More than 128,000 debt-related complaints from California consumers reached the CFPB in a single reporting period, according to a Bureau letter to the DFPI. That is not a consumer literacy problem. That is a compliance infrastructure problem.

California is one of the most aggressively enforced debt collection environments in the country. Regulators are active, penalties are steep, and consumers are increasingly aware of their rights. For collection agencies, law firms, and debt buyers, one misclassified account or a missed disclosure does not stay quiet for long.

Understanding the statute of limitations on California debt is the starting point. But knowing the rule is the easy part. The harder part is building operations that apply it correctly, consistently, across every account in your portfolio.

This guide covers exactly that.

The statute of limitations on debt in California sets the legal deadline to file a lawsuit to recover an unpaid debt. After it expires, courts will dismiss a case if the consumer raises it as a defense.

Under California law, most written consumer‑debt contracts have a four‑year limit, while debts based on oral contracts generally have a two‑year limit. The statute affects only legal enforcement, not the underlying debt; collection efforts can continue, but creditors can no longer sue once the period expires.

For collection agencies and law firms, it acts as a litigation gatekeeper, determining:

California does not apply a single limitation period to all debts. Correct classification matters because applying the wrong statute can result in cases being dismissed, compliance exposure, and wasted legal resources.

Use the table below as your quick reference when classifying accounts at intake.

Choice-of-law note: Some credit card agreements include clauses designating another state's law. Delaware and South Dakota are common examples because major issuers are incorporated in those states. California courts often apply California law regardless, but agencies handling purchased portfolios should review the underlying agreement before assuming which statute applies.

Getting the start date wrong is one of the most common and costly errors in managing California accounts. A misidentified default date can make a litigable account look expired, or push an expired account into legal review.

In California, the limitation period begins when the cause of action accrues. For most debt, that is the date of the first missed payment that was not cured, not the charge-off date, not the assignment date, and not the date a final statement was sent.

Example: A consumer misses their January 2021 credit card payment. The statute of limitations starts running from that January default, not from the July 2021 charge-off date. An agency using the charge-off date as the trigger would miscalculate the expiration by six months and potentially route a time-barred account into legal review.

These are common sources of misclassification in purchased portfolios. None of them restarts or extends the limitation period unless a debtor takes a specific action, which is covered in the next section.

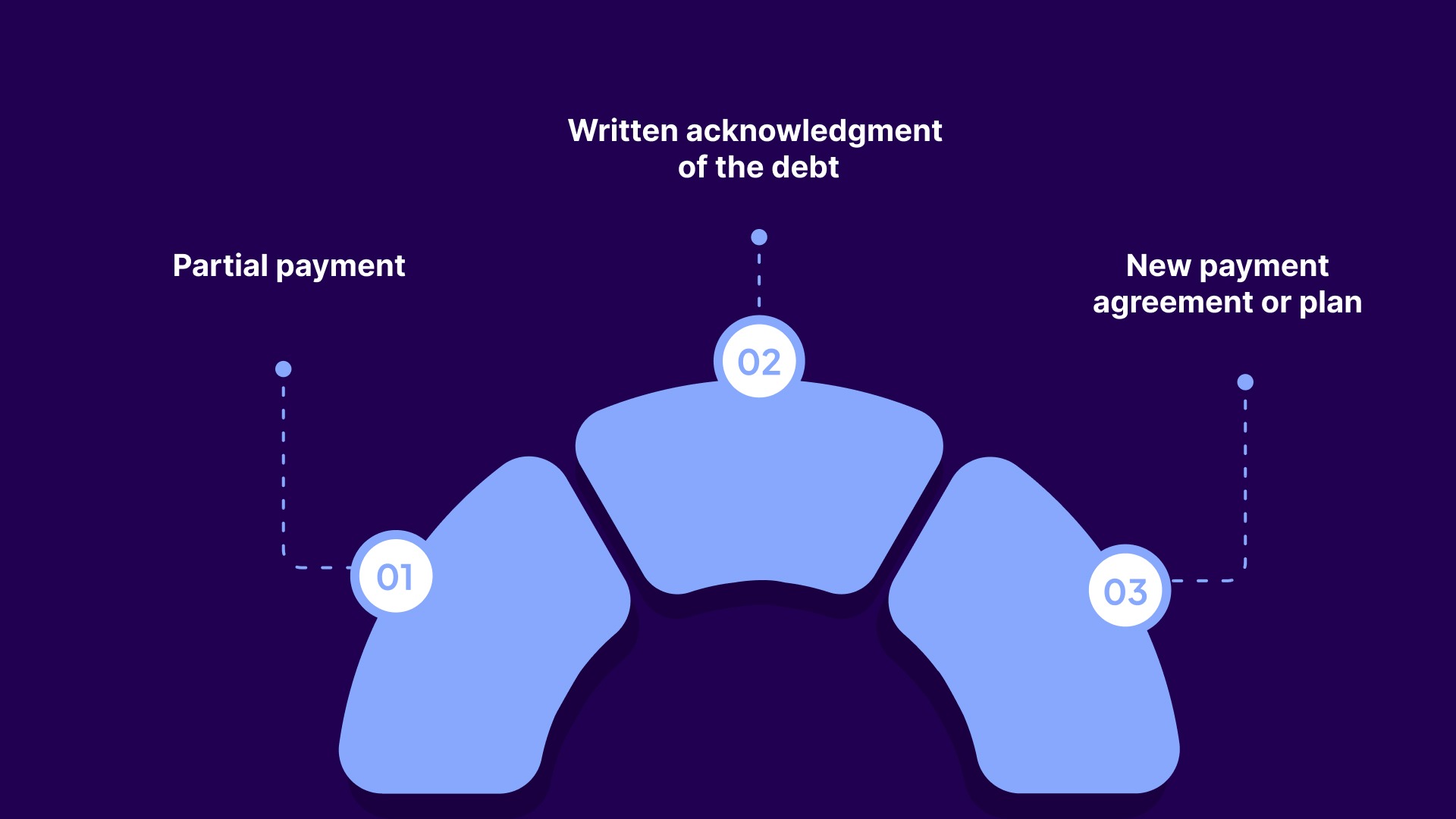

The four-year window is not always fixed. Certain debtor actions can restart it entirely, and certain circumstances can pause it temporarily. Both have real operational implications for how you manage and document California accounts.

For high-volume portfolios, these events need to be tracked at the account level. An account that looks expired on paper may still fall within the actionable window if a tolling event occurred and was not recorded.

Tracking limitation dates manually across California portfolios creates real risk. Tratta is designed to help collection teams centralize account data, enforce state-specific limitation rules, and prevent time-barred accounts from entering legal queues. Book a free call to see how it works.

Once the statute of limitations expires, an account is time-barred for litigation. California does not prohibit all post-expiration collection activity, but it draws clear lines around what is and is not allowed. Agencies operating in this state are held to a high standard on both sides.

The §1788.14 disclosure is a standalone compliance requirement. It must appear in the first written communication after the statute expires and must state that the debt is too old for legal action, and that making a payment or acknowledging the debt may affect applicable timelines. Missing this is a violation, regardless of whether any other part of the outreach is handled correctly.

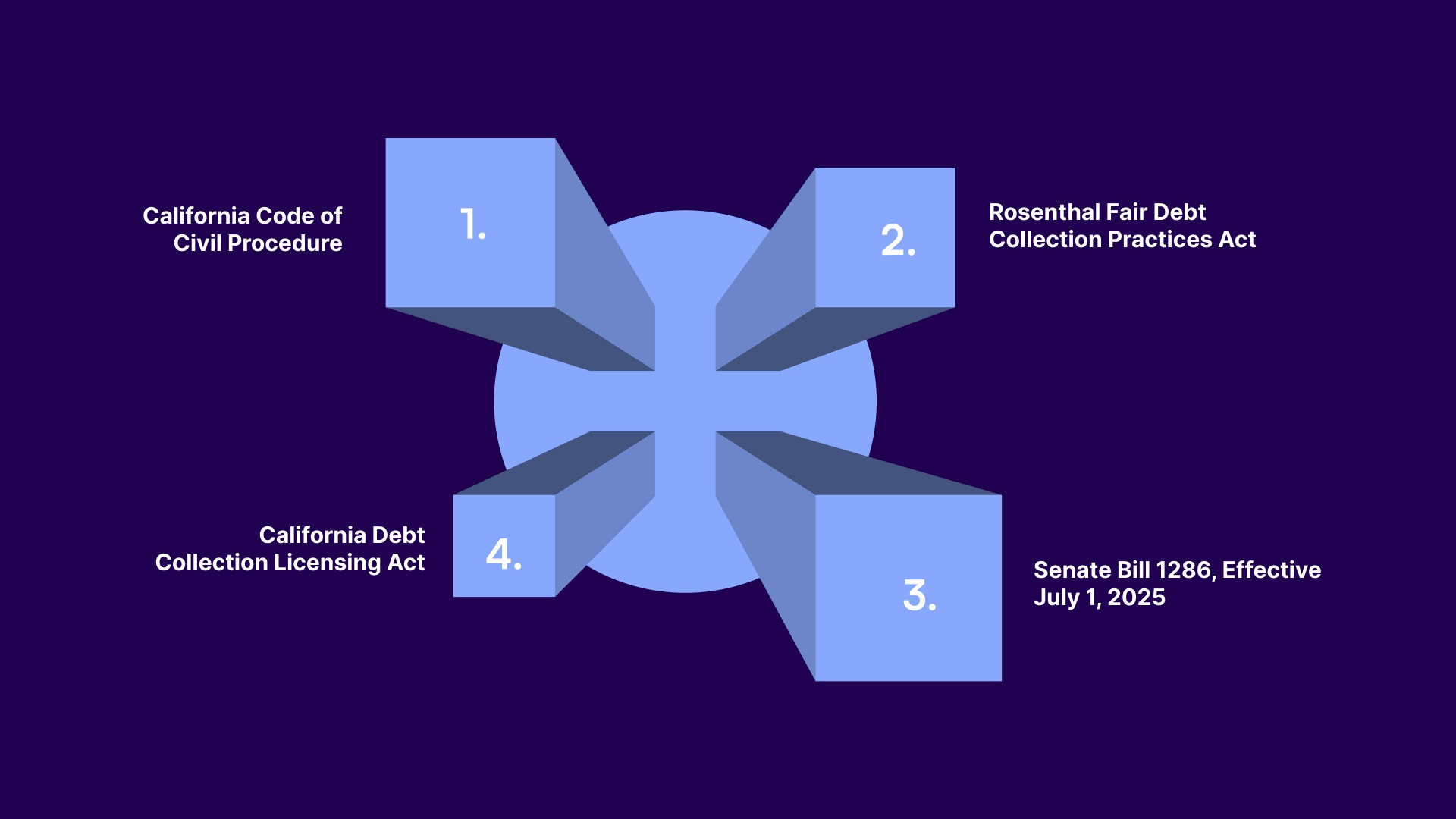

The statute of limitations does not operate in isolation. A set of state and federal laws governs how limitation periods are tracked, disclosed, and enforced. If you manage California accounts, all of these affect your day-to-day operations.

CCP § § 337, 339, and 337.5 define the limitation periods for written contracts, oral contracts, and judgment enforcement, respectively. Courts apply these sections directly when deciding whether a case can move forward. Misclassifying an account under the wrong section can invalidate an otherwise eligible filing.

California's Rosenthal Act is broader than the federal FDCPA in one important way: it applies to original creditors collecting their own debts, not just third-party collectors. A bank or lender pursuing overdue accounts directly must meet the same standards as an external agency. Violations carry statutory damages of $100 to $1,000 per violation, plus actual damages and attorney's fees.

The RFDCPA specifically prohibits threatening legal action on time-barred accounts and misrepresenting the legal status of any debt. California also incorporates federal FDCPA sections 1692b through 1692j by reference under Civil Code §1788.17, meaning a state violation and a federal violation often run simultaneously.

SB 1286 is the most significant update to California's debt collection framework in recent years. It extends the protections of the Rosenthal Act to commercial debts up to $500,000 that are originated, renewed, sold, or assigned on or after July 1, 2025.

For agencies, law firms, and debt buyers handling mixed portfolios, the practical impact is direct:

SB 1286 does not add new licensing requirements for commercial debt collectors, but existing DCLA licenses must cover those collection activities. All written communications must display the collector's DFPI license number in 12-point type.

Effective January 1, 2022, the DCLA requires all debt collectors and debt buyers operating in California to be licensed by the Department of Financial Protection and Innovation (DFPI). Unlicensed collection activity carries penalties including fines, cease‑and‑desist orders, and license revocation. The DFPI actively enforces the DCLA and has imposed significant fines on multiple collectors for practices including fake legal threats and unlicensed operations.

Most compliance discussions stop at knowing the rules. For collection agencies, law firms, and debt buyers managing California accounts at volume, the real risk is operational: where correct rules meet inconsistent data and high throughput.

In purchased portfolios, missing payment history often leads teams to rely on charge-off dates. In California, this typically overstates the timeline, making expired accounts appear legally actionable.

Without these fields, limitation tracking is unreliable. Accounts with incomplete data should be held for verification rather than routed into active workflows.

Applying a uniform rule across states ignores California’s shorter timelines. Accounts can reach legal review after expiration without being flagged.

Commercial accounts meeting SB 1286 criteria now require consumer-like limitation tracking and disclosures. Skipping this check creates new compliance exposure.

In high-volume environments, manual controls fail. Time-barred accounts can slip into litigation without automated gating and documented overrides.

Combining these accounts within the same workflow results in non-compliant outreach, inefficient legal review, and reduced recovery performance.

This distinction trips up consumers and also creates internal confusion on operations teams. The California debt statute of limitations and the credit reporting window are governed by different rules and run on different clocks.

A debt can be time-barred for litigation purposes yet remain on a credit report for years afterward. Conversely, an account can be removed from a credit report while still within the statute of limitations. Your outreach strategy and account routing need to account for both timelines independently, not as one combined deadline.

Note: California’s SB 1061, effective January 1, 2025, prohibits most medical debt from appearing on California consumer credit reports. If your portfolio includes California medical accounts, those debts no longer generate credit‑reporting leverage regardless of their limitation status. This affects how you structure outreach and settlement offers for medical portfolios.

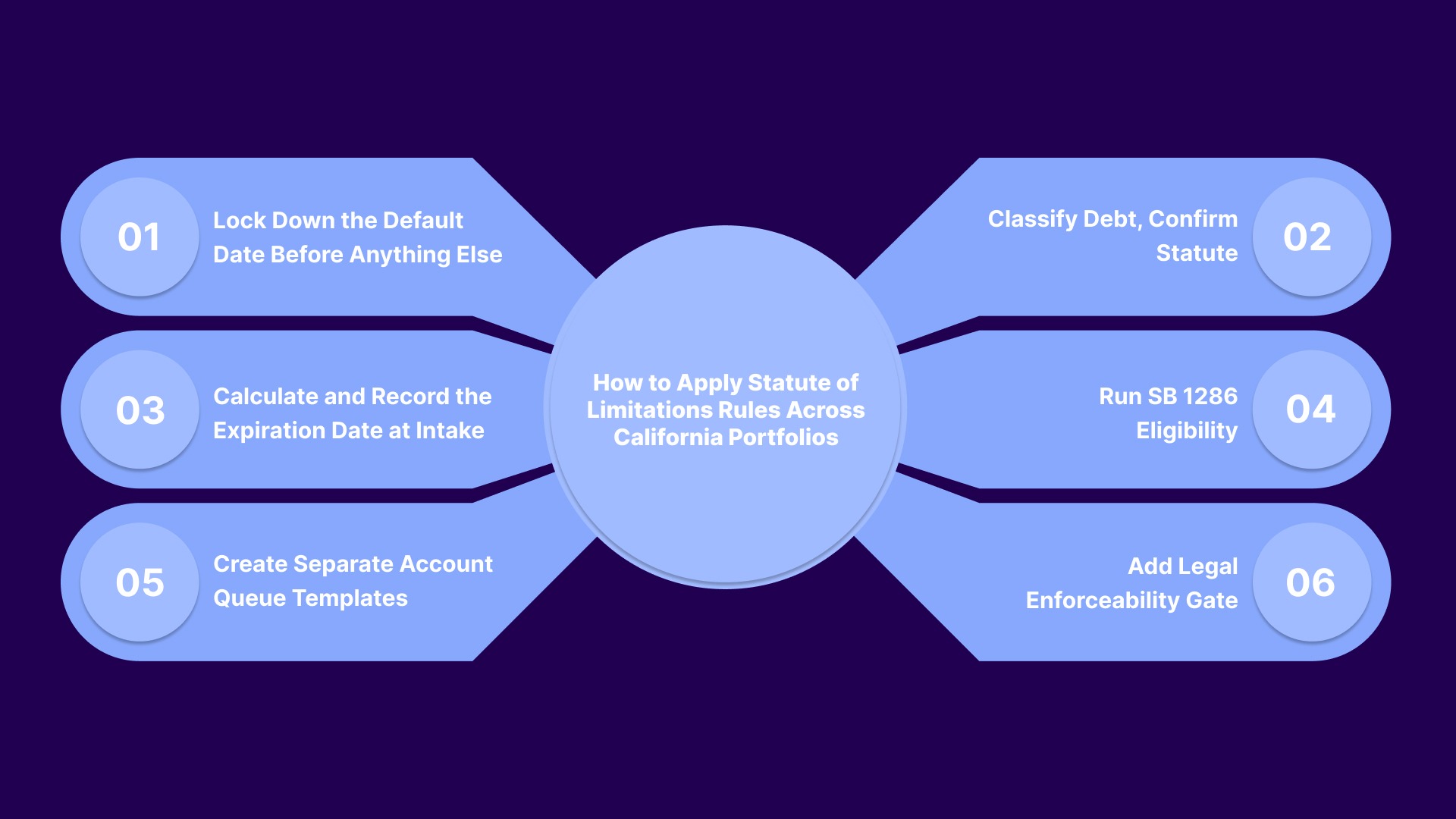

The rules above only work if your operations consistently apply them. Here is a practical framework covering what to do at each stage, with the errors it prevents.

When a California account comes in, the first question is: what is the verified last payment date and confirmed first default date? Not the charge-off date, not the assignment date.

For example, if you are onboarding a purchased credit card portfolio and the seller's file includes charge-off dates but no payment history, hold that segment in a documentation queue and request the original creditor's payment records before those accounts move anywhere. A verified default date is the foundation for every downstream decision.

Apply four years to written contracts, open accounts, and commercial debt within SB 1286's scope. Apply for two years to oral contracts. For purchased portfolios, pull the underlying credit agreement and check for a choice-of-law clause before assuming California's statute governs.

A common error here is treating all credit card accounts the same, regardless of the issuer's state of incorporation. If the agreement specifies Delaware law, that account may be subject to Delaware's limitation period and should be flagged separately.

Once the default date is confirmed and the applicable statute identified, calculate the expiration date and record it on the account record before routing. For a January 2022 default on a written contract, that expiration date is January 2026.

Do not wait until the account reaches legal review to run this calculation. By then, the error has already moved through your workflow. Intake is the only point where catching this is clean and low-cost.

For any commercial account in your portfolio: check whether it was originated, renewed, sold, or assigned after July 1, 2025. If it meets that threshold and the balance is under $500,000, it now follows consumer-equivalent rules under the Rosenthal Act.

In practice, this means updating your intake form to include an origination or assignment date field for commercial accounts, and adding a routing rule that flags any post-July 2025 commercial account for the same disclosure and limitation tracking workflow as your consumer accounts.

Accounts within the statute and accounts past it need to live in different places in your system, not just different status tags. Each queue needs its own communication template set built around the enforceability status.

For time-barred accounts, every outbound communication template must include the §1788.14 disclosure language. The simplest way to enforce this is to make it a fixed header or footer in all templates assigned to the time-barred queue, not an optional field an agent can toggle. One missed disclosure is a violation; a pattern of them is a regulatory event.

Before any California account can move to legal placement, it must pass an enforceability check confirming that the expiration date is in the future and that no documented tolling or resetting event has altered that calculation.

This does not need to be complex. It can be a required field check in your case management system, a compliance sign-off step, or a simple rule that blocks legal escalation if the calculated expiration date field is in the past. Whatever the mechanism, it needs to be system-enforced, not reliant on an individual agent's awareness.

Want better visibility into the status of limitations across your California portfolios?

Tratta's reporting and analytics tools help compliance and operations teams track account-level limitation data, flag at-risk accounts before they reach legal review, and maintain audit-ready records. Explore the platform: tratta.io

Knowing the statute of limitations is one part of it. The real challenge is keeping limitation status, outreach, and payments aligned across systems at scale, where most compliance risk actually shows up.

Tratta is a digital-first debt collection platform built for collection agencies, law firms, creditors, and debt buyers. It centralizes consumer engagement, payments, and workflow controls, helping teams operationalize compliance without adding manual overhead.

In practice, this ensures statute-of-limitations compliance is enforced directly in execution, while improving recovery performance and reducing operational risk.

California's statute of limitations for debt is among the most strictly enforced in the country. The four-year window on written contracts, the mandatory §1788.14 disclosure for time-barred accounts, and SB 1286's 2025 expansion into commercial portfolios all point in the same direction: the compliance bar in California is high, and enforcement is active.

For collection agencies, law firms, and debt buyers, the path to getting this right is operational. Confirm default dates at intake. Classify accounts correctly. Separate litigation-eligible accounts from expired ones before they reach your legal team. Build the required disclosure language into your communication templates, not just into agent training. And put a system-level gate in front of every legal placement decision.

Tratta is built to support these workflows across payments, communications, reporting, and escalation controls on a single platform. If your team manages California accounts and wants clearer visibility into limitation status and more consistent compliance across your operations, schedule a demo to see how Tratta can help.

When key dates are missing, teams rely on original creditor records, payment histories, and account statements. Accounts should be held from workflows until verified to avoid misclassification.

Yes. Choice-of-law clauses may apply another state’s statute, but California courts often still apply local limits. Always review the original agreement before legal routing decisions.

Accounts nearing expiration should be flagged early, prioritized for review, and restricted from legal escalation unless timelines are verified to prevent last-minute compliance errors.

System-level controls like enforceability checks, state-based routing, and separate workflows for time-barred accounts help ensure consistent compliance across high-volume portfolios.

Time-barred accounts reduce the potential for legal recovery, directly affecting portfolio value. Accurate limitation tracking improves pricing models, segmentation, and expected recovery forecasting.