Staying compliant in debt collection is getting harder. Rules change, oversight is tightening, and even a small misstep can lead to complaints, penalties, or lost accounts. If you are managing high volumes, keeping every interaction compliant can be difficult.

In fact, the Consumer Financial Protection Bureau reported 207,800 debt collection complaints in a single year, highlighting how quickly compliance failures can escalate into regulatory and legal risk.

For agencies operating in Minnesota, the stakes are even higher due to additional state-level requirements. In this article, we break down the key Minnesota debt collection laws you need to understand in 2026 and what they mean for your compliance and recovery strategy.

Compliance failures in debt collection do not stay small. They turn into financial penalties, lawsuits, and operational disruption that directly impact your bottom line. With both federal and Minnesota-specific laws in play, a single violation can trigger multiple layers of liability.

If you are handling high account volumes, the risk compounds quickly. One non-compliant script, one mistimed call, or one missing disclosure can expose your agency across hundreds or thousands of accounts.

Non-compliance can lead to the following consequences:

The financial impact is only part of the problem. Legal disputes slow down collections, damage client trust, and reduce recovery rates. That is why understanding the specific laws governing Minnesota debt collection is necessary.

Suggested Read: Debt Collection Rights and Regulations: Understanding the Law

Collection agencies need to navigate a layered legal framework that combines federal law with multiple state statutes governing licensing, conduct, disclosures, and consumer protection. Missing even one requirement can expose an organization to enforcement actions and private litigation.

Understanding the following laws can help you operate compliantly and protect recovery performance:

The Minnesota Collection Agencies Act governs who can legally operate as a collection agency in the state. It requires agencies to obtain proper licensing, maintain financial responsibility, and follow strict operational standards. The law also outlines prohibited practices and gives regulators authority to enforce compliance.

Key requirements and implications include:

Minnesota does not have a standalone statute named exactly like the federal FDCPA, but it enforces similar standards through state provisions and incorporates federal protections. Agencies must comply with the Fair Debt Collection Practices Act alongside Minnesota statutes governing unfair practices. These combined rules regulate how, when, and how often you communicate with consumers.

Core compliance expectations include:

Tratta helps agencies operationalize these requirements through automated communication controls, validation workflows, and audit-ready tracking, reducing the risk of human error. Its system ensures that every interaction aligns with regulatory expectations while maintaining consistent engagement across accounts. Schedule a free demo.

The Minnesota Consumer Fraud Act broadly prohibits deceptive, misleading, or fraudulent practices in consumer transactions, including debt collection. Its scope is broader than traditional collection laws, meaning agencies can be held accountable even for indirect or ambiguous misrepresentations. Enforcement can come from both the Attorney General and private lawsuits.

This law introduces additional compliance pressure through:

The Minnesota Deceptive Trade Practices Act focuses on preventing deceptive business practices, including false representations and misleading conduct. Unlike some statutes, it allows courts to issue injunctions even without proof of intent, making it easier to enforce. This creates additional compliance exposure for collection agencies.

Key considerations under this law include:

Minnesota law sets time limits on how long a debt can be legally enforced. Under the Minnesota Statute of Limitations, most contract-based debts have a six-year limitation period, though specifics can vary based on the debt type. Attempting to collect or litigate time-barred debt without proper handling can create serious legal risk.

This directly affects the collection strategy in the following ways:

Recent reforms are changing how these rules apply in day-to-day operations. These updates, particularly around medical debt, introduce new compliance expectations that agencies cannot afford to overlook.

Suggested Read: Text of Fair Debt Collection Practices Act in Federal Code

Recent reforms, especially those related to medical debt, introduce new compliance obligations that directly affect reporting, communication, and recovery strategies. These changes are not cosmetic. They alter how agencies segment accounts, apply pressure, and manage consumer interactions.

Reforms include:

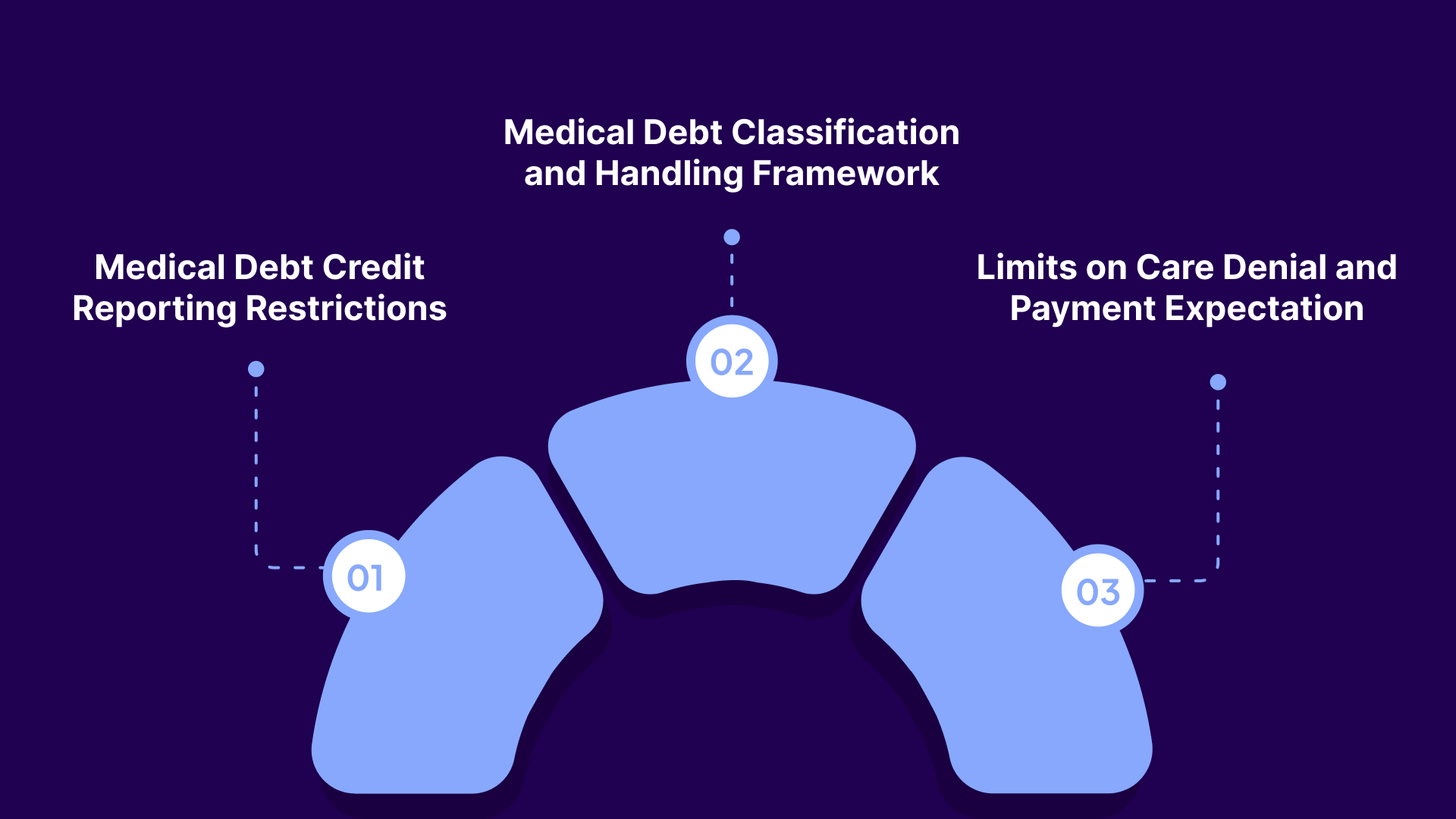

Minnesota now restricts how medical debt is reported to credit agencies, significantly reducing a long-standing collection lever. This change directly impacts recovery strategies that rely on credit visibility to drive repayment. Agencies must now rethink how they approach medical accounts without relying on reporting pressure.

Key compliance considerations include:

Minnesota has created a dedicated legal framework that defines and regulates medical debt. This formal classification introduces clear boundaries on how these accounts are treated throughout the collection lifecycle. Agencies must align their workflows with these definitions to avoid compliance gaps.

This framework requires agencies to:

Minnesota law (under § 62J.807) now limits how unpaid medical debt affects a consumer’s access to care. Providers cannot deny medically necessary treatment due to outstanding balances, which indirectly affects the urgency of collection and repayment behavior. This reduces the immediate pressure on consumers to resolve medical debt.

Operational implications include:

Minnesota is treating certain debt categories with heightened consumer protection and stricter oversight, requiring agencies to move beyond one-size-fits-all strategies. The next section highlights how you need to design and execute your collection strategy.

Suggested Read: Minnesota's Debt Fairness Act: Key Changes and Provisions

Minnesota’s legal environment shifts debt collection from a volume-driven model to a control-driven, risk-aware operation. Agencies can no longer rely on uniform approaches across portfolios. Instead, laws now dictate how different account types behave, how quickly they resolve, and how much pressure can be applied.

These are a few ways debt collection laws are forcing change:

Tratta supports this shift by aligning strategy with compliance at a structural level. It allows agencies to manage different account types, enforce communication boundaries, and maintain visibility across workflows without relying on manual adjustments. Call us to learn more.

As Minnesota regulations introduce tighter controls, compliance becomes a systems-and-process design challenge, not just a policy issue. Agencies need operational precision across communication, data handling, and workflow execution to stay compliant without slowing down recoveries.

These are a few tips to ensure your team remains compliant:

At this level, compliance depends on how well your systems enforce these controls at scale. This is exactly what we explore in the next section with Tratta.

Suggested Read: Debt Collection Compliance Checklist: An Essential Guide for Debt Collectors

.jpg)

Tratta is a digital-first debt collection platform that unifies payments, communication, workflows, and compliance into a single system. It is built to help agencies enforce regulatory requirements at scale while maintaining efficiency and recovery performance.

Designed for modern compliance environments, Tratta enables agencies to align operations with laws such as the FDCPA and evolving Minnesota regulations through automation and centralized control.

In addition to compliance-specific capabilities, here are Tratta’s core platform features:

Tratta brings compliance and performance into a single operational layer. It reduces reliance on manual oversight by embedding rules directly into workflows. As regulations continue to improve, this approach helps agencies stay compliant without sacrificing recovery efficiency.

Failing to align with Minnesota debt collection laws can quickly lead to penalties, lawsuits, and operational breakdowns. What starts as a small compliance gap can escalate into regulatory action, financial loss, and damaged client trust. Over time, inconsistent processes and outdated strategies reduce recovery rates and make scaling nearly impossible.

Tratta helps you avoid these risks by embedding compliance directly into your operations. With automated workflows, communication controls, and centralized visibility, it ensures every interaction aligns with both federal and Minnesota-specific requirements. This allows you to maintain performance without exposing your agency to unnecessary legal risk.

Stay compliant without slowing down your collections. See how Tratta can help you simplify operations and reduce risk. Schedule a free call.

In Minnesota, most debts are subject to a six-year statute of limitations (Minn. Stat. § 541.05). After this period, the debt becomes time-barred, meaning agencies cannot pursue legal action to enforce collection, though limited collection activity may still be allowed if compliant.

The commonly cited phrase is a consumer's request to stop communication, but legally it relates to rights under the Fair Debt Collection Practices Act. Once a written cease-and-desist request is received, agencies must stop most communication, except for specific permitted notices.

Minnesota collection is governed by a combination of federal and state laws, including the Fair Debt Collection Practices Act, the Minnesota Collection Agencies Act, and consumer protection laws such as the Minnesota Consumer Fraud Act. Recent reforms also regulate medical debt under Minn. Stat. Ch. 332C.

Consumers are obligated to repay valid debts, but collectors must prove the debt and follow all legal requirements. If a debt is disputed, validated, or time-barred, enforcement options may be limited, and agencies must proceed carefully to remain compliant.

Yes, but with restrictions. While agencies may attempt to collect time-barred debt, they cannot threaten or initiate legal action, and any communication must not mislead consumers about enforceability under Minn. Stat. § 541.05 and FDCPA rules.