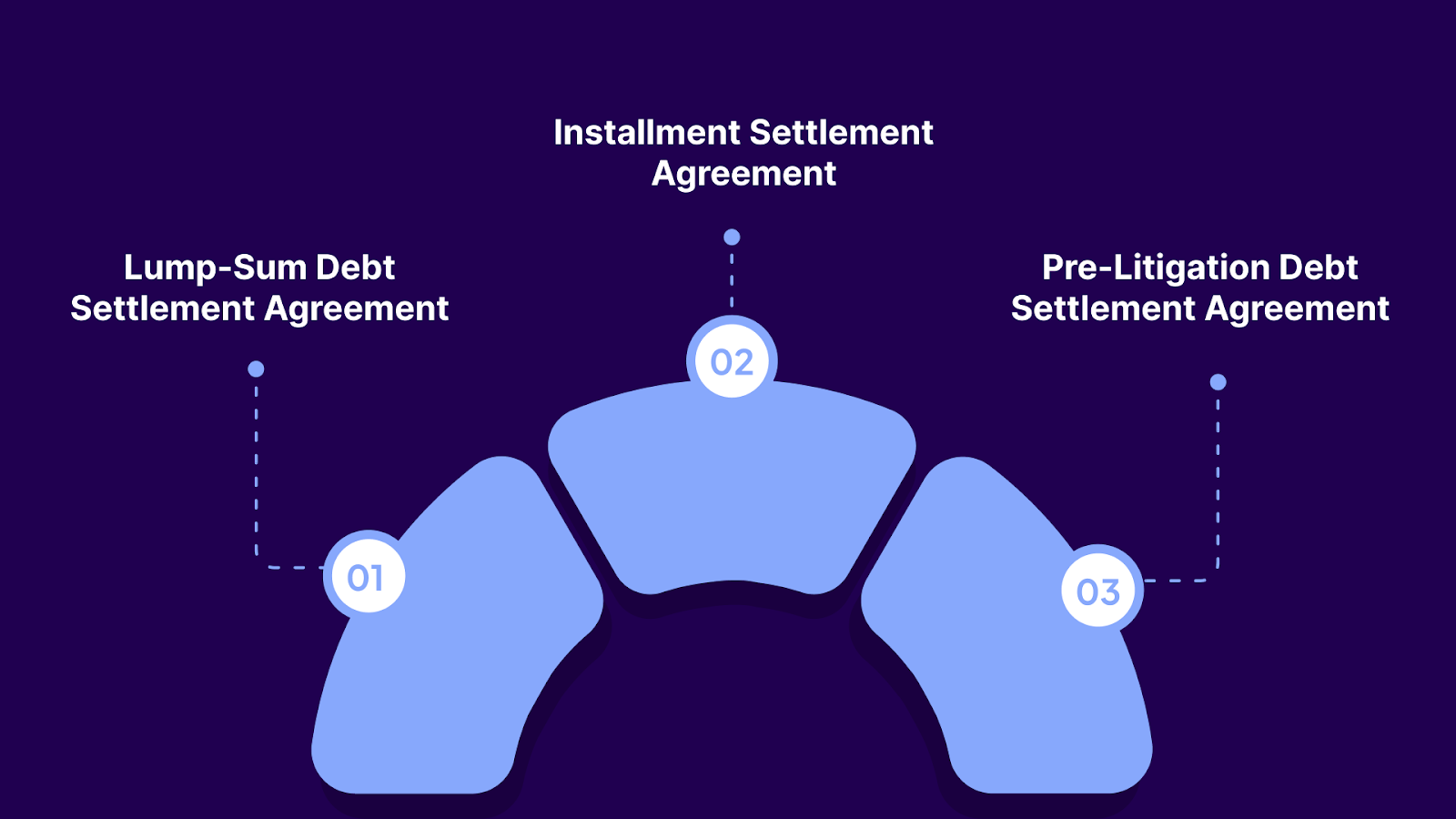

Agreements are useful in the following types of settlement accounts:

A settlement agreement only works if the terms are clear and complete. Both parties should be able to review the document and understand exactly what is being agreed to before any payment is made. This is explained in the next section.

Suggested Read: Understanding Settlement Accounts: Definition and How They Work

A settlement agreement should clearly outline the terms both parties are agreeing to, so there is no confusion later. Including the right details helps ensure the document is enforceable, transparent, and easy for both sides to follow.

These clauses are necessary in every debt settlement agreement between two parties:

Managing these components consistently across multiple accounts can be challenging. Tratta helps collection agencies manage settlement communications, payment arrangements, and account activity in one platform. This makes it easier to track agreements and keep resolutions moving forward. Book a free demo.

The examples below are structured according to commonly accepted practices in U.S. debt collections. They are written with consideration for major applicable regulations, such as the FDCPA, Regulation F, and the FCRA. They are intended to illustrate how agencies typically document settlement terms while maintaining clear communication and compliance awareness.

The example shows how a lump-sum settlement is typically documented in collections. This format clearly outlines the account details, negotiated amount, payment deadline, and the conditions required to consider the debt resolved.

Settlement Agreement

This Settlement Agreement (“Agreement”) is made on [Date] between:

Collection Agency / Authorized Representative of Creditor

[Agency Name]

[Address]

[License Number if applicable]

and

Consumer

[Full Name]

[Address]

1. Account Information

Original Creditor: [Creditor Name]

Account Number: [XXXXXX]

Current Balance: $[Amount]

The collection agency represents that it is authorized to resolve this account on behalf of the creditor or current account owner.

2. Settlement Offer

The agency agrees to accept $[Settlement Amount] as a negotiated settlement of the account referenced above.

If the payment is received in accordance with the terms below, the account will be considered settled for less than the full balance.

3. Payment Terms

Payment must be received by [Date].

Accepted payment methods may include:

If payment is not received by the agreed date, this settlement offer may be withdrawn, and normal collection activity may resume where permitted by law.

4. Consumer Rights and Federal Compliance

Nothing in this Agreement is intended to waive or limit any rights provided to the consumer under applicable law, including the Fair Debt Collection Practices Act (FDCPA) and Regulation F.

Consumers retain the right to dispute the debt as permitted by law. This agreement applies only if the consumer voluntarily accepts the settlement terms.

5. Credit Reporting

Information about this account may be reported to consumer reporting agencies in accordance with the Fair Credit Reporting Act (FCRA) and applicable regulations.

Upon successful completion of the settlement payment, the account may be reported as settled or a similar status consistent with industry reporting standards.

6. Tax Implications

If a portion of the debt is forgiven, the creditor may be required to report the forgiven amount to the Internal Revenue Service as required by law. The consumer may receive a Form 1099-C where applicable.

Consumers should consult a tax professional regarding potential tax consequences.

7. No Admission of Liability

This Agreement represents a negotiated compromise of the account. It does not constitute an admission of liability by any party.

8. Governing Laws

This Agreement is intended to comply with applicable laws governing debt collection and consumer protection, including but not limited to:

Additional disclosures may apply depending on the consumer’s state of residence.

9. Entire Agreement

This document represents the entire settlement agreement between the parties. Any changes must be made in writing and agreed to by both parties.

10. Acceptance

Authorized Representative

Name:

Title:

Signature: __________________

Date: ___________

Consumer

Name:

Signature: __________________

Date: ___________

Further Insight: How Do Settlements Work in Self-Service Debt Payments?

Some consumers may not be able to make a single lump-sum payment but are still willing to resolve the debt. In these cases, an installment settlement agreement allows both parties to structure manageable payments while working toward closing the account.

Settlement Agreement

This Settlement Agreement (“Agreement”) is made on [Date] between:

Collection Agency / Authorized Representative of Creditor

[Agency Name]

[Address]

[License Number if applicable]

and

Consumer

[Full Name]

[Address]

1. Account Information

Original Creditor: [Creditor Name]

Account Number: [XXXXXX]

Current Balance: $[Amount]

The collection agency represents that it is authorized to resolve this account on behalf of the creditor or current account owner.

2. Settlement Offer

The agency agrees to resolve the account for a total settlement amount of $[Settlement Amount], to be paid through an agreed installment arrangement.

If the payments described below are completed successfully, the account will be considered settled for less than the full balance.

3. Payment Schedule

The consumer agrees to make the following payments:

Payments must be made through approved payment channels provided by the agency.

4. Missed Payment Terms

If a scheduled payment is missed or returned, the settlement arrangement may become void where permitted by law. The account may revert to its previous balance, less any payments received, and collection activity may resume, subject to applicable regulations.

5. Consumer Rights and Federal Compliance

Nothing in this Agreement is intended to waive or limit any rights provided under applicable law, including the Fair Debt Collection Practices Act (FDCPA) and Regulation F.

Consumers retain the right to dispute the debt as permitted by law prior to accepting the settlement.

6. Credit Reporting

Information related to this account may be reported to consumer reporting agencies in accordance with the Fair Credit Reporting Act (FCRA).

Once the settlement payments are completed, the account may be reported as settled or a similar status consistent with credit reporting guidelines.

7. Tax Implications

If any portion of the debt is forgiven, the creditor may be required to report the forgiven amount to the Internal Revenue Service. The consumer may receive a Form 1099-C where required by law.

Consumers should consult a qualified tax advisor regarding potential tax consequences.

8. No Admission of Liability

This Agreement represents a negotiated resolution and does not constitute an admission of liability by either party.

9. Governing Laws

This Agreement is intended to comply with applicable laws governing debt collection, including:

Additional disclosures may apply depending on jurisdiction.

10. Entire Agreement

This document represents the complete agreement between the parties regarding the settlement of the account. Any modifications must be made in writing and agreed to by both parties.

11. Acceptance

Authorized Representative

Name:

Title:

Signature: __________________

Date: ___________

Consumer

Name:

Signature: __________________

Date: ___________

Further Insight: 5 Debt Settlement Letter Templates for Faster Negotiations

Complex accounts sometimes require a negotiated resolution before legal action progresses further. In these situations, settlement agreements help both parties close the matter without additional time, expense, or uncertainty.

Settlement Agreement

This Settlement Agreement (“Agreement”) is entered into on [Date] between:

Collection Agency / Authorized Representative of Creditor

[Agency Name]

[Address]

[License Number if applicable]

and

Consumer

[Full Name]

[Address]

1. Account Information

Original Creditor: [Creditor Name]

Account Number: [XXXXXX]

Current Balance: $[Amount]

The collection agency represents that it is authorized to resolve this account on behalf of the creditor or current account owner.

2. Settlement Terms

To resolve the account prior to further legal proceedings, the agency agrees to accept $[Settlement Amount] as a negotiated settlement.

If the payment terms outlined below are completed, the account will be considered settled according to the agreed terms.

3. Payment Conditions

The consumer agrees to one of the following payment arrangements:

Payments must be made through approved payment channels provided by the agency.

4. Suspension of Legal Action

Upon acceptance of this Agreement and while payments remain current, the agency may pause further legal escalation related to the account where permitted by law.

If the settlement terms are not completed, collection activity or legal action may resume consistent with applicable regulations.

5. Consumer Rights and Compliance Notice

Nothing in this Agreement limits or waives any rights provided under applicable law, including the Fair Debt Collection Practices Act (FDCPA) and Regulation F.

Consumers retain the right to dispute the debt as allowed by law prior to accepting this settlement.

6. Credit Reporting

Information regarding this account may be reported to consumer reporting agencies in accordance with the Fair Credit Reporting Act (FCRA).

After successful completion of the settlement terms, the account may be reported as settled or a similar status consistent with reporting standards.

7. Possible Tax Consequences

If a portion of the debt is forgiven, the creditor may be required to report the forgiven amount to the Internal Revenue Service. The consumer may receive a Form 1099-C where applicable.

Consumers may wish to consult a tax professional regarding potential tax implications.

8. No Admission of Liability

This Agreement reflects a negotiated compromise intended to resolve the account. It does not represent an admission of liability by either party.

9. Governing Laws

This Agreement is intended to comply with applicable laws governing debt collection and consumer protection, including:

Additional requirements may apply depending on jurisdiction.

10. Entire Agreement

This document represents the complete settlement agreement between the parties. Any modifications must be made in writing and agreed to by both parties.

11. Acceptance

Authorized Representative

Name:

Title:

Signature: __________________

Date: ___________

Consumer

Name:

Signature: __________________

Date: ___________

Important Notice: These sample settlement agreements are provided for informational purposes only. Collection agencies should have settlement communications reviewed by legal counsel to ensure compliance with federal, state, and local laws.

Now that you have seen how settlement agreements are typically structured, the next step is understanding how to draft a debt settlement offer letter. This letter presents the proposed terms to the consumer before any formal agreement is created.

Suggested Read: Automated Debt Settlement: What It Is And How It Works

A debt settlement offer letter formally presents the terms a creditor or collection agency is willing to accept to resolve an account. It outlines the proposed settlement amount, payment terms, and conditions so the consumer can review and decide whether to accept. If accepted, the terms are typically documented later in a formal settlement agreement.

Key steps to writing a settlement letter:

Managing settlement letters manually can quickly become difficult as account volumes increase. Teams need a reliable way to maintain agreement consistency, track responses, and ensure offers are documented correctly.

Tratta helps collection agencies coordinate settlement activity alongside communication and payments in one system. Instead of juggling spreadsheets and disconnected tools, teams can monitor account progress and keep negotiations organized. Learn more.

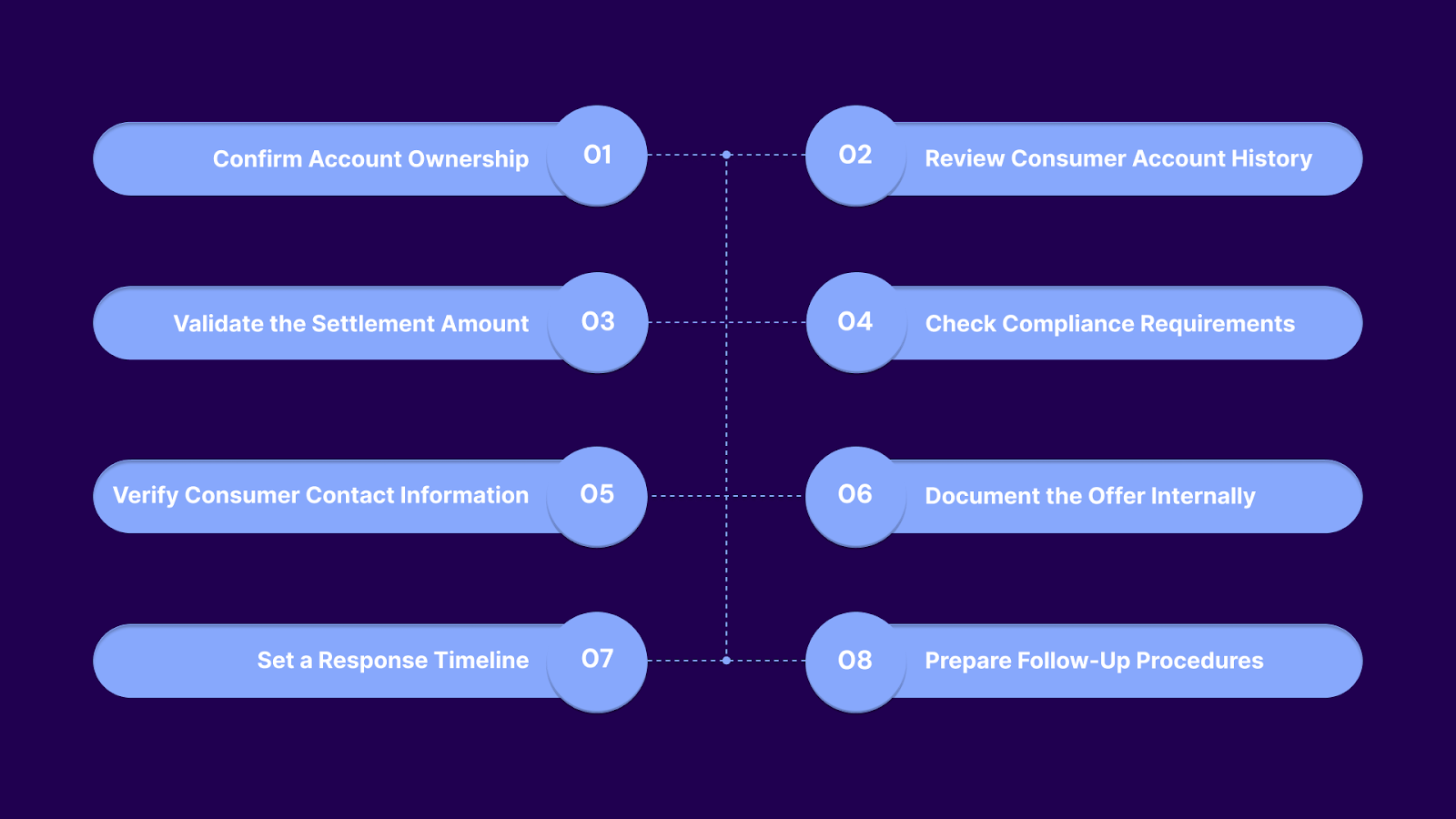

A checklist helps ensure account details are verified, regulatory requirements are considered, and the proposed terms are practical for both parties.

Follow this structured review process before any settlement agreement:

Agencies also need reliable systems to track agreements, payments, and communication as accounts progress. That is where technology begins to play an important role.

Managing settlement agreements across hundreds or thousands of accounts can quickly become complex. Collection teams must track offers, document consumer responses, monitor payments, and ensure communications remain consistent and compliant.

The right software can help agencies in the following ways:

Tratta brings these features together in a collections-focused platform. Agencies can coordinate communication, payment activity, and account progress without relying on disconnected systems. By keeping settlement activity visible and organized, Tratta helps teams manage agreements more efficiently while maintaining control over their portfolios.

When settlement agreements are unclear or poorly documented, collection agencies face unnecessary complications. Misunderstood payment terms, missed deadlines, and inconsistent communication can lead to disputes, compliance risks, and unresolved accounts that linger longer than necessary.

Tratta helps agencies manage settlement activity with better organization and visibility. By keeping communication, payment activity, and account updates connected in one platform, teams can move negotiations forward while maintaining clear records of every agreement.

This is how Tratta accelerates the debt settlement process:

If your team regularly manages settlement agreements, having the right systems in place can make a significant difference. Schedule a call today to optimize settlement workflows and improve recovery outcomes.

Collection agencies document the account details, settlement amount, payment terms, deadlines, and compliance language in writing. The agreement should clearly state when the debt will be considered resolved after payment.

The 7-7-7 rule generally refers to a structured outreach rhythm where collectors follow up with consumers at planned intervals. Agencies use similar communication strategies to maintain engagement and improve recovery chances.

Yes. Collection agencies frequently draft settlement agreements when negotiating resolutions with consumers. The document should clearly outline the terms and follow applicable debt collection and consumer protection regulations.

Sometimes. Acceptance depends on factors such as account age, balance size, recovery probability, and creditor policies. Older accounts or hardship situations may increase the likelihood of a reduced settlement.

Agreements should include account identification, settlement amount, payment schedule, acceptance terms, compliance language, and signatures. Clear documentation helps prevent disputes and ensures both parties understand the resolution.