Debt collection errors often surface where timing and legal boundaries intersect. According to the CFPB’s 2025 FDCPA Annual Report, complaints related to “taking or threatening to take a negative or legal action” ranked fourth among all debt collection issues in 2024, accounting for 7% of the 207,800 complaints received that year.

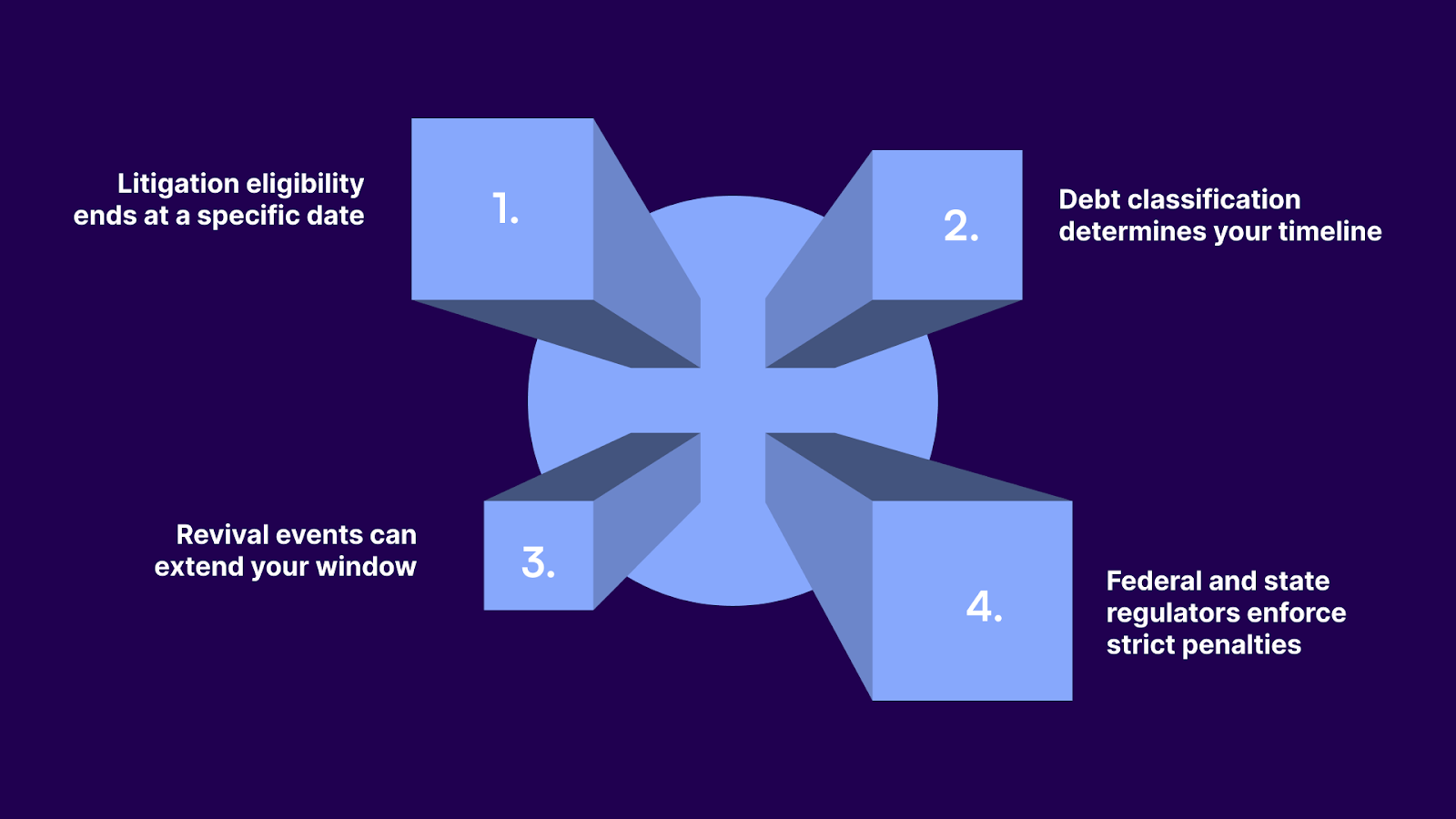

For collection agencies handling Illinois placements, statute-of-limitations rules are a common source of this risk. When litigation deadlines are miscalculated or debt is misclassified, otherwise valid recovery efforts can quickly turn into compliance exposure.

This guide explains how the Illinois statute of limitations works, why it matters operationally for collection agencies, and where timing mistakes most often create regulatory risk.

The statute of limitations plays a direct role in how collection agencies manage Illinois accounts. Understanding these deadlines helps agencies decide which accounts to prioritize, when to escalate efforts, and how to stay compliant with state and federal law.

Taken together, these factors make statute-of-limitations tracking a core operational requirement. To manage Illinois accounts effectively, agencies must first understand how the statute actually runs and when it begins under state law.

The statute of limitations is a legal deadline that determines how long a creditor or collection agency can file a lawsuit to recover unpaid debt. It does not erase the debt or prevent agencies from attempting collection through phone calls, letters, or payment plans. It only restricts access to the court system.

In Illinois, the statute of limitations begins when the cause of action accrues. For most consumer debt, this occurs on the date of the last missed payment or the date the contract was breached. Once the limitation period expires, the debt becomes time-barred. Agencies can still contact the consumer and request payment, but they cannot file a lawsuit or threaten legal action to enforce the debt.

Knowing when the statute begins and how long it runs is critical for managing Illinois accounts. Errors in calculating these timelines can lead to premature write-offs, wasted litigation costs, or compliance violations that expose your agency to legal liability.

Illinois law assigns different limitation periods based on the type of contract or agreement that created the debt. Correctly classifying debt is essential because using the wrong period can result in either premature abandonment of viable accounts or illegal litigation on time-barred debt.

Table showing limitation periods by debt category:

These distinctions mean that the same balance can yield very different enforcement timelines depending on its classification. Beyond classification, agencies must also account for events that can reset or pause the statute entirely.

Suggested Read: How Do Medical Bills Influence Credit Scores and Debt Recovery?

Certain consumer actions or legal events restart or pause the statute. These events extend your litigation window.

Under 735 ILCS 5/13-206, a partial payment accompanied by a written acknowledgment or new promise to pay the debt restarts the statute from that payment date.

Illinois courts require both the payment and clear evidence of intent to acknowledge the full debt obligation.

Examples:

The payment and acknowledgment must occur before the original statute expires to trigger a restart.

A written acknowledgment of the debt restarts the statute. The consumer must sign a document that clearly states they owe the debt.

Examples of valid acknowledgments:

What does not restart the statute:

When a consumer enters a new payment plan or modifies an existing arrangement, the statute restarts. Illinois courts treat these agreements as new promises to pay.

The arrangement must be in writing and signed by the consumer. Verbal payment plans do not restart the statute.

When a consumer files for bankruptcy, the automatic stay pauses the statute. The clock stops running and resumes only after the bankruptcy case is closed, dismissed, or discharged.

How this affects your timeline:

Illinois law allows tolling in limited circumstances:

These provisions are narrow and fact-specific. They require legal analysis before application.

Suggested Read: Statute of Limitations on Debt Collection: How Long Can Debt Be Collected?

Once debt becomes time-barred, agencies lose the right to pursue litigation. However, they retain the ability to contact consumers, request payment, and negotiate settlements. Recognizing these limits is essential to remaining compliant with both federal and state laws.

The difference between lawful collection and a compliance violation often comes down to wording, timing, and system controls. These risks are compounded by overlapping federal and Illinois laws that expand liability well beyond a single account.

Statute-of-limitations errors create risk beyond a single compliance failure. In Illinois, the same misstep can expose collection agencies to overlapping enforcement, litigation, and licensing consequences under multiple laws.

Here are the laws that you need to know to eliminate the risks.

Together, these laws amplify the impact of statute-of-limitations errors. Managing statute-of-limitations risk under this layered legal framework requires more than policy awareness. Agencies need system-level controls that enforce timing rules consistently across accounts, workflows, and communication channels.

Tratta supports this by translating legal limitations into operational guardrails, restricting escalation paths, logging consumer activity, and maintaining auditable timelines tied to each account’s legal status. Schedule a demo today.

Suggested Read: Exceptions to the Statute of Limitations: Key Insights

Collection agencies handling thousands of Illinois accounts need systems and workflows that prevent statute-of-limitations violations. Manual tracking is not sufficient. Agencies must use technologies such as Tratta, internal controls, and compliance protocols to manage deadlines at scale.

Here are a few things you can do to manage your accounts:

These practices are difficult to execute consistently without centralized data, automated controls, and real-time visibility. That is where technology platforms like Tratta, purpose-built for compliant debt recovery, become critical.

Tratta is a digital debt collection platform designed for agencies, law firms, and credit issuers. It centralizes consumer data, communications, payments, and workflow actions in one system, helping agencies track statute-of-limitations deadlines and maintain compliance across Illinois placements.

The features help agencies to take prompt actions in time-sensitive situations:

A centralized portal gives consumers direct access to balances, payment options, and account details without requiring agent contact. All consumer actions are logged automatically, creating a complete record of payment activity and engagement. When consumers make payments or acknowledge debt through the portal, these revival events are captured immediately.

Payment functionality integrated directly into the platform allows consumers to submit payments without leaving the system. Each transaction is time-stamped and recorded instantly, providing clear documentation of when payments occur. This real-time capture is critical for tracking events that restart the statute.

Interactive voice response in multiple languages removes communication barriers that can delay payment on accounts approaching statute deadlines. Consumers can complete transactions in their preferred language, reducing friction and improving completion rates across different consumer segments.

Communication across email, SMS, IVR, and portal messaging is tracked and stored in each account record. This creates a complete history of consumer interactions, enabling identification of written acknowledgments or statements that may reset the limitation period. Communication logs become evidence when disputes arise.

Automated campaign tools segment accounts by age, debt type, and statute status, then apply structured outreach based on those attributes. Campaigns can include rules that block litigation threats on time-barred accounts while continuing non-litigious contact. This prevents workflow-level compliance violations.

Real-time dashboards surface account age, payment patterns, and statute status across entire portfolios. Reports show which accounts are approaching limitation deadlines, allowing teams to prioritize escalation decisions before enforcement windows close. This visibility supports proactive management rather than reactive responses.

Configurable workflows and rules allow agencies to apply Illinois-specific limitation periods based on debt type. Custom fields track the default date, last payment date, and acknowledgment date. Automated calculations update limitation deadlines when revival events occur, reducing manual tracking errors.

API connections pull account data from creditor systems, legal platforms, and CRM tools into a single view. This eliminates manual data transfers that introduce timing errors or missing information. Accurate, synchronized data ensures statute calculations reflect the current account status.

Role-based access controls, audit trails, and encrypted data storage protect sensitive account information while maintaining records required for regulatory reviews. Documentation of consumer interactions, payment activity, and workflow decisions supports compliance with FDCPA, Illinois Collection Agency Act, and CFPB regulations.

Statute-of-limitations management depends on consistent execution. Tratta centralizes timing, activity, and account status to help agencies move enforceable accounts forward while restricting actions on accounts that fall outside legal limits.

Illinois statute-of-limitations rules determine when collection agencies can pursue litigation and when they must rely on non-litigious recovery methods. Agencies that misclassify debt, ignore revival events, or file suit on time-barred accounts face regulatory enforcement. Managing these deadlines at scale requires accurate data, clear policies, and technology that tracks account age and payment activity in real time.

Tratta supports statute-of-limitations management by centralizing consumer interactions, automating deadline calculations, and providing real-time visibility into account status. It further reduces compliance risk, improves recovery rates, and maintains stronger relationships with creditors.

If your agency handles Illinois placements, ensure your systems accurately track statute-of-limitations deadlines and prevent legal action on time-barred accounts. Schedule a demo to see how Tratta helps collection agencies manage compliance and optimize recovery workflows.

The applicable statute usually follows the consumer’s residence or the contract’s governing-law clause, and applying the wrong jurisdiction can invalidate litigation and increase compliance exposure.

No. Charge-off is an accounting action. The statute generally begins at default or last payment, making charge-off an unreliable trigger for limitation calculations.

Portfolio data often contains gaps, misclassified debt types, or incomplete payment histories, requiring independent verification before litigation decisions or escalated recovery activity occur.

No. Consumer consent does not override prohibitions on lawsuits, threats, or misrepresentation once a debt is time-barred under federal and applicable state law.

Accurate records of default dates, payments, communications, governing law, and tolling events provide defensible support during audits, disputes, litigation challenges, and regulatory reviews.