Delinquent non-tax debt owed to the U.S. federal government hit $216.1 billion at the end of fiscal year 2023, an 11% jump from the previous year. Collection agencies and creditors face the same trend: accounts are aging faster, recovery windows are narrowing, and delays cost real money.

Your agency places thousands of accounts every month. How many actually move within the first week? How many consumers want to pay but cannot reach an agent during business hours or set up a payment plan through your portal at 9 p.m.?

Speed separates agencies that hit recovery targets from those that struggle. When accounts age past 90 days, recovery rates drop by half. The problem is not placement volume. The problem is accelerating receivable collection by removing friction, offering flexible payment options, and letting your team work on the accounts that matter most.

In this guide, we will show you precisely what slows down receivable collections and the strategies that fix it.

Accelerating receivables means reducing time-to-payment, improving recovery rates, and lowering the cost per collected dollar. You achieve this by creating faster pathways to right-party contact, offering immediate payment options, and automating follow-up across multiple channels.

For your agency, acceleration shows up in three places: shorter time-to-first-payment, higher conversion on payment arrangements, and lower operational cost per account. This requires systems that let consumers resolve debts quickly on their terms while giving your team tools to prioritize accounts effectively.

The goal is not more aggressive outreach. It is about removing friction from the payment process so accounts move through your collection cycle faster.

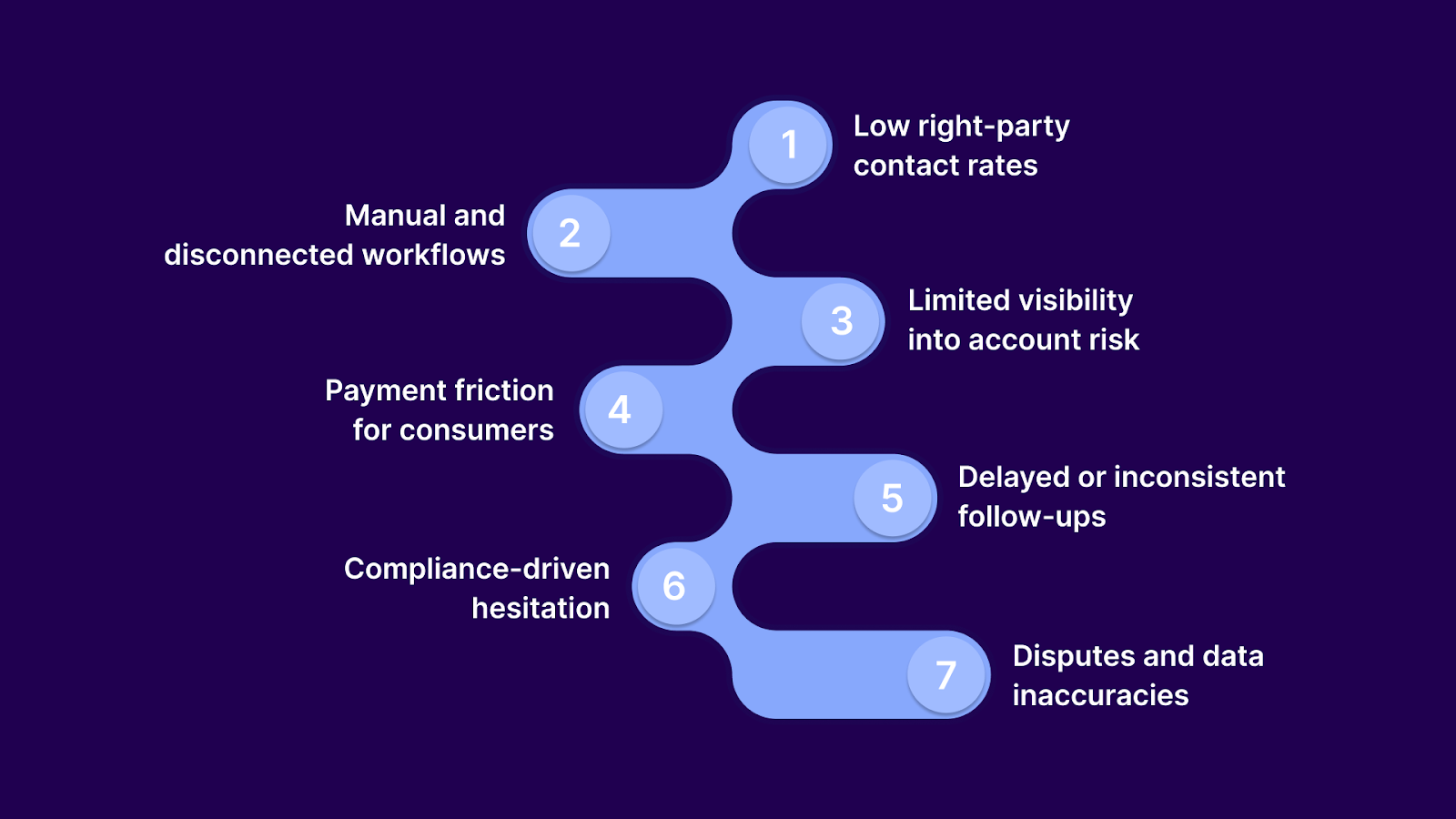

Even with experienced teams in place, receivable collections often slow down due to process gaps, system limitations, and external constraints. In most cases, delays aren’t caused by lack of effort; they’re caused by friction in how collections are executed.

Common reasons receivable collections slow down include:

These challenges compound over time, making it harder to recover balances efficiently. Addressing them is the first step toward accelerating receivable collections in a way that’s both effective and compliant.

Suggested Read: How To Calculate Average Net Accounts Receivable: Definition, Formula & Examples

Reducing time-to-payment requires combining communication strategies, workflow automation, consumer-centered payment options, and data-driven prioritization. These strategies represent actionable approaches you can implement to accelerate receivable collections.

Phone calls alone limit your ability to reach consumers quickly. Most people check their email and text messages multiple times per day, often more frequently than they answer unknown phone numbers.

Ways to expand reach:

However, executing a proper omnichannel strategy requires more than adding new tools; it requires coordination. That’s why Tratta centralizes email, SMS, IVR, and portal interactions in a single system, ensuring your outreach remains consistent, measurable, and compliant across every channel. Book a demo to see how it works in practice.

Suggested Read: Understanding IVR Payment Systems: Enhancing Customer Experience & Streamlining Payments

Manual outreach limits how quickly you can contact consumers. If your team manually sends every follow-up email or reminder, accounts sit idle while agents work through their daily task lists.

What automation delivers:

Automation ensures every account receives timely outreach without manual intervention, reducing average time from placement to first payment.

Consumers who want to resolve debts often delay payments because they cannot reach an agent during business hours or cannot afford a lump-sum payment.

Self-service removes these friction points:

Multi-Service Fuel Card saw this impact firsthand. After switching to Tratta's self-service platform, debit card payments nearly doubled to almost 40%. The result was an additional $650,000 collected in just seven months. As their Director of Risk Management noted, the platform eliminated the need for customers to speak to an agent for most payment transactions.

Tratta's consumer self-service platform and embedded payment features provide consumers with secure, easy-to-use tools for managing payments independently. This reduces operational costs while improving payment completion rates. Schedule a demo to see how these features work together in your environment.

Treating all accounts equally wastes agent time on low-yield accounts and delays action on high-potential balances.

Prioritize with data:

Generic follow-up messages sent at arbitrary intervals do not drive action. The timing and content of your follow-ups should respond directly to consumer behavior and account status.

Structure your cadences around triggers:

When you catch consumers while the account is fresh in their mind, you increase the likelihood of immediate action and reduce unnecessary aging.

High contact rates are essential for fast collections, but aggressive outreach can lead to opt-outs, complaints, and compliance violations.

Maintain contact without burning bridges:

Fragmented systems slow down decision-making, create data gaps, and require agents to switch between multiple platforms.

A unified system delivers:

You cannot improve what you do not measure. The right KPIs help you identify bottlenecks and adjust strategies before they impact your entire portfolio.

Focus on metrics that matter:

Suggested Read: Top 10 KPI Metrics for Effective Tracking of Accounts Receivable

Compliance violations delay collections by triggering legal disputes, forcing operational pauses, and damaging creditor relationships.

Automate compliance to maintain your outreach:

When you apply these strategies effectively, you can move accounts faster and capture payments more reliably. However, even the best tactics stall if your systems aren’t set up to support them. That’s where a platform like Tratta helps you put these strategies into action and see real results.

Accelerating the collection of receivables requires more than knowing the right strategies. Agencies and creditors need infrastructure that removes friction, supports digital-first consumer behavior, and embeds compliance directly into daily workflows. Without that foundation, even well-designed collection strategies stall during execution.

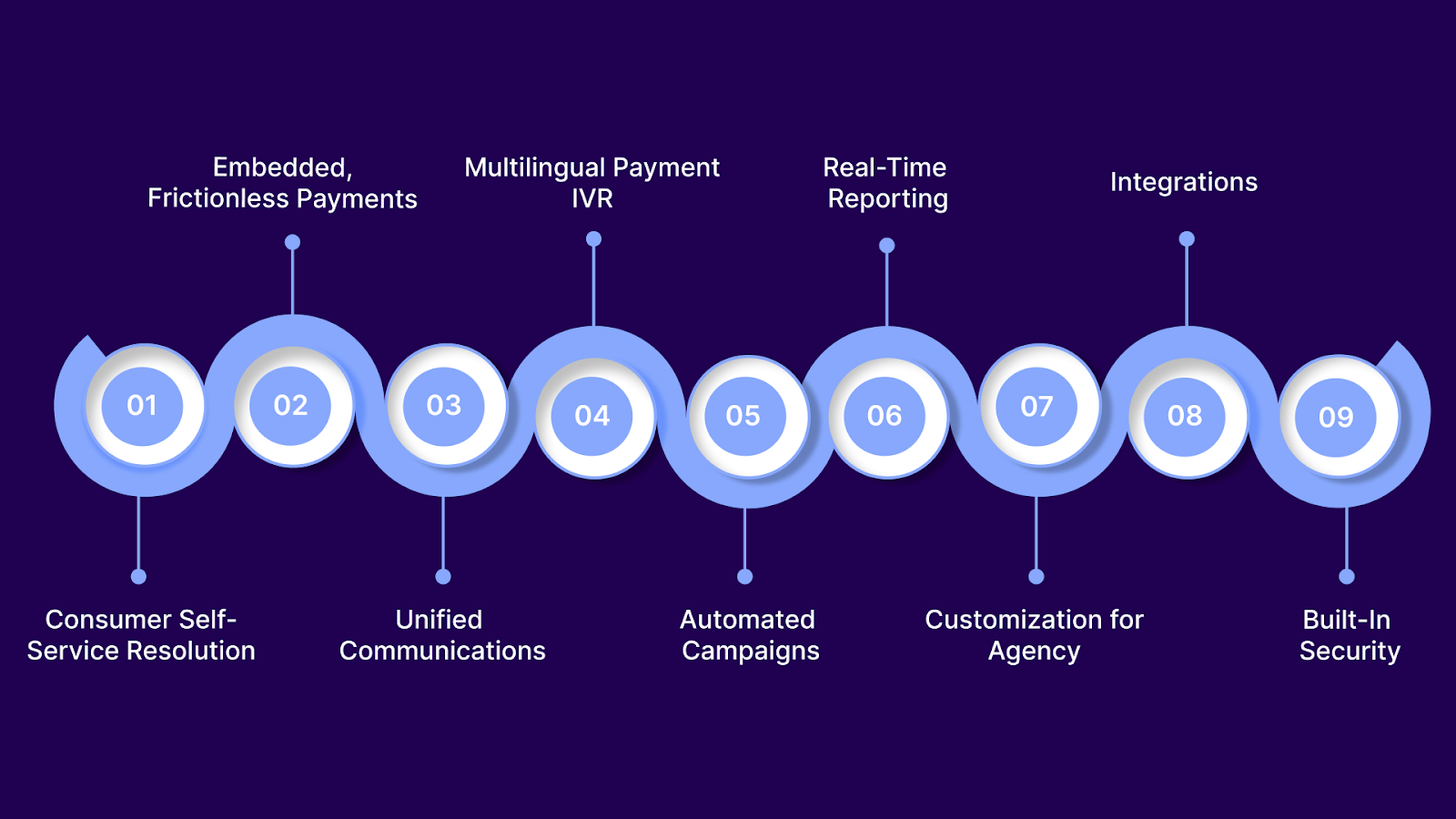

Tratta was built specifically to address these operational gaps in modern collections. The platform unifies communications, payments, analytics, and compliance into a single environment, reducing time-to-payment while maintaining regulatory control.

Tratta provides a secure, always-on consumer portal where individuals can view account details, review balances, make payments, and submit disputes without contacting an agent. By giving consumers control over how and when they resolve debts, agencies reduce delays caused by limited business hours and agent availability. This self-service model accelerates first payments and improves follow-through on payment arrangements.

Payment completion is a critical driver of receivables acceleration. Tratta embeds ACH and card payments directly within the collection experience, including portals, SMS links, email notices, and IVR flows. Consumers complete transactions without being redirected to external processors, reducing abandonment and shortening the path from engagement to settlement.

Tratta enables coordinated outreach across email, SMS, portal messaging, and IVR without requiring multiple disconnected tools. All consumer interactions are logged in a single system, giving teams a complete view of engagement history. This allows agencies to adjust channel mix based on response and payment behavior, increasing right-party contact rates and speeding resolution.

To support diverse consumer populations and capture payments outside business hours, Tratta includes multilingual IVR payment capabilities. Consumers can resolve balances independently in their preferred language, expanding accessibility while reducing reliance on live agents. This capability helps agencies collect more payments without increasing staffing costs.

Acceleration depends on timely follow-ups. Tratta’s campaign automation enables agencies to trigger outreach based on account events, such as placements, upcoming due dates, or missed payments. Automated sequences ensure consistent contact without manual intervention, keeping accounts moving through the collection cycle and reducing unnecessary aging.

Tratta surfaces real-time insights into payment activity, engagement patterns, and return-code trends through configurable dashboards. Teams can track time-to-first-payment, channel conversion rates, and recovery performance by segment. This visibility enables faster adjustments to prioritization and outreach strategies, improving overall recovery efficiency.

Collection operations vary by portfolio, creditor, and regulatory environment. Tratta allows agencies to configure authentication rules, payment plan parameters, settlement options, and workflow logic without custom development. This flexibility supports faster adaptation to changing requirements while maintaining consistent operational control.

Tratta integrates with existing AR systems, CRMs, and data providers through REST APIs. Agencies can synchronize placement files, payment data, and engagement signals without creating new silos. This ensures acceleration strategies work within existing infrastructure rather than requiring a full system replacement.

Compliance is embedded directly into Tratta’s workflows. The platform enforces communication timing rules, tracks consent and preferences, logs all interactions, and secures payment data through tokenization and role-based access. These safeguards allow agencies to maintain consistent outreach without slowing collections due to compliance uncertainty.

By removing structural barriers and unifying the systems that support collections, Tratta helps agencies and creditors execute proven acceleration strategies at scale. The result is faster time-to-payment, accelerated cash collection rates, and lower operational cost per account, without sacrificing compliance or consumer experience.

The gap between what your agency could collect and what you actually recover often comes down to speed. Every day, accounts sit unresolved, recovery rates decline, and operational costs climb. The agencies that have moved past legacy systems and manual workflows are the ones winning placements and maintaining strong creditor relationships.

Accelerating the collection of receivables requires tools built specifically for modern debt-recovery operations. Tratta consolidates everything you need into one platform. With the platform, you get shorter time-to-first-payment, higher self-service conversion rates, and lower cost per dollar collected without adding complexity to existing workflows.

If you are ready to close the gap between potential and actual recovery performance, schedule a free demo with Tratta to see how the platform works in your environment.

Yes. Digital payments are permitted when consent, disclosures, and validation notices are provided, communications comply with the FDCPA and Regulation F, and payment data is secured under PCI DSS.

No. Automation must respect call frequency limits, time-of-day rules, consent requirements, and opt-outs; compliant platforms enforce these automatically, reducing risk while maintaining consistent, lawful consumer engagement nationwide.

Yes. Consumers can self-enroll in payment plans if terms are clearly disclosed, payments are authorized, and modifications remain voluntary, documented, and compliant with creditor policies and laws.

The five C’s of accounts receivable management are Character, Capacity, Capital, Conditions, and Collateral, used to assess customer credit risk and guide payment terms and collection strategies.

Agencies should document consent, delivery, and access. Regulation F allows electronic notices if consumers receive required disclosures, can retain them, and are not charged for access fees.