Your portfolio just doubled. Your recovery rates dropped 15%. This scenario plays out across collection agencies every quarter. The debt collection software market is growing and is projected to reach $11.96 billion by 2033, yet many agencies still struggle when volumes increase.

The problem is not growth. It is what growth exposes. Processes that work at lower volumes begin to fail as accounts, channels, and compliance requirements multiply. Without scalable collection solutions, more placements often mean higher costs, slower recovery, and greater regulatory risk.

More accounts should mean more revenue, not more strain, which is why this article breaks down how scalable collection solutions help agencies manage high volumes efficiently, protect margins, and maintain compliance.

Scalable collection solutions handle increasing account volumes without requiring equal increases in staff, infrastructure, or operational costs. These platforms use automation, self-service tools, and centralized workflows to maintain recovery performance as portfolios expand.

Traditional systems built on manual processes quickly reach capacity limits. Scalable solutions remove those limits by making processes repeatable, consistent, and independent of headcount.

Core characteristics include:

When these elements work together, you can add 10,000 accounts without adding 10 agents. Recovery speed improves because follow-ups happen on schedule, not when staff capacity allows.

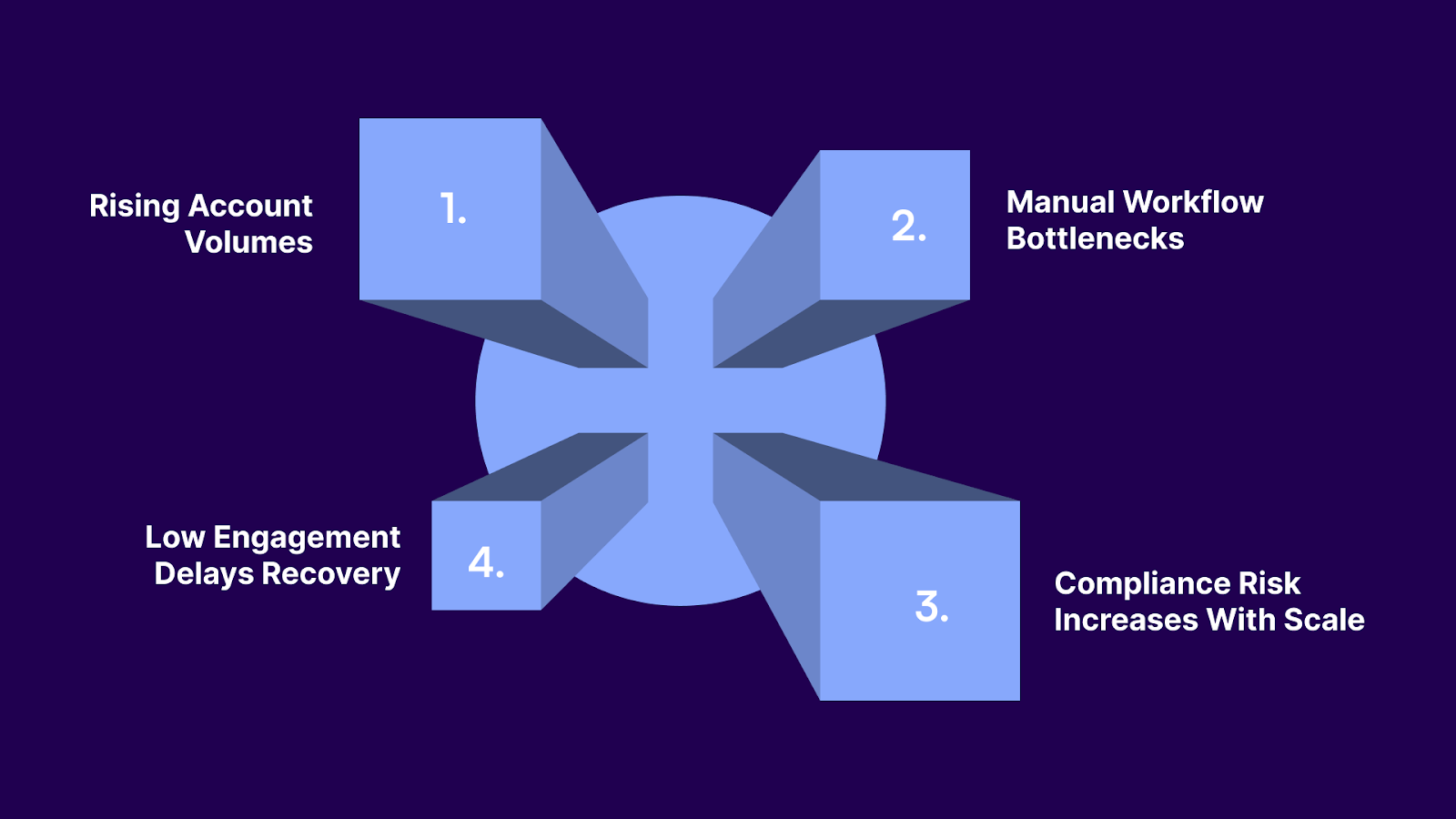

Scaling collections is all about maintaining control, consistency, and compliance as volume increases. Processes that work at lower volumes often fail under scale, directly impacting recovery rates, operating margins, and regulatory risk.

The challenges below are the most common barriers to sustainable growth.

As agencies take on new clients or larger portfolios, manual processes struggle to keep pace. Task lists expand, follow-ups are missed, and accounts age without timely engagement.

This breakdown shows up quickly in performance metrics:

Portfolio diversity compounds the issue. Different clients require different settlement rules, payment plans, and disclosure language. Managing these variations manually increases errors and creates operational and compliance gaps.

Manual workflows introduce friction at every stage of the collection process. Agents spend significant time on repetitive administrative tasks rather than on high-value account resolution.

Common bottlenecks include:

As volume grows, these inefficiencies multiply, wasting resources and degrading both agent productivity and consumer experience.

Regulatory compliance becomes harder to manage as collections expand across accounts, channels, and time zones. Requirements under the FDCPA and Regulation F must be applied consistently, accurately, and on time.

Key obligations include:

At scale, manual enforcement becomes unreliable. Missed notices, mistimed calls, or delayed suppression flags create violations that expose agencies to complaints, litigation, and regulatory scrutiny.

Traditional, agent-led collection models limit consumer participation. Calls go unanswered, letters are ignored, and engagement depends on consumers being available during business hours.

This creates avoidable delays:

When consumers face friction or limited options, resolution slows, and recovery rates suffer.

Tratta addresses these challenges with a consumer self-service portal that operates 24/7. Debtors can view balances, set up payment plans, and make payments without agent involvement. This reduces friction, increases engagement, and accelerates resolution. Book a demo to explore how it solves your problems.

Suggested Read: Debt Recovery Case Management Software for Smarter Workflows

Not all collection platforms scale the same way. Some simply digitize manual processes without removing bottlenecks. The platforms that actually scale share specific capabilities.

Effective automation handles repetitive tasks without human intervention:

This frees agents to focus on complex negotiations and high-value accounts. Instead of spending hours sending emails, they handle only the cases that require judgment.

Automation only works if it maintains quality. Templates should be customizable by portfolio or client. Triggers should be configurable to match your collection strategy.

Scalable platforms embed regulatory requirements directly into workflows, making violations impossible rather than merely unlikely.

Built-in compliance includes:

Under Regulation F, debt collectors must provide specific validation information, including the debt amount, the creditor's name, and the consumer's rights. The system should generate these disclosures automatically and maintain proof of delivery.

Audit trails are critical. When regulators request documentation, you need complete records of every communication, payment, and status change.

Debtors have communication preferences. Some respond to email, others to SMS, others only to phone calls. Scalable solutions support all channels from one system, so outreach is coordinated rather than fragmented.

Channels to support:

Omnichannel platforms track engagement across all touchpoints. If a debtor clicks a payment link in an email but does not complete the transaction, the system flags the account for follow-up.

Self-service reduces dependency on agent availability. Debtors can check balances, review payment history, set up plans, and make payments anytime from any device.

A debtor ready to pay at midnight does not wait for your office to open. They log in, confirm their balance, and submit payment immediately. Your recovery happens faster without any agent involvement.

Digital payment options should include:

Security is required. Look for platforms that are PCI DSS Level 1 compliant and SOC 2 Type II certified. Payment data should be encrypted and tokenized.

You cannot improve what you cannot measure. Scalable platforms provide real-time reporting on recovery performance, agent productivity, and portfolio health.

Dashboards should display:

Drill-down capabilities let you investigate anomalies. If one portfolio has a lower recovery than others, you can identify whether the issue is account quality, agent performance, or strategy misalignment.

Suggested Read: Email Marketing Strategies for Debt Recovery Business

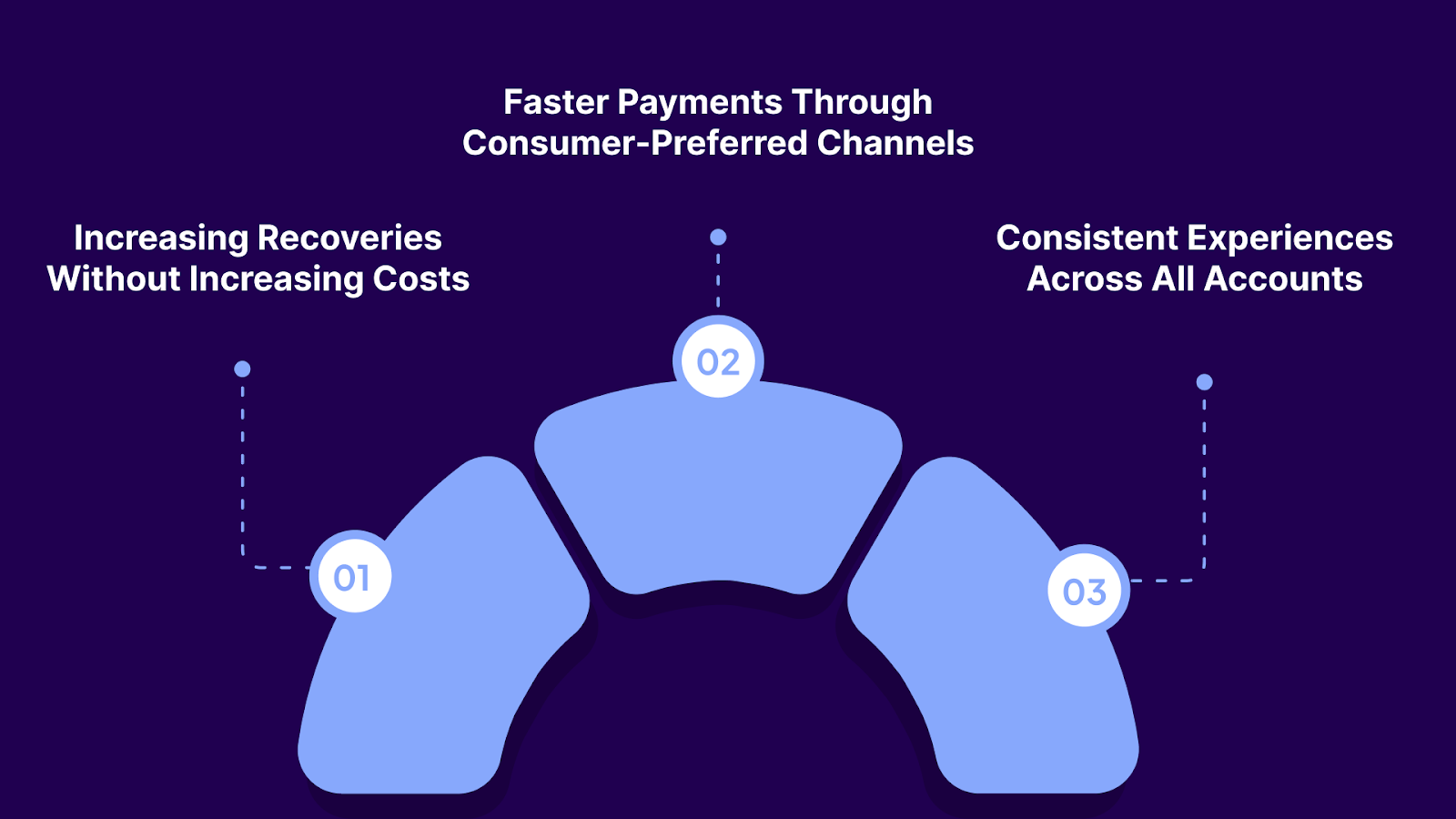

Scalability is not just about handling volume. It is about maintaining or improving performance as volume increases. The right platform changes the economics of collections.

Manual processes force a linear relationship between accounts and headcount. Add 10,000 accounts, hire 5 agents. Double your portfolio, double your payroll.

Scalable solutions break this pattern:

An agency that previously managed 50,000 accounts with 20 agents can now manage 100,000 accounts with 25 agents. Cost per account drops. Profit margins expand.

Debtors who can pay on their terms pay faster. Self-service portals eliminate scheduling friction. Payment plans are available immediately, rather than after agent negotiation.

Agencies that offer digital options match consumer behavior. Those who do not create unnecessary obstacles. The gap between intent and action shrinks when payment is immediate. A debtor who clicks a link and completes payment in 30 seconds becomes a resolved account.

Scalable platforms standardize execution. Every account receives the same quality of service regardless of when it entered the system or which agent is assigned.

Consistency improves outcomes:

For your team, standardization reduces training time and improves quality. New agents follow established workflows instead of inventing their own.

Suggested Read: Honest Debt Recovery Solutions: What to Look For

Not all collection software is built for scale. Here are the key differences between platform types.

As volume grows, systems that rely on manual effort or disconnected tools struggle to maintain performance and compliance. Platforms built with unified architecture are better equipped to handle higher account volumes without increasing operational cost or risk.

Tratta operates as a unified, cloud-native platform. Payments, outreach, compliance, and analytics work from a single source of truth. Your team manages all collection activities through a single interface. Schedule a demo to see how Tratta eliminated operational silos.

Suggested Read: Collecting Payments: 7 Quick Tips for Debt Recovery Teams

Selection mistakes are expensive. The wrong platform creates technical debt, compliance gaps, and operational friction. Here is what to evaluate.

Ask specific questions about performance at scale:

Request references from agencies managing portfolios similar to your target size. If you plan to reach 100,000 accounts, speak with agencies already operating at that level.

Compliance failures destroy agencies. Your platform should make compliance violations difficult, if not impossible.

Review how the system handles:

Ask about update frequency. How quickly does the vendor implement new regulatory requirements?

Your debtors interact with the platform more than your agents do. A poor consumer experience creates a support burden and reduces recovery rates.

Test the self-service portal yourself:

Your platform should provide complete visibility into performance without manual report building.

Evaluate dashboard capabilities:

Reports should reflect account status as of the current moment, not as of last night's batch process.

Your collection strategy will change. Client requirements vary. Regulatory rules evolve. Your platform must adapt without requiring vendor involvement for every adjustment.

Look for configuration options including:

Ask about configuration limits. Some platforms advertise flexibility but impose strict boundaries on customization.

Suggested Read: Understanding Debt Recovery Resources And Collection Agencies

Tratta is a digital-first platform built to support high-volume collection operations without adding operational or compliance risk. Instead of relying on manual processes or disconnected tools, Tratta helps you standardize workflows, shift resolution to self-service, and maintain consistent compliance as volume grows.

The following capabilities show how Tratta directly addresses the operational, compliance, and engagement challenges that limit scalability.

Tratta gives consumers secure, 24/7 access to resolve balances on their terms, reducing agent workload and accelerating payment.

Consumers can:

Available payment options:

All payment data is encrypted and tokenized. The platform maintains PCI DSS Level 1 and SOC 2 Type II certifications to protect sensitive information.

Tratta Campaigns allow you to automate outreach across digital channels while maintaining full compliance.

You can:

Required FDCPA disclosures are applied automatically. Timing restrictions are enforced at the system level, and cease-communication requests immediately stop all outreach.

Tratta extends digital self-service to voice channels through a multilingual IVR.

Consumers can:

All IVR activity syncs with the consumer portal in real time, ensuring agents and clients always see the most up-to-date account status.

Tratta integrates with your existing systems without requiring a full technology overhaul.

Integration options include:

This flexibility allows you to maintain your current CRM or core collection system while adding Tratta’s consumer engagement and payment capabilities. Typical implementation is completed within 30 days, including configuration and training.

Tratta provides real-time visibility into performance across portfolios and workflows.

Dashboards track:

All metrics update in real time as accounts move through campaigns and payment flows.

Organizations use Tratta to scale collections while maintaining performance and compliance. Companies like Multi-Service Fuel Card have doubled card payment volume and recovered hundreds of thousands in previously uncollected balances by shifting resolution to consumer self-service.

Large agencies such as FMA Alliance have handled multi-fold increases in transaction volume while maintaining exceptional customer satisfaction and reducing call dependency through automated outreach and reporting.

Growth will keep coming. The real question is whether your collections operation is built to handle it. Scalable collection solutions enable agencies to absorb higher volumes without losing control over recovery performance, costs, or compliance.

Tratta supports this shift by helping agencies move away from manual dependency and toward consistent, digital-first execution. When payments, outreach, compliance, and reporting work from a single system, scaling stops being a risk and starts becoming an advantage.

If your portfolio is growing faster than your results, it may be time to rethink how collections operate. See how Tratta helps agencies scale collections without adding cost or complexity. Schedule a demo today.

Implementation timelines vary, but modern cloud-based platforms usually deploy within weeks, depending on integrations, data migration complexity, and internal process readiness.

Yes. Scalable platforms support portfolio-level rules, client-specific disclosures, and configurable workflows to manage varying settlement terms, regulations, and reporting needs.

Automation reduces low-value tasks, not expertise. Experienced agents focus on complex negotiations, disputes, and high-balance accounts where human judgment delivers better outcomes.

Reliable platforms use encryption, tokenization, role-based access controls, and industry certifications like PCI DSS and SOC 2 to protect consumer and payment data.

ROI is measured through reduced cost per account, improved recovery rates, faster time to payment, lower agent workload, and fewer compliance-related incidents.