Errors in debt collection most often arise where timing and legal enforceability overlap. According to the CFPB’s 2025 FDCPA Annual Report, complaints related to taking or threatening legal action ranked among the most common debt collection issues in 2024, accounting for 7% of the 207,800 complaints received that year. These complaints frequently stem from disputes over whether a debt was still legally enforceable at the time of collection.

For collection agencies, law firms, and credit issuers handling Alabama accounts, missteps in handling statutes of limitations are a recurring source of this risk. When breach-of-contract timelines are miscalculated or debts are misclassified, accounts that appear recoverable can become time-barred, exposing agencies to regulatory scrutiny and lost enforcement rights.

This guide explains how the Alabama statute of limitations for breach of contract applies in a collections context, why it matters operationally, and how agencies can manage contract-based receivables without crossing compliance boundaries.

In Alabama, the statute of limitations for breach of contract is the time window during which a creditor or debt collector can file a lawsuit to enforce payment when a contract is violated. Once this window closes, the debt may still exist, but its legal enforceability can change significantly.

For debt collection agencies, this concept is critical. Many accounts placed for collection stem from unpaid contractual obligations, such as service agreements, financing arrangements, or commercial contracts. The statute of limitations determines whether those receivables can be pursued through legal action or must be handled through alternative, non-litigation strategies.

Alabama law applies different limitation rules depending on factors such as the type of contract involved and how it was formed. Because of this, correctly identifying the nature of the underlying agreement is an essential first step in evaluating any contract-based debt.

From an operational standpoint, the statute of limitations helps agencies:

Once breach-of-contract debts are correctly identified, the next consideration is how Alabama law applies different limitation periods based on contract type.

Not all debts in your portfolio fall under breach of contract claims. The classification matters because it determines which statute of limitations applies and what evidence you need to pursue legal action.

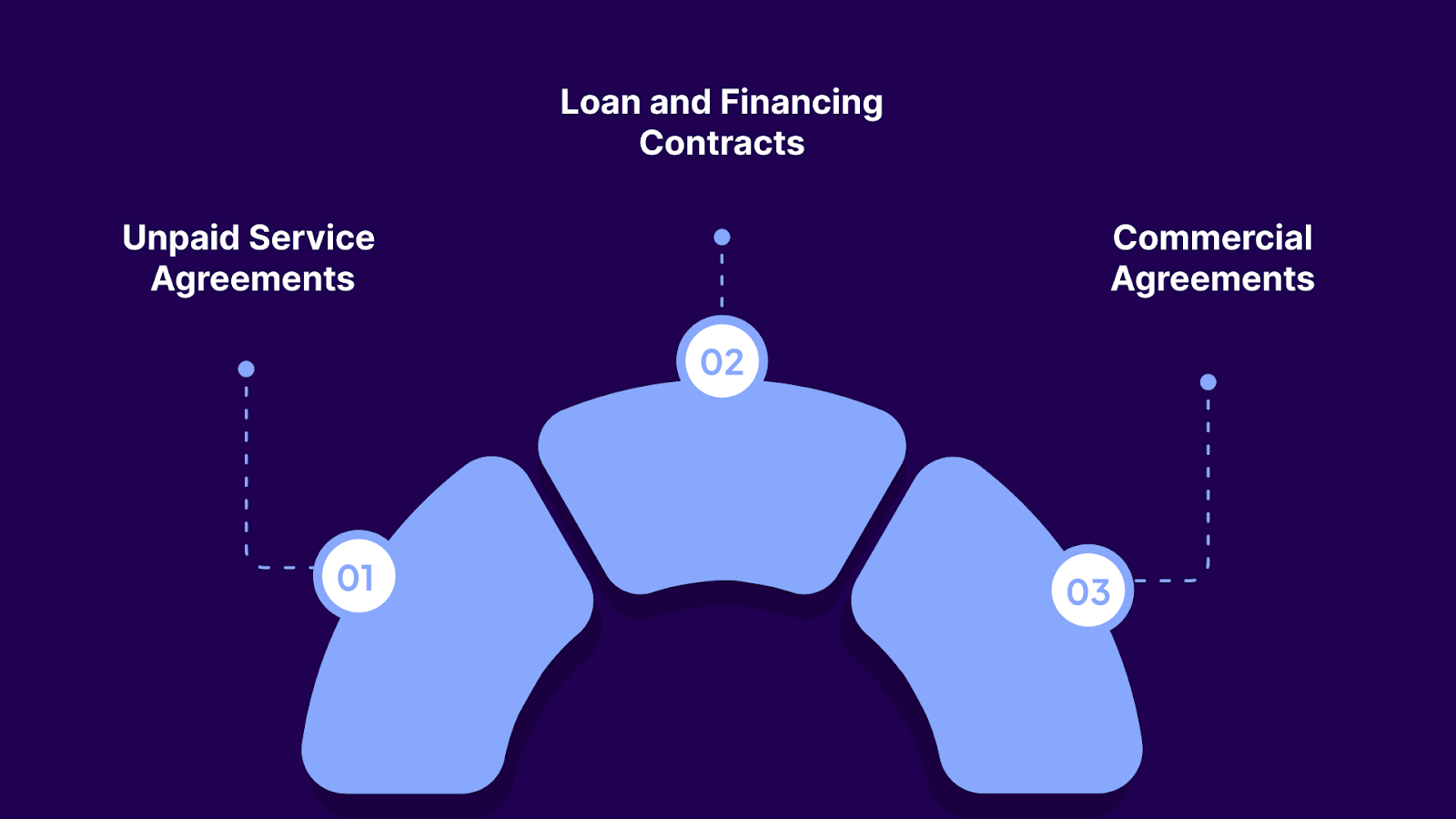

Breach of contract debt arises when one party fails to fulfill obligations outlined in a valid agreement. For collection agencies, these typically include:

Service contracts create payment obligations in exchange for specific deliverables. These include maintenance agreements, subscription services, professional services contracts, and vendor agreements. When a customer stops paying for services rendered under a written or oral agreement, a breach-of-contract debt arises.

Consumer and commercial loans account for the most common breach-of-contract debts in collections. This category covers personal loans, auto financing agreements, equipment financing, and lines of credit. The existence of a promissory note or loan agreement establishes the contractual obligation to repay.

Business-to-business contracts for goods, supplies, or ongoing services often result in significant breach-of-contract debt. These agreements usually include net payment terms like Net 30 or Net 60. When businesses fail to pay within those terms, the debt is referred to collections as a breach-of-contract claim.

The contract type determines both the applicable statute of limitations and the burden of proof required in litigation. Written contracts with clear terms are easier to enforce than oral agreements, which require additional evidence to establish their existence and terms.

Suggested Read: Statute of Limitations on Debt Collection: How Long Can Debt Be Collected?

Alabama law applies different limitation periods based on how the contract was formed and what it covers. Understanding these distinctions helps you classify accounts correctly and take appropriate action before deadlines expire.

These limitation periods illustrate why contract classification is not a clerical task but a legal and operational decision. As account volume grows, tracking limitation periods by contract type becomes increasingly complex to manage manually.

Tratta supports this process by allowing agencies to capture contract attributes at placement, track key dates centrally, and maintain clear visibility into statute-of-limitations status across portfolios. This helps teams prioritize enforceable accounts while avoiding action on debt that falls outside legal limits. Schedule a free demo to see how it works in practice.

Suggested Read: Exceptions to the Statute of Limitations: Key Insights

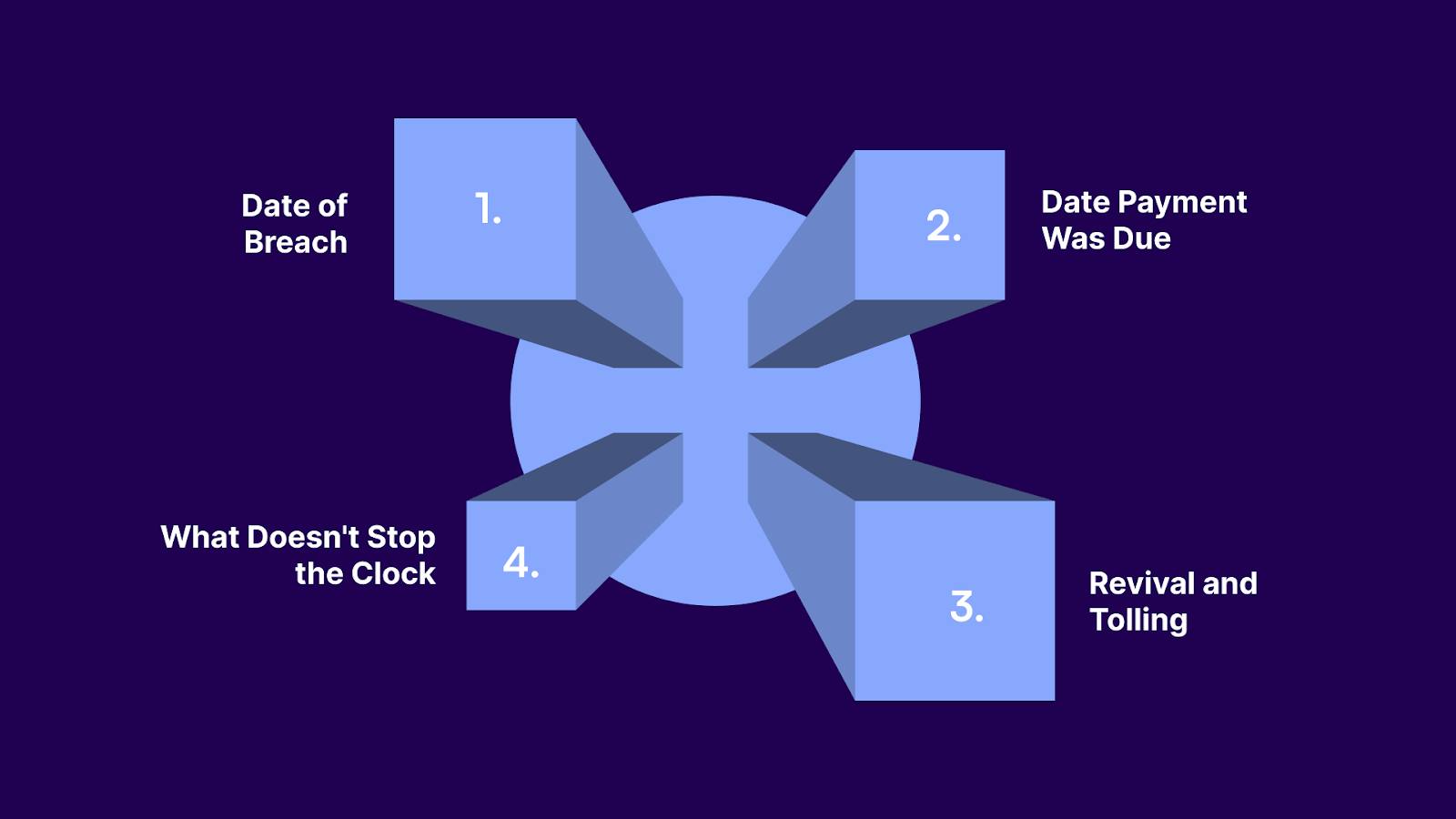

The statute of limitations begins when the breach occurs, not when the contract was signed. For debt collection, this typically means the date of the first missed payment or the date a required payment was due but not received.

Alabama courts start the clock from the date of the breach, the due date of the first missed payment. If a borrower made a payment on January 1, 2020, but missed the February 1, 2020, due date, the limitations period begins to run from February 1, 2020 (the date of breach). Under a six-year statute, your agency would have until February 1, 2026, to file suit.

The technical trigger is the date the breach occurred. For payment obligations, that's when a required payment was missed, not when the debtor made their last payment. This distinction matters for accounts with irregular payment patterns. If someone skipped payments and then resumed paying, the statute may revive with each new payment in some circumstances.

Under Alabama case law, the statute restarts only through:

Agencies must document the debtor's intent through signed acknowledgments or payment agreements with corresponding promises. Mere payment without acknowledgment typically fails to revive.

Certain actions do not toll or stop the statute of limitations:

If a debtor moves out of Alabama during the limitations period, the time they spent outside the state generally does not extend your deadline. The clock continues running.

Your agency needs documented proof of when the statute began and any events that may have revived it. Account notes, payment ledgers, and signed documents become critical evidence if you need to prove timeliness in court.

Even with accurate trigger dates and documentation, statute-of-limitations deadlines eventually expire. At that point, the collection strategy and legal obligations change significantly.

When Alabama's statute of limitations on a breach-of-contract debt expires, the debt becomes time-barred. This creates specific legal restrictions on your collection activities while leaving some options available.

A time-barred debt is one where the statutory deadline to file a lawsuit has passed. The debt still exists, and the debtor still owes the money. However, you cannot legally sue to collect it. According to Regulation F § 1006.26(b), debt collectors are prohibited from suing or threatening to sue on time-barred debt, even if state law would technically allow the filing.

Once the statute expires, your agency faces clear limits:

The Consumer Financial Protection Bureau affirmed that bringing or threatening legal action on time-barred debt violates the Fair Debt Collection Practices Act, regardless of whether your agency knew the debt was time-barred.

Despite these restrictions, you can still attempt collection on time-barred debt through non-legal channels:

While federal Regulation F does not mandate specific time-barred-debt disclosures in all cases, certain states and localities do. Some collection agencies voluntarily disclose time-barred status to reduce compliance risk. The CFPB noted that, depending on the circumstances, agencies may need to disclose their inability to sue to avoid violating FDCPA prohibitions on false or misleading representations.

Time-barred debt can become enforceable again if the debtor takes specific actions. If a debtor makes a payment, provides a written acknowledgment, or signs a new payment agreement, they may inadvertently restart the statute of limitations. This creates ethical considerations. Your agency should not mislead debtors about the consequences of payment or trick them into reviving time-barred debt.

Now that you know exactly what happens when SOL expires, let's understand what you can do before or after its expiration.

Statute-of-limitations status directly affects which collection actions are permitted and which create compliance risk. Different stages of the statute of limitations require different operational controls to remain compliant.

The period before the statute expires represents the strongest legal position for a collection agency. During this stage, all lawful enforcement options remain available, including litigation where appropriate.

Tratta's platform helps agencies manage statute-of-limitations risk by maintaining comprehensive account histories, tracking key dates, and providing visibility into account status. The system flags accounts approaching limitation deadlines, enabling strategic action before enforcement rights expire. Book a free demo to explore the features.

Once the statute expires, your approach shifts to voluntary collection with strict compliance controls.

The operational discipline required to manage statute-of-limitations risk properly increases as portfolios grow. Manual tracking breaks down at scale, creating compliance gaps that regulators and consumer attorneys exploit.

Suggested Read: How Do Medical Bills Influence Credit Scores and Debt Recovery?

Even well-intentioned debt collection agencies face compliance risks under the statute of limitations. Most violations arise from process breakdowns, not deliberate misconduct. In Alabama, these risks can quickly lead to regulatory scrutiny, litigation, and financial exposure.

Let's look at some of the compliance risks:

Filing suit after the statute of limitations has expired is one of the most serious compliance violations. Liability can attach even when the expiration was missed due to tracking errors or incomplete data.

Statements or correspondence that suggest lawsuits, judgments, or enforcement on time-barred debt are prohibited. This includes language that indirectly implies legal escalation rather than explicitly stating it.

Applying the wrong statute of limitations due to incorrect contract classification can result in agencies pursuing debts that are no longer legally enforceable. These errors often stem from assumptions rather than documented review.

Partial payments, written acknowledgments, or revised payment arrangements can restart limitation periods. Missing these events leads to inaccurate expiration calculations and compliance exposure.

Without reliable documentation of when the default occurred, agencies cannot confidently determine the limitation status. Weak documentation makes SOL determinations difficult to defend if challenged.

Manual tracking of statute-of-limitations deadlines does not scale. Without automated flags, calculation controls, and audit trails, agencies are more likely to make enforcement errors.

As portfolios grow and span multiple jurisdictions, the risk of statute-of-limitations issues increases. Agencies operating in Alabama benefit from compliance frameworks that account for state-specific limitations while maintaining consistent operational oversight.

Debt collection agencies need technology that automatically enforces compliance with the statute of limitations while preserving recovery opportunities for enforceable debt.

Tratta supports this need by bringing account data, payments, communications, and operational rules into a single system.

Here’s how Tratta’s capabilities support statute-aware collection workflows in practice.

Tratta’s self-service portal allows consumers to review balances and take action without involving an agent. Payments and account interactions are recorded automatically, ensuring payment activity and acknowledgments are captured as they occur. This creates a reliable activity trail for statute-of-limitations evaluation.

Payments processed directly within the platform are logged instantly with precise timestamps. Real-time recording reduces uncertainty around payment timing and eliminates delays caused by external payment systems, an essential factor when determining whether limitation periods have been affected.

By offering IVR payment options in multiple languages, Tratta helps remove communication barriers that can slow resolution on aging accounts. Faster payment completion reduces friction on accounts approaching statutory deadlines.

All outreach and responses, across email, SMS, IVR, and portal messaging, are stored within the account record. This consolidated communication history helps teams identify written acknowledgments and maintain documentation if the limitation status is questioned.

Campaign tools enable agencies to segment accounts by age, contract type, and statute status. Outreach rules can restrict litigation-related language on time-barred accounts while enabling compliant communication to continue, reducing workflow-level risk.

Custom fields and rules track key dates, including the default date, last payment date, and acknowledgment dates. When new activity occurs, workflows can automatically update account status, minimizing the need for manual recalculation.

Dashboards surface account aging, recent activity, and statute-related indicators across portfolios. Teams can identify accounts nearing enforcement cutoffs early and make informed prioritization decisions.

System-level controls prevent prohibited actions on expired accounts:

These guardrails protect agencies from FDCPA violations caused by collector error or system gaps.

Tratta integrates with your existing collection management platform, CRM, or ERP system through REST APIs. Account data, payment history, and limitation period calculations sync automatically, eliminating duplicate data entry and ensuring consistency across systems.

Managing statute-of-limitations risk depends on consistency across people, processes, and data. By centralizing account timelines and enforcing workflow controls, Tratta helps agencies advance enforceable accounts while limiting exposure to time-barred debt.

The Alabama statute of limitations breach of contract draws a firm line between accounts that still support legal recovery and those that require a different approach. Where agencies struggle is not with awareness of that line, but with maintaining accuracy as accounts age, change hands, or trigger new activity.

Consistency at scale is the real differentiator. Portfolios that rely on manual tracking or disconnected systems are more likely to miss deadlines, misapply limitations, or introduce compliance risk through workflow gaps.

Tratta is built to support that consistency by centralizing account timelines, statute-related activities, and enforcement controls in a single system. This allows teams to operate with clarity around enforceability while reducing reliance on manual checks and assumptions.

Schedule a free demo today if your organization manages Alabama contract debt and needs a more reliable way to control statute-of-limitations risk across growing portfolios.

Yes. Time-barred or near-expiration accounts typically have lower recovery values and higher compliance risks, directly impacting portfolio pricing and prioritization decisions.

Yes. Reviewing limitation status before placement prevents wasted legal spend and reduces the risk of assigning already time-barred accounts.

Yes. New written payment agreements or acknowledgments can restart limitation periods, requiring recalculation and updated enforcement timelines.

Regularly. Status should be revalidated whenever payments, acknowledgments, transfers, or workflow changes occur, to ensure that the enforceability assumptions remain accurate.

Inconsistent contract classification, incomplete breach-date data, and manual tracking across systems create the highest exposure at scale.