Debt recovery has become more complex as consumer credit balances continue to grow and delinquency pressure persists. According to TransUnion’s 2026 Consumer Credit Forecast, U.S. credit card balances are projected to reach $1.18 trillion. Delinquency rates are expected to increase by one basis point to 2.57%.

This reinforces the need for more effective recovery approaches. Traditional collection methods that rely heavily on a single payment option, such as ACH, are often too rigid for today’s fragmented payment behavior.

Augmented cash collections combine smarter payment strategies, data-driven execution, and operational controls to reduce friction and improve outcomes. This article explores 7 augmented cash collection strategies that help agencies recover more efficiently in a changing credit environment.

Brief look:

Augmented cash collections enhance traditional collection methods by integrating more innovative payment strategies, data, and operational controls. Rather than relying on a single payment rail or manual follow-ups, this approach focuses on improving how, when, and why payments occur.

The goal is to increase successful recoveries while reducing friction and compliance risk. These are the limitations of traditional approaches:

These limitations highlight why incremental improvements are no longer enough. In the next section, we look at scenarios in which you should be concerned about your existing collection approach.

Suggested Read: 8 Ways to Reduce DSO for Faster Payments

Cash collection breakdowns surface as a gradual performance drag across recovery, compliance, and agent productivity. The indicators below signal when your current approach is constraining recovery outcomes.

When these signals appear, tactical adjustments are rarely enough. This is the point where augmented cash collection strategies become necessary to restore efficiency, control, and recovery performance.

Suggested Read: Accounts Receivable Dashboard: Examples And Benefits

Augmented cash collections engineer payment outcomes by controlling timing, choice, friction, and compliance in ways traditional collection playbooks do not address.

The following strategies focus on execution leverage rather than surface-level improvements.

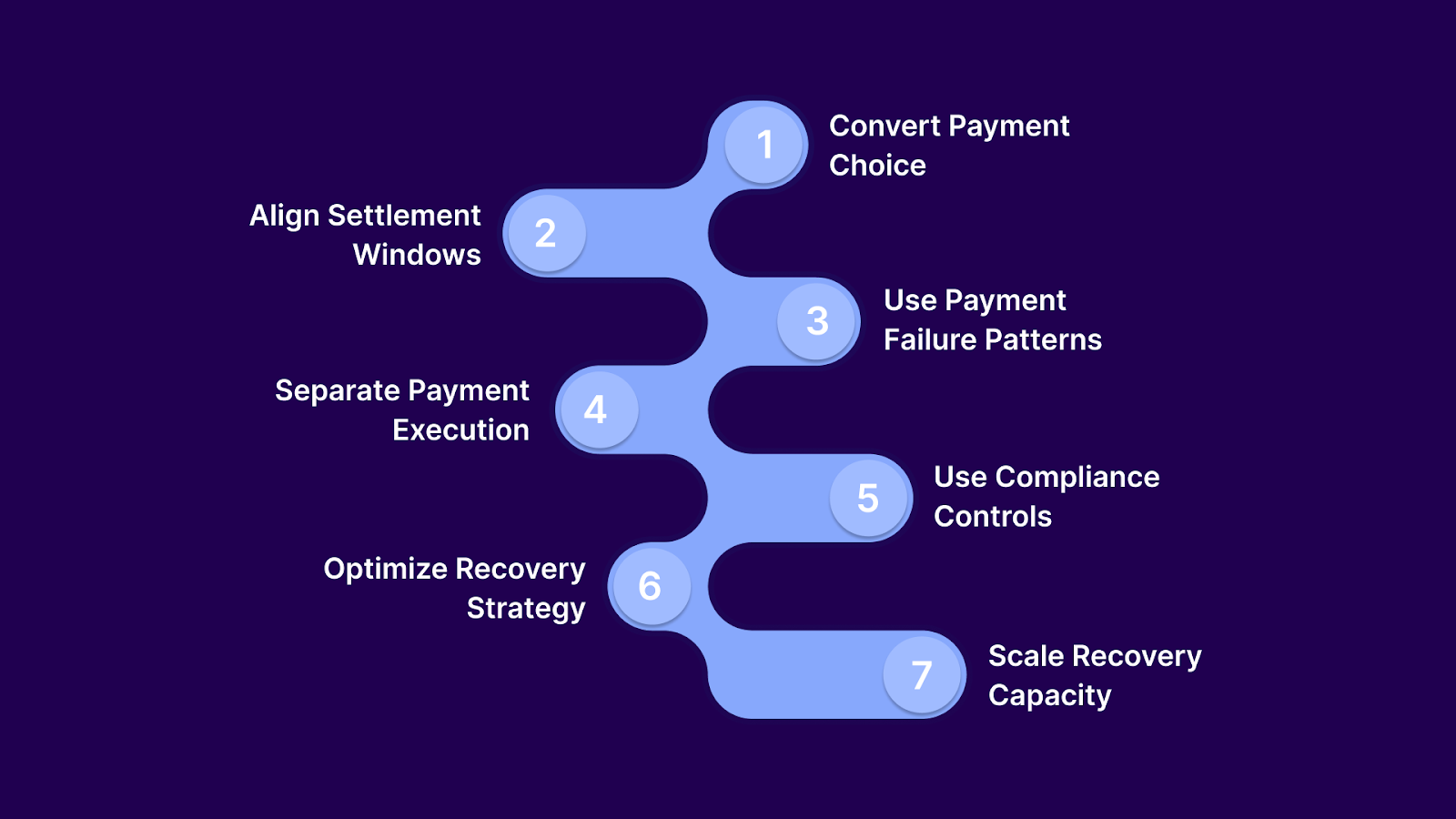

Most agencies treat payment choice as a passive option. Augmented collections use payment choice as a behavioral signal that predicts intent and readiness to resolve. When method selection is tracked and acted on, agencies intervene earlier and more precisely.

This strategy improves recovery by:

Traditional settlement offers expire by date. Augmented strategies tie settlement availability to payment certainty windows, where confirmation and funds are most likely to occur. This aligns with execution reality instead of static timelines.

Collectors improve outcomes by:

Further Insight: Understanding the Proposal for the Settlement Agreement in Business

Failed payments are usually treated as an operational issue. Augmented collections treat them as a predictive signal that a strategy is about to fail. This allows intervention before accounts stall or churn.

Agencies gain leverage by:

In many agencies, agents both negotiate and execute payments. Augmented collections decouple these functions so agents focus on resolution logic while execution follows controlled, standardized flows. This reduces error and increases throughput.

Recovery improves when agencies:

Compliance is often positioned as a constraint. Augmented strategies design compliance controls to reduce hesitation and abandonment, not just satisfy audits. When consumers trust the process, they complete payments more often.

This shifts outcomes by:

Further Insight: SMS Compliance Laws and Regulations

Most agencies measure success by dollars collected. Augmented collections measure how quickly accounts move from intent to completion. Faster velocity reduces risk, cost, and drop-off.

Managers improve performance by:

Growth usually increases exceptions. Augmented strategies design payment operations, so scale reduces variability rather than amplifying it. This allows agencies to grow volume without growing chaos.

Agencies achieve this by:

Tratta helps you put these strategies into practice by centralizing payment execution, choice, and compliance in one system. You can control how payments are offered, triggered, and completed without relying on manual workarounds or disconnected tools. Schedule a free demo.

Augmented cash collection strategies only work when they are translated into concrete operating rules. Implementation requires discipline across payment design, agent behavior, compliance, and measurement.

The steps below outline how collection agencies move from intent to consistent execution.

1. Map Payment Methods to Recovery Scenarios

Start by defining which payment methods are appropriate for settlements, repayment plans, and high-risk accounts. This prevents agents from improvising and ensures each account follows an execution path aligned with resolution intent.

2. Standardize Payment Execution Workflows

Replace ad-hoc payment handling with defined workflows that control how payments are initiated, authorized, and confirmed. Standardization reduces errors, improves consistency across agents, and makes outcomes more predictable.

3. Centralize Payment Visibility and Controls

Consolidate payment tracking so that all activity, including failures and partial payments, is visible in a single operational view. This allows supervisors to identify breakdowns early and intervene before accounts stall.

4. Embed Compliance at the Point of Payment

Capture authorization, disclosures, and documentation directly into payment workflows. This shifts compliance from a back-office cleanup task to a real-time control mechanism.

5. Train Agents on Execution Logic, Not Just Scripts

Educate collectors on why certain payment methods are used in specific scenarios, not just what to say. This improves judgment, reduces misaligned offers, and increases first-attempt success.

6. Monitor Early Signals and Adjust Quickly

Track indicators like failed payments, abandonment, and time-to-resolution by method and scenario. Use these signals to refine payment options and timing before performance degrades.

Once these steps are applied consistently, the benefits show up in measurable performance gains. The following section focuses on the specific metrics that improve when cash collection strategies are correctly operationalized.

Suggested Read: Real-Time Metrics and KPIs for Debt Collection Dashboard

Augmented cash collections are only valuable if they change measurable outcomes. When payment choice, execution, and compliance are engineered intentionally, improvements show up quickly across recovery, efficiency, and risk indicators.

The table below highlights the metrics that typically move first and explains why those gains occur.

To ensure these gains are sustained over time, agencies need to reinforce execution discipline:

When these guardrails are in place, augmented cash collection strategies remain effective instead of degrading quietly over time. The following section outlines when you should rethink your cash collection strategy before performance erosion becomes systemic.

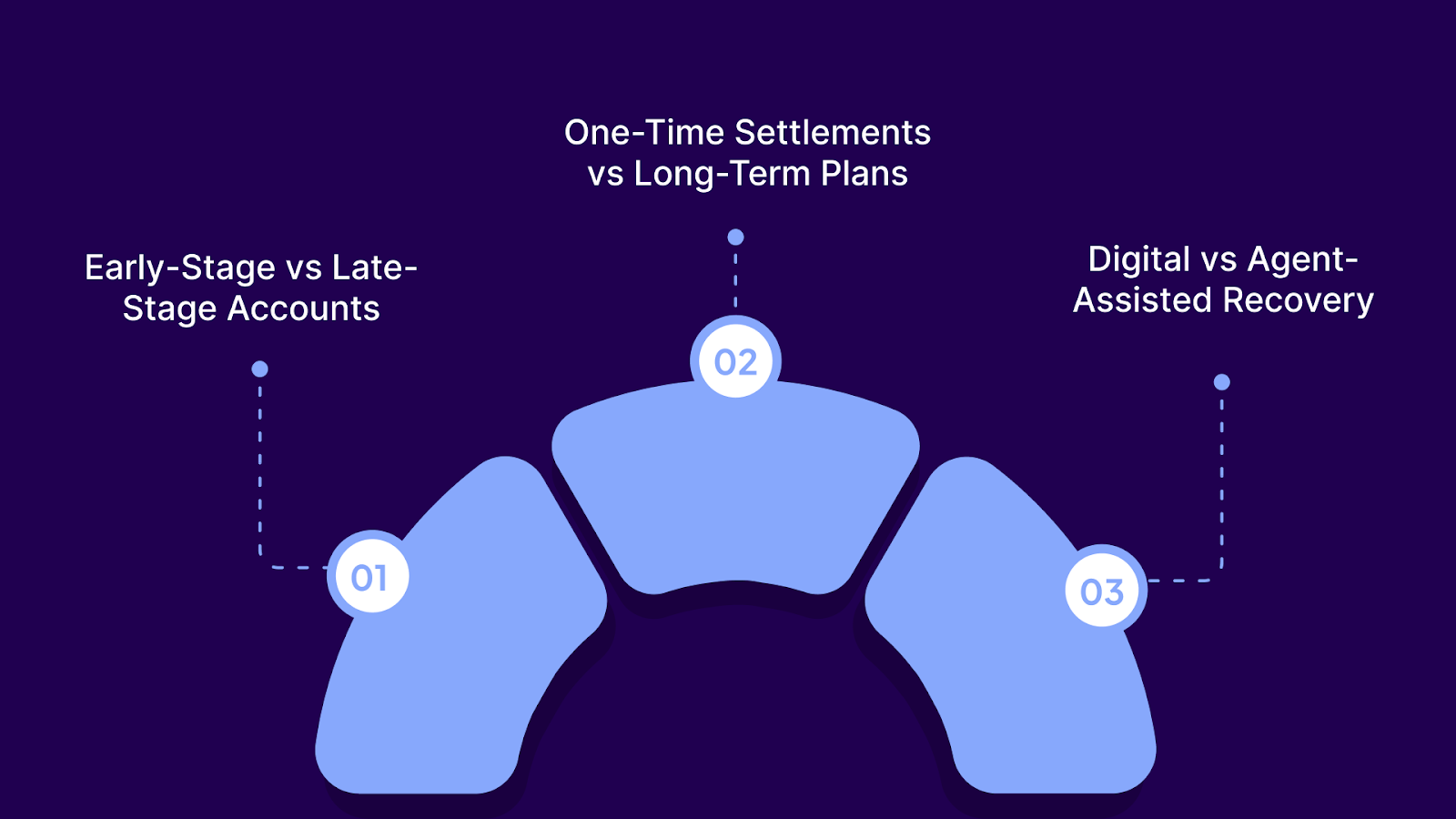

Augmented cash collections are most effective when applied selectively rather than uniformly. Their value increases in situations where payment intent, execution risk, and operational constraints vary significantly.

The scenarios below illustrate where augmentation has the most impact on outcomes.

Early-stage accounts benefit from reduced friction and faster execution, helping you convert intent before hesitation sets in. Late-stage accounts require higher payment certainty and tighter controls to avoid failed settlements and repeated renegotiation.

Augmented strategies allow you to apply different execution logic based on account age, rather than forcing a single recovery approach.

One-time settlements are highly sensitive to delays between agreement and payment completion.

Augmented cash collections improve certainty at the moment of execution, reducing drop-off after negotiation. Long-term plans benefit from structured, predictable payment handling that minimizes breakage over time.

Digital recovery depends entirely on frictionless execution, as there is no agent to intervene when payments stall.

Augmented strategies optimize self-service flows to increase completion without increasing contact volume. In agent-assisted recovery, augmentation standardizes execution so results do not depend on individual collector behavior.

Tratta supports stage-specific recovery through its Campaigns feature. You can design and automate outreach and payment engagement based on account age, balance, and recovery status. You can have early- and late-stage accounts follow different execution paths.

Augmented cash collection strategies often fail because execution breaks down in real-world conditions. Avoiding these mistakes is critical before layering in additional technology or complexity.

The challenges below reflect where agencies most commonly lose value after deciding to modernize.

Many agencies assume augmentation means adding new payment methods. This overlooks the execution logic needed to decide when, how, and for whom those methods are used.

To correct this, you must reframe augmentation as a recovery strategy, not a menu expansion:

When agents control how payments are executed, outcomes vary widely, and compliance risk increases. Inconsistent handling creates unpredictable recovery performance and rework.

To avoid this, execution must be system-driven, not agent-dependent:

Layering new methods or processes without centralized tracking creates blind spots. Agencies often realize too late that failures are increasing, but cannot pinpoint where or why.

Prevent this by consolidating oversight before scaling execution:

When compliance checks happen after execution, remediation becomes costly and reactive. This approach increases audit exposure and slows recovery cycles. Compliance must be enforced at the moment of payment to be effective.

You should:

Focusing only on dollars collected hides inefficiencies and risk. High volume can mask growing failure rates and operational strain. Shift measurement toward execution quality to sustain performance.

You need to:

While these pitfalls highlight where augmented strategies often go wrong, they also point directly to the solution: smarter use of technology.

Instead of relying on manual processes or fragmented tools, agencies can use software to automate repayment plans, strengthen compliance oversight, and improve consumer engagement.

Tratta is a debt collection and recovery platform designed to turn strategy into execution at scale. It brings payments, compliance, consumer engagement, and visibility into a single operating system. This allows for augmented cash collection strategies to be applied consistently across accounts, stages, and channels.

Core features include:

Gives consumers a secure, intuitive way to view balances and complete payments without agent involvement. This reduces friction and increases completion rates, especially in digital-first recovery.

Centralizes acceptance of ACH, cards, and supported alternatives within one compliant framework. This eliminates gateway sprawl and simplifies reconciliation.

Allows consumers to make payments by phone in their preferred language. This expands accessibility while keeping payment data synchronized in real time.

Coordinates email, SMS, and voice outreach into a unified engagement layer. Messaging stays consistent, compliant, and tied to payment activity.

Enables rules-based, automated campaigns driven by account attributes such as age, balance, and recovery stage. This supports stage-specific execution without manual segmentation.

Provides real-time visibility into payment performance, failures, and trends. Teams can adjust strategy based on execution data, not lagging reports.

Allows agencies to tailor workflows, messaging, and consumer experiences to their operating model. Strategies adapt without forcing rigid, one-size-fits-all processes.

Connects securely with CRMs, internal systems, and external tools through APIs. Data flows cleanly without manual handoffs or duplication.

Embeds authorization controls, audit trails, and data protection into every workflow. Compliance is enforced during execution, not after the fact.

The accurate measure of their value lies in how they translate strategy into tangible recovery gains, as demonstrated in the following case study.

When MS Fuel Card (part of Shell), a diesel card provider serving commercial fleets, experienced high ACH return rates and manual recovery workflows, collection performance stalled.

After implementing Tratta, the company shifted more volume to card-based and self-service payments. Within seven months, card payments nearly doubled, rising from roughly 20% to almost 40% of total collections, and the organization recovered over $650,000 more than it had through its previous card processor.

Self-service payment links embedded in digital outreach reduced call dependency and data-entry errors, while centralized reporting improved visibility into execution. The result was faster recovery driven by better payment execution, not increased pressure.

Augmented cash collections give you a way to recover more efficiently by aligning payment choice, execution, and compliance with how consumers actually pay. When these elements are engineered intentionally, you reduce friction, shorten resolution timelines, and improve predictability.

Tratta turns augmented strategies into consistent execution by centralizing payments, engagement, controls, and visibility in one operating system. You gain the flexibility to adapt by account stage and recovery path without introducing fragmentation or risk.

See how augmented cash collection strategies work in practice, not just on paper. Speak to our team to understand how your collection strategy performs when execution is no longer the weak link.

Automation focuses on doing the same tasks faster. Augmented cash collections change how payment decisions, execution, and controls are designed, using data and structure to improve outcomes rather than just reduce effort.

Not necessarily. Many agencies layer augmented strategies on top of existing CRMs and core systems by improving execution logic, payment orchestration, and visibility rather than performing a full system rip-and-replace.

Early indicators such as payment completion rates and time-to-resolution often improve within weeks. Larger gains in recovery efficiency and compliance consistency typically appear as strategies are applied across more accounts and stages.

Yes. While larger agencies benefit from scale, smaller agencies often see faster gains because execution gaps are easier to identify and correct. The key factor is operational discipline, not portfolio size.

When implemented correctly, they improve transparency, reduce friction, and give consumers more control over how they resolve accounts. This often leads to higher follow-through without increasing pressure or complaints.